The family business in new EU countries: the spread and agency conflicts they face

Dr. Alfreda Sapkauskiene

Vilnius University,

Lithuania

Email: alfreda.sapkauskiene@evaf.vu.lt

Liliana

Sileikiene

Ernst & Young Baltic, Lithuania

Email: liliana.sileikiene@lt.ey.com

Abstract. Capital financing is vital for the development of the new EU countries. Investors base their economic and financial decisions on the information available in the financial reports that listed EU companies must prepare following International Financial Reporting Standards (IFRS). Studies show that the majority of listed companies worldwide are family owned and face Type II agency problem - the conflict between minority shareholders and large controlling shareholders (family), i.e. controlling family may seek to extract private benefits at the expense of minority shareholders and disclose information in financial reports for self-interested purposes to avoid minority contests. The research of Type II agency conflict effects on mandatory IFRS disclosure levels in the new EU countries is limited, however, with the reference to existing research literature and legal systems in the new EU countries, we find that minority protection is strongest in Malta, and weakest in Latvia. The biggest number of family controlled firms are in Poland and Romania, whilst family business in Poland, Estonia, Croatia, Cyprus, Romania and Bulgaria enjoy the largest market capitalisation. Nationally, the highest market capitalisation of family controlled firms are in Estonia, Cyprus, Latvia and Poland. This paper shows, that due to moderate minority protection in the new EU countries Type II agency conflict is important, and therefore, it is suggested further the research related to mandatory IFRS disclosure levels.

Key words: family business, listed companies, new EU countries, shareholders minority, type II agency problem.

JEL Code: M10, M48, G00

Copyright © 2019 Alfreda

Sapkauskiene, Liliana Sileikiene. Published by Vilnius University Press

This

is an Open Access article distributed under the terms of the Creative Commons

Attribution Licence, which permits unrestricted use, distribution, and

reproduction in any medium, provided the original author and source are

credited.

Pateikta / Submitted on 03.10.2019

Introduction

To maintain continuous economic development in new EU countries and to create new workplaces, it is vitally important to create favourable conditions for companies to attract capital financing in these markets. The economy grows when companies can create added value: to develop new products, to hire employees, to increase production capacities and to expand business to new markets. All of this is possible if companies can attract capital to finance their development. In order to attract investors’ financing, companies have to trade their shares on stock exchanges. Investors base their economic and financial decisions on the information available in the financial reports. According to 19 July 2002 Reglament (European Communities) No. 1606/2002, starting on 1 January 2005, consolidated statements of Member State companies shall comply with International Financial Reporting Standards (IFRS), which strictly regulate financial disclosure.

Family-controlled businesses are rather common among listed companies in various countries (Faccio & Lang, 2002; Anderson & Reeb, 2003; Villalonga & Amit, 2006). Actually, many companies throughout the world are controlled by large shareholders, mostly families. Porta, Lopez-de-Silanes & Shleifer (1999) acknowledge that family controlled business is the most widespread form of organizational structure, especially in countries with weak protection of minority shareholders. Family controlled business faces Type II agency problem – the conflict between minority shareholders and large controlling shareholders (family), as they hold significant ownership and have control over the firm (Shleifer & Vishny, 1986). Controlling family may seek to extract private benefits at the expense of minority shareholders, make decisions that are not beneficial to minority interests and disclose information in financial reports for self-interested purposes to avoid minority contests.

Most family controlled business studies refer to USA (Anderson & Reeb, 2003; Villalonga & Amit, 2006; Ali, Chen & Radhakrishnan, 2007; Villalonga & Amit, 2010; McGuire, Dow & Ibrahim, 2012; Villalonga et al., 2015; Martin, Campbell, & Gomez-Mejia, 2016), West Europe (Faccio & Lang, 2002; Cascino et al., 2010; Cucculelli & Marchionne, 2012; Bouzgarrou & Navatte, 2013; Poutziouris, Savva, & Hadjielias, 2015), East Asia (Claessens, Djankov & Lang, 2000; Jaggi, Leung & Gul, 2009; Jiang & Peng, 2011; Wu, 2013; Cheng, 2014; Abdullah et al., 2015), Near East (Al-Akra & Hutchinson, 2013; Haddad et al., 2015). The research of family controlled business in the new EU countries is limited. Family firms in Czech Republic and Poland are the most studied out of 13 new EU countries (Zapalska, 1997; Zapalska et al., 2003; Kowalewski, Talavera, & Stetsyuk, 2010). Research of family-controlled businesses in the new EU countries is limited, so it would be appropriate to examine the effects of Type II agency problems on mandatory IFRS disclosure levels, as financial disclosure influences the actions of investors – minority shareholders – and provides them with the information they need to make rational economic decisions.

The objective of this paper is to take the first step and study the spread of listed family controlled firms in new EU countries to find out a necessity of the research on minority shareholders sensitive information disclosure level in listed family controlled firms’ financial reports.

The remainder of this paper is constructed as follows. Section 1 reviews prior family business and Type II agency problem research literature. Section 2 provides the research methodology. Results are reported in section 3.

1. Family Business Literature Review

Family controlled business have some unique characteristics: (1) possess little diversified portfolios due to their concentrated ownership, (2) have longer investment horizons due to passing on ownership as an asset to the future generations, (3) family members are strongly involved in the management of their firms (Cheng, 2014). A few studies point out that family business represent over a third of large listed USA firms (Anderson & Reeb, 2003; Villalonga & Amit, 2006), over 55% if smaller listed firms are included (Villalonga & Amit, 2010). In Western Europe family business account for 44% of listed companies (Faccio & Lang, 2002) and in East Asia over two-thirds of firms (Claessens, Djankov & Lang, 2000). According to data from the EU Federation of National Associations „European family businesses“, in most new EU countries, family-controlled business accounts for more than 70% of all listed and non-listed firms.

Over the past 10-15 years, family business has showed up as leading research subject within finance literature (Villalonga et al., 2015). Due to unique characteristics, family business face unique agency conflicts. Villalonga et al. (2015) reviewed family business studies in finance and accounting literature and found that the dominant theoretical perspective has been agency theory. There are 4 conflicts family business faces in existing research literature: (1) shareholders vs managers (Jensen & Meckling, 1976), (2) controlling (family) shareholders vs minority shareholders (Shleifer & Vishny, 1986), (3) shareholders vs creditors, (4) family shareholders vs family outsiders (non-shareholders, non-managers). Actually, the finance literature about family controlled business has more concisely focused on the first two of above mentioned problems, i.e. Type I Agency problem and Type II Agency problem (Villalonga et al., 2015).

Type I Agency problem appears, when managers not act in the best interests of shareholders, i.e. owners‘ and managers‘ interest are not aligned. This problem is reduced in family controlled business. Concentrated and under-diversified ownership, long investment horizons due to passing on ownership as an asset to the future generations and family‘s reputation are strong incentives for family shareholders to monitor managers. Usually, in family controlled business owner and CEO are the same person, thus there is no inducement misalignment and no Type I Agency problem (Cheng, 2014).

Type II Agency problem appears, when controlling family not act in the best interests of minority shareholders, i.e. concentrated ownership and substantial control gives the opportunity to extract private benefits at the expense of minority shareholders (e.g. family members exaggerated compensation, related party transactions, or special dividends) (Burkart, Panunzi, & Shleifer, 2003). Difference between family control rights and cash flows (dual-class shares, voting agreement, and pyramid ownership structures) provides family with the inducement and ability to pursue private benefits. In summary, family business face more severe Type II Agency problem (Cheng, 2014).

2. Research Methodology

Sample design. We chose 13 EU countries that joined the EU in 2004 or later for the research. For the homogeneity determination, we have assessed the political past and legal systems of the countries. The level of protection of minority shareholders in the new EU countries was determined with reference to the existing research literature and legal systems of countries. Data were collected on 11 February, 2017, from Bloomberg Financial Markets Lab. Our initial sample consisted of 1,647 listed companies from non-financial sectors in 13 new EU countries. As in prior studies, we excluded financial firms, since they operate in a specific sector where disclosure is object of sector’s regulatory requirements (Ben Ali, 2014). We discard all firms with missing market capitalisation data on 11th of February, 2017 (270 firms). The final sample included 1,377 listed companies. In order to select family-controlled firms, we refer to the definition of family business[1] put forth by the European Commission (EC) in November 2009 and according to it we selected 256 family-controlled firms.

Data collection method. For this study, we have used content analysis as a method of collecting and analysing data. For detecting of Type II Agency problem appearance, the level of protection of minority shareholders in the new EU countries was determined with regards to the existing research literature and legal systems of countries. The spread of listed family controlled firms in new EU countries was determined according to a family controlled firms market capitalisation.

3. Research Results Sectors

New EU countries are homogeneous, and they have three similarities: (1) most countries (except Cyprus and Malta) became free from a communist regime from 1989 to 1993, (2) most countries (except Bulgaria, Romania and Croatia) joined the EU in 2004 and (3) most countries’ (except Cyprus and Malta) legal system is civil-law.

A common attribute for new EU countries (except Cyprus and Malta) is the post-communism stamp and transition from a centrally planned economy to a market economy. The different privatization techniques in all transition economies in Central and East Europe countries led to a concentrated ownership structure which is typical for all Continental European countries (Sethi, Braendle & Noll, 2006). After privatization new EU countries are characterized by concentrated ownership of managers or strong influence of the state and interest groups as well as weak minority shareholders protection (Aoki, 1995), which meets Lopez-de-Silanes et al. (1998) findings, that concentration of ownership of shares in listed companies is negatively related to investor protections.

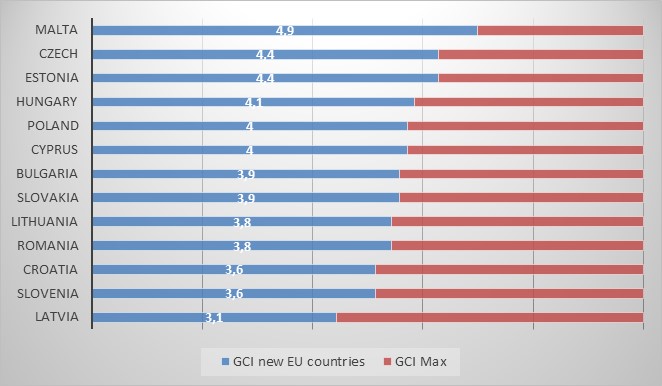

Legal system (common-law or civil-law) characterizes juridical and economical development level of country. According to Lopez-de-Silanes et al. (1998), common-law countries typically have the strongest, German-civil-law countries the moderate and French-civil-law countries the weakest legal protection of investors. Hence, minority shareholders protection should be strongest in Cyprus and Malta as a common law countries, while weakest in Bulgaria and Romania as a French-German-civil-law countries. According to The Global Competitiveness Report 2017–2018 (Schwab, Sala i Martin, 2017) the average of Global Competitiveness Index (GCI) protection of minority shareholders‘ interests (1 = not protected at all; 7 = fully protected) in new EU countries is 3.96, i.e. moderate. Hence, according to the Global Competitiveness Report 2017–2018, minority shareholders protection is strongest in Malta (4.9), while weakest in Latvia (3.1). GCI protection of minority shareholders‘ interests are presented in Figure 1.

Figure 1. Global Competitiveness Index (GCI) in new EU countries

Source: The Global Competitiveness Report 2017–2018 (Schwab, Sala i Martin, 2017)

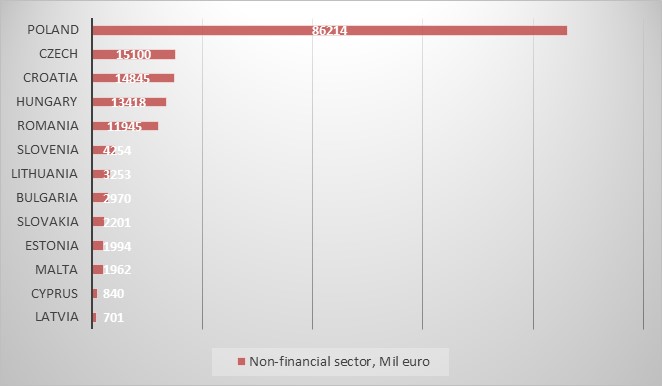

Every year, European Securities and Markets Authorities (ESMA) presents a list of EU-regulated markets. All new EU countries have their national regulated markets, which are included in the ESMA list. The Warsaw stock exchange stands out from other EU countries’ stock exchanges because market capitalisation is 123 times higher than the lowest Nasdaq Riga market capitalisation and 6 times higher than the second highest market capitalisation, the Prague stock exchange. The highest market capitalisations include the Poland, Czech Republic, Croatia, Hungary and Romania stock exchanges, whose values are more than 10 mil euro. Less than 5 mil euro market capitalisations has Slovenia, Lithuania, Bulgaria, Slovakia, Estonia, Malta, Cyprus and Latvia stock exchanges (see Figure 2).

Figure 2. Market capitalisation in new EU countries

Source: Bloomberg, 2017

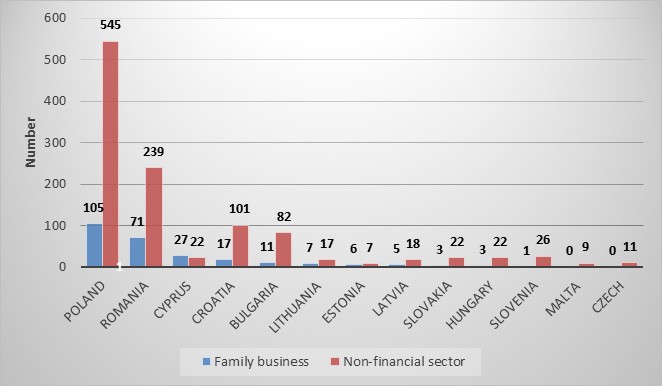

Figure 3 presents the number of family-controlled firms and all non-financial firms that are in regulated markets. Cyprus regulated market has larger number of family firms than non-family firms, the most family-controlled businesses are in Poland (105) and Romania (71).

Figure 3. Family business units in new EU countries

Source: Bloomberg, 2017

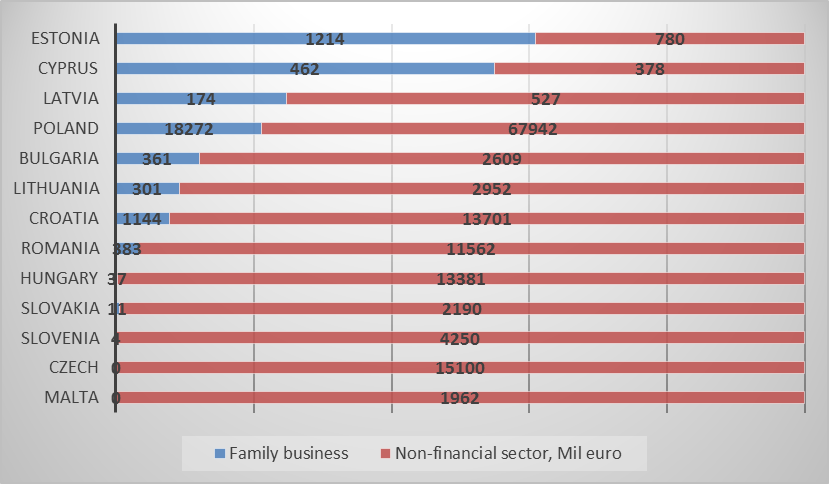

Highest market capitalisation of family firms are in Poland (EUR 18,272.31 million), Estonia (EUR 1,214.56 million), Croatia (EUR 1,144.15 million), Cyprus (EUR 462.44 million), Romania (EUR 382.99 million) and Bulgaria (EUR 360.91 million), while in Czech Republic and Malta we did not find family businesses companies at all (see Figure 4).

Fig. 4. Family businesses market capitalisation (EUR million)

Source: Bloomberg, 2017

Fig. 5. Family businesses in new EU countries (EUR million)

Source: Bloomberg, 2017

Nationally, the highest market capitalisation of family firms is in Estonia (61%), Cyprus (55%), Latvia (25%), Poland (21%), Bulgaria (12%), Lithuania (9%), Croatia (8%) and Romania (3%).

Conclusion

As a higher majority of new EU countries had a transition from a centrally planned economy to a market economy, according to previous findings, it led to a concentrated ownership structure as well as to a weak minority shareholders protection. In the new EU countries where there is mostly a high concentration of ownership of listed companies (except the Czech Republic, Malta, Slovenia, Slovakia and Hungary) the moderate protection of minority shareholders was found. The weakest minority protection was found in Latvia, whilst strongest minority protection – in Malta.

The market capitalisation of family controlled firms in Poland is EUR 18,272.31 million, Estonia – EUR 1,214.56 million, Croatia – EUR 1,144.15 million, Cyprus – EUR 462.44 million, Romania – EUR 382.99 million, Bulgaria – EUR 360.91 million, Lithuania – EUR 301.34 million and Latvia – EUR 173.90 million, while nationally, the market capitalisation of family controlled firms in Estonia is 61%, Cyprus – 55%, Latvia – 25%, Poland – 21%, Bulgaria – 12%, Lithuania – 9%, Croatia – 8% and Romania – 3%. It means, that family controlled firms with large market capitalisation are widespread in 8 of 13 new EU countries.

This paper shows, that due to moderate minority protection in 8 new EU countries Type II agency conflict is important, and therefore, it is suggested to further the research related to minority shareholders sensitive information disclosure level in listed family controlled firms’ financial reports in new EU countries: Poland, Estonia, Croatia, Cyprus, Romania, Bulgaria, Lithuania and Latvia.

References

Abdullah, M.; Evans, L.; Fraser, I., Tsalavoutas, I., 2015. IFRS mandatory disclosures in Malaysia: The influence of family control and the value (ir)relevance of compliance levels. Accounting Forum. 39(4), p. 328-348. DOI: http://dx.doi.org/10.1016/j.accfor.2015.05.003.

Al-Akra, M.; Hutchinson, P., 2013. Family firm disclosure and accounting regulation reform in the Middle East: The case of Jordan. Research in Accounting Regulation. 25(1), p. 101-107. DOI: http://dx.doi.org/10.1016/j.racreg.2012.11.003.

Ali, A.; Chen, T.; Radhakrishnan, S., 2007. Corporate disclosures by family firms. Journal of Accounting and Economics. 44(1–2), p. 238-286. DOI: http://dx.doi.org/10.1016/j.jacceco.2007.01.006.

Anderson, R. C.; Reeb, D. M., 2003. Founding‐family ownership and firm performance: Evidence from the S&P 500. The Journal of Finance. 58(3), p. 1301-1328.

Aoki, M., 1995. Controlling insider control: issues of corporate governance in transition economies. Corporate Governance in Transitional Economies, p. 3-30.

Ben Ali, C., 2014. Corporate governance, principal- principal agency conflicts, and disclosure. The Journal of Applied Bussiness Research. 30(2), p. 419-432. DOI: https://doi.org/10.19030/jabr.v30i2.8412.

Bouzgarrou, H.; Navatte, P., 2013. Ownership structure and acquirers performance: Family vs non-family firms. International Review of Financial Analysis. 27, p. 123-134. DOI: http://dx.doi.org/10.1016/j.irfa.2013.01.002.

Burkart, M.; Panunzi, F.; Shleifer, A., 2003. Family firms. The Journal of Finance. 58(5), p. 2167-2202.

Cascino, S.; Pugliese, A.; Mussolino, D.; Sansone, C., 2010. The influence of family ownership on the quality of accounting information. Family Business Review. 23(3), p. 246-265.

Cheng, Q., 2014. Family firm research – A review. China Journal of Accounting Research. 7(3), p. 149-163. DOI: http://dx.doi.org/10.1016/j.cjar.2014.03.002.

Claessens, S.; Djankov, S.; ; Lang, L. H., 2000. The separation of ownership and control in East Asian corporations. Journal of financial Economics. 58(1), p. 81-112.

Cucculelli, M.; Marchionne, F., 2012. Market opportunities and owner identity: Are family firms different? Journal of Corporate Finance. 18(3), p. 476-495. DOI: http://dx.doi.org/10.1016/j.jcorpfin.2012.02.001.

Lopez - de Silanes, F. L.; Porta, R.; Shleifer, A.; Vishny, R., 1998. Law and finance. Journal of Political Economy. 106(6), p. 1113-1155.

ESMA European Securities and Markets Authority. Available at: <https://www.esma.europa.eu/databases-library/registers-and-data> [Accessed February 28, 2018].

Faccio, M.; Lang, L. H. P., 2002. The ultimate ownership of Western European corporations. Journal of Financial Economics. 65(3), p. 365-395. DOI: http://dx.doi.org/10.1016/S0304-405X(02)00146-0.

Haddad, A.; AlShattarat, W.; AbuGhazaleh, N.; Nobanee, H., 2015. The impact of ownership structure and family board domination on voluntary disclosure for Jordanian listed companies. Eurasian Business Review. 5(2), p. 203-234. DOI: https://doi.org/10.1007/s40821-015-0021-5.

Jaggi, B.; Leung, S.; Gul, F., 2009. Family control, board independence and earnings management: Evidence based on Hong Kong firms. Journal of Accounting and Public Policy. 28(4), p. 281-300. DOI: http://dx.doi.org/10.1016/j.jaccpubpol.2009.06.002.

Jensen, M. C.; Meckling, W. H., 1976. Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics. 3(4), p. 305-360. DOI: http://dx.doi.org/10.1016/0304-405X(76)90026-X.

Jiang, Y.; Peng, M., 2011. Are family ownership and control in large firms good, bad, or irrelevant? Asia Pacific Journal of Management. 28(1), p. 15-39. DOI: https://doi.org/10.1007/s10490-010-9228-2.

Kowalewski, O.; Talavera, O.; Stetsyuk, I., 2010. Influence of family involvement in management and ownership on firm performance: Evidence from Poland. Family Business Review. 23(1), p. 45-59. DOI: https://doi.org/10.1177/0894486509355803.

Martin, G.; Campbell, J.; Gomez-Mejia, L., 2016. Family control, socioemotional wealth and earnings management in publicly traded firms. Journal of Business Ethics. 133(3), p. 453-469. DOI: https://doi.org/10.1007/s10551-014-2403-5.

McGuire, J.; Dow, S.; Ibrahim, B., 2012. All in the family? Social performance and corporate governance in the family firm. Journal of Business Research. 65(11), p. 1643-1650. DOI: http://dx.doi.org.ezproxy.ktu.edu/10.1016/j.jbusres.2011.10.024

Porta, R.; Lopez‐de‐Silanes, F.; Shleifer, A., 1999. Corporate ownership around the world. The Journal of Finance. 54(2), p. 471-517.

Poutziouris, P.; Savva, C. S.; Hadjielias, E., 2015. Family involvement and firm performance: Evidence from UK listed firms. Journal of Family Business Strategy, 6(1), 14-32. DOI: https://doi.org/10.1016/j.jfbs.2014.12.001.

Schwab, K.; Sala i Martin, X., 2017. Global Competitiveness Report 2017-2018, World Economic Forum, 09/2017. Available at: <http://www3.weforum.org/docs/GCR2017-2018/05FullReport/TheGlobalCompetitivenessReport2017–2018.pdf> [Accessed February 28, 2018].

Sethi, S. P.; Braendle, U. C.; Noll, J., 2006. Enlarged EU: Enlarged corporate governance? Why directives might be more appropriate for transition economies. Corporate Governance: The International Journal of Business in Society. 6(3), p. 296-304. DOI: https://dx.doi.org/10.2139/ssrn.556703.

Shleifer, A.; Vishny, R. W., 1986. Large shareholders and corporate control. Journal of Political Economy. 94(3), p. 461-488.

Villalonga, B.; Amit, R., 2006. How do family ownership, control and management affect firm value? Journal of Financial Economics. 80(2), p. 385-417. DOI: http://dx.doi.org/10.1016/j.jfineco.2004.12.005.

Villalonga, B.; Amit, R., 2010. Family control of firms and industries. Financial Management. 39(3), p. 863-904. DOI: https://doi.org/10.1111/j.1755-053X.2010.01098.x.

Villalonga, B.; Amit, R.; Trujillo, M.; Guzmán, A., 2015. Governance of family firms. Annual Review of Financial Economics. 7(1), p. 635-654. DOI: https://doi.org/10.1146/annurev-financial-110613-034357.

Wu, C., 2013. Family ties, board compensation and firm performance. Journal of Multinational Financial Management. 23(4), p. 255-271. DOI: http://dx.doi.org/10.1016/ j.mulfin.2013.01.001.

Zapalska, A., 1997. A Profile of Women Entrepreneurs and Enterprises in Poland Journal of Small Business Management. October, 76-83, p. 20.

Zapalska, A.; Shuklian, S.; Rudd, D.; Flanegin, F., 2003. Environment and Performance of Family Businesses in the Reforming Polish Economy. The Journal of East-West Business. 9 (1), 24-30.

Alfreda Sapkauskiene: Associate Professor, PhD of Social Sciences field, Management and Administration, Department of Finance, Faculty of Economics and Business Administration, Vilnius University, Vilnius, Email: alfreda.sapkauskiene@evaf.vu.lt, Contact: (+370 5) 236 142, Address: Sauletekio av. 9, II building, LT-10222, Vilnius.

Liliana Sileikiene: Master’s degree in Accounting and Audit, Kaunas University of Technology; Senior Consultant on Accounting Compliance and Reporting, Ernst&Young Baltic, Vilnius, Email: liliana.sileikiene@lt.ey.com