Ekonomika ISSN 1392-1258 eISSN 2424-6166

2021, vol. 100(2), pp. 144–170 DOI: https://doi.org/10.15388/Ekon.2021.100.2.7

The Symmetric and Asymmetric Time-Varying Causality Relationships Between the COVID-19 Outbreak and the Stock Exchange: The Case of Selected Countries

Cuma Demirtaş

Faculty of Economics and Administrative Sciences, Aksaray University, Turkey

Email: cumademirtas@aksaray.edu.tr

Munise Ilıkkan Özgür

Faculty of Economics and Administrative Sciences, Aksaray University, Turkey

Email: mozgur@aksaray.edu.tr

Esra Soyu

Aksaray University, Aksaray Vocational School of Social Sciences, Turkey

Email: esrasoyu@aksaray.edu.tr

Abstract. In this study, the effects of COVID-19 (mortality rate, case rate, and bed capacity) on the stock market was examined within the framework of the efficient market hypothesis. Unlike other studies in the literature, we used the variable of bed capacity besides the mortality rate and case rate variables. The relationship between the mentioned variables, using daily data between December 31 of 2019 and November 10 of 2020, has been analyzed with time-varying symmetric and asymmetric causality tests for China, Germany, the USA, and India. Considering that the responses to positive and negative shocks during the pandemic process may be different and that the results may change depending on time, time-varying symmetric and asymmetric causality tests were used. According to the time-varying symmetric causality test, stock markets in all countries were affected in the period when the cases first appeared. A causal relationship between COVID-19 and country stock markets was found. The results showed that the effects of the case rate and bed capacity on the stock market occurred around the same time in Germany and the United States; however, these dates differed in China and India. According to time-varying asymmetric causality test findings, the asymmetric effect of the pandemic on the stock market in countries emerged during the second wave. The findings showed that the period during which positive and negative information about the pandemic intensified coincided with the period during which the second wave occurred; besides, the results show the effect of this information on the stock market differed as positive and negative shocks.

Key Words: COVID-19, Symmetric Relationships, Asymmetric Relationships, Efficient Market Hypothesis

________

Received: 15/05/2021. Revised: 26/09/2021. Accepted: 04/10/2021

Copyright © 2021 Cuma Demirtaş, Munise Ilıkkan Özgür, Esra Soyu. Published by Vilnius University Press

This is an Open Access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Introduction

A new type of coronavirus called COVID-19 first appeared in Wuhan, China, in December 2019 and has caused great damage worldwide. Spreading at an alarming rate and infecting millions of people, the COVID-19 disease was declared a pandemic by World Health Organization (WHO) on March 11, 2020 (WHO, 2020). The data of the cases published by the WHO during the analysis period reveals a 4 times increase trend in number of cases worldwide. When the contagion process of the pandemic and the periods in which the cases increase are analyzed on a regional basis, the following dates and regions emerge: the first increase in the number of cases in the Western Pacific, which started on February 13; the second increase in cases on March 10 in Europe, the United States, the Eastern Mediterranean, the Western Pacific, Southeast Asia and Africa; the third beginning on August 1 in the United States, Southeast Asia, Europe, Africa, the Eastern Mediterranean and the Western Pacific; and the fourth beginning on November 6 in the EU, the United States, Southeast Asia, the Eastern Mediterranean, Africa and the Western Pacific. While China ranked first in the first increase in cases of the pandemic, Europe was first in the second increase, the USA in the third increase and again Europe in the fourth increase as the epicenter of the virus infections. As of November 10, 2020, there have been more than 50 million confirmed cases and 1,258,000 deaths in 208 countries, with the countries most affected by the pandemic being the United States, India, Brazil, Russia, France, Spain, Argentina, England, Colombia, and Mexico (WHO, 2020).

The spread of the coronavirus between countries has prompted many governments to take unprecedented measures to contain the pandemic. These measures have caused turmoil, erosion of confidence, and increased uncertainty in financial markets. As a result, the rate of market risk aversion has increased in a way that is unprecedented since the global financial crisis of 2008 (OECD, 2020). Investors are more optimistic when the market is in an upward trend and the perceived risk is reduced; when the market trends downwards, investors tend to be more pessimistic. This situation shows that investors’ emotions play an important role in stock markets (Liu, et al., 2020).

The information provided is effective for guiding investors’ emotions; it can provide signals to help in making investment decisions. The information provided concerning events can be perceived as positive, negative, or neutral news. This is because investors and businesses use this information to describe both past and future market conditions. Completeness, accuracy, and timeliness of information are important. The sooner the information is reflected in stock prices, the more efficient the stock market will be. The stock price adjusts quickly as new information becomes available and is absorbed by investors. Market efficiency is determined by the speed at which investors can respond to information (Machmuddah, et al., 2020).

Fama (1970) classified market efficiency as weak, medium strong, and strong forms. According to Fama, the inability to use past prices in future price estimates indicates the weak form of that market, the full reflection of publicly available information on stock prices indicates its medium strong form, and the reflection of all public and private sector information on stock prices makes up the strong form.

In this context, it is important to examine the effect of the information released about COVID-19 worldwide on the stock market. According to the information announced in the worldwide about the COVID-19 outbreak, stock markets were indeed affected. Whether the measures taken to combat the virus would be effective or the vaccine would be found had different effects on the stock market (Wagner, 2020).

This differentiation is manifested in negative and positive shocks on the stock market. Several studies in literature have examined the relationship between the COVID-19 pandemic and the stock market (e.g., Al-Awadhi, et al., 2020; Ashraf, 2020; Baker, et al., 2020; Lyócsa, et al., 2020; Mishra, et al., 2020; Narayan, et al., 2020; Okorie & Lin, 2020; Sharif, et al., 2020; Zhang, et al., 2020; Topcu & Gülal, 2020, Alfaro, et al., 2020; Zeren & Hızarcı, 2020; Gormsen & Koijen, 2020; Onali, 2020; and Erdem, 2020). In these studies, the effect of COVID-19 on the stock market was examined for case and death rates. However, the most important factor in combating the pandemic has been the strength of the health care system. Countries with strong health systems show rapid reflexes against the pandemic; they have prevented its spread with effective treatment methods. Conversely, the prolonging of the process of combating the pandemic in countries with weak health care systems caused devastating effects in many areas, especially economically and financially. In this respect, the strength of the health care system is one of the important indicators for the preparedness of a country to fight the pandemic. In line with this information, in addition to the mortality rate and case rate variables used in the literature, bed capacity is also considered an indicator for the strength of a country’s health care system.

The effect of COVID-19 on the stock market varies according to the successes and failures in fighting the pandemic. The method used here allows the detection of negative shocks (positive: decrease in the number of cases and death toll) and positive shocks (negative: increase in the number of cases and death toll) as positive shocks (increase in the stock market) and negative shocks (decrease in the stock market), respectively, during the COVID-19 pandemic period. However, tests developed for causality analysis (Hacker & Hatemi, 2006; Hsiao, 1981; Sims, 1972; Toda & Yamamoto, 1995) accept that the effect of positive shocks is the same as the effect of negative shocks. However, in financial markets, in the presence of asymmetric information and the heterogeneity of market participants, positive and negative shocks of the same magnitude do not draw similar reactions. In this case, the results obtained from the aforementioned tests can be misleading.

The aim of the study is to determine the effect of the pandemic on the stock market by using the variables of case (case rate), death (mortality rate) and bed (bed capacity) and to reveal whether the effect of the pandemic on the stock market changes over time. In this way, it will be revealed whether the bed capacity, which is one of the important indicators of the severity of the pandemic, affects the stock market and when and how the impact of the pandemic on the stock market begins.

This study contributes to the existing literature, since, unlike many other studies, it covers a wider time period and analyzes bed capacity in addition to mortality rate and case rate variables. In addition, in examining the effect of the pandemic on the stock market in other studies, the data set of the analysis period is considered as a whole; in this study, it is examined by sub periods to take into account whether or not the said effect has changed in line with the new information announced.

The first part of the study includes data and methods used; the second part consists of empirical results; whereas the third part presents the conclusion and suggestion for future studies.

Data and Methods

Data

In this study, the daily data set of the COVID-19 outbreak and stock closing prices were used. A delay was taken for the variables (death, case, and bed) used for COVID-19, considering Ashraf’s (2020) study. The time frame for the data is between December 31, 2019 and November 10, 2020. The variables are used in logarithmic form. Four countries, namely, the United States, Germany, China, and India, were selected for the study. Some criteria have been considered in the selection of these countries. The first of these criteria is made according to the development levels of the countries. Accordingly, the United States and Germany are in the developed country group, and China and India are in the rising economy group. A classification was made to assess whether the bed capacity is sufficient for the increasing number of cases in these countries, as an indicator of the strength of the health care system. According to this classification, the higher number of cases in some countries (USA and India) and the lower numbers in others (China and Germany) were considered. The information about the data appears in Table 1; descriptive statistics are included in Table 2.

Table 1. Summary of the Data

|

Variables |

Explanation |

Source |

|

Stock |

Stock market closing prices |

Investing. com |

|

Death |

Mortality rate = Number of deaths / Number of cases |

(European Centre for Disease Prevention and Control, 2020) |

|

Case |

Case Rate = Number of cases / Total population |

(European Centre for Disease Prevention and Control, 2020) |

|

Bed |

Bed Capacity = Number of beds / Number of cases |

(World Bank, 2020)/ (European Centre for Disease Prevention and Control, 2020) |

Table 2. Descriptive Statistics

|

China |

Germany |

|||||||

|

Stock |

Death |

Case |

Bed |

Stock |

Death |

Case |

Bed |

|

|

Mean |

3071.7 |

0.1555 |

2.17E-07 |

685768.5 |

12000.4 |

0.2522 |

1.06E-05 |

148055.5 |

|

Med. |

3019.5 |

0.0487 |

2.09E-08 |

205986.9 |

12488.4 |

0.0463 |

4.88E-06 |

1638.424 |

|

Max. |

3451.1 |

2.0000 |

1.06E-05 |

6179608. |

13789.0 |

1.0000 |

7.42E-05 |

664153.7 |

|

Min. |

2660.2 |

0.0000 |

6.97E-10 |

408.1104 |

8441.71 |

0.0007 |

1.20E-08 |

107.8697 |

|

S. D. |

218.29 |

0.2780 |

8.44E-07 |

1442015. |

1362.17 |

0.3879 |

1.54E-05 |

267038.9 |

|

Skew. |

0.1394 |

3.0207 |

9.117112 |

3.147361 |

-0.72649 |

1.3408 |

2.233847 |

1.363985 |

|

Kurt. |

1.5995 |

14.007 |

106.6378 |

11.97060 |

2.46304 |

2.9269 |

7.651700 |

2.944571 |

|

J-B. |

18.353 |

1418.9 |

99659.51 |

1080.857 |

17.1963 |

51.570 |

298.1233 |

53.35509 |

|

Prob. |

0.0001 |

0.0000 |

0.000000 |

0.000000 |

0.00018 |

0.0000 |

0.000000 |

0.000000 |

|

Sum |

663493.2 |

33.593 |

4.69E-05 |

1.48E+08 |

2064060. |

43.377 |

0.001828 |

25465542 |

|

Obs. |

216 |

216 |

216 |

216 |

222 |

222 |

222 |

222 |

|

USA |

India |

|||||||

|

Stock |

Death |

Case |

Bed |

Stock |

Death |

Case |

Bed |

|

|

Mean |

3146.91 |

0.1973 |

9.01E-05 |

6098.827 |

36583.13 |

0.2268 |

1.92E-05 |

152527.0 |

|

Med. |

3237.18 |

0.0286 |

8.16E-05 |

1.320066 |

37981.63 |

0.0247 |

6.52E-06 |

81.27962 |

|

Max. |

3580.84 |

1.0000 |

0.000369 |

35454.33 |

42597.43 |

1.0000 |

7.16E-05 |

724201.4 |

|

Min. |

2237.40 |

0.0053 |

3.04E-09 |

0.292014 |

25981.24 |

0.0100 |

7.32E-10 |

7.397812 |

|

S. D. |

282.778 |

0.3552 |

7.41E-05 |

12929.00 |

4115.882 |

0.3876 |

2.26E-05 |

286744.4 |

|

Skew. |

-1.02993 |

1.7305 |

0.57664 |

1.763469 |

-0.574402 |

1.4484 |

0.803949 |

1.447139 |

|

Kurt. |

3.45603 |

4.1427 |

3.09765 |

4.218223 |

2.140034 |

3.1733 |

2.161314 |

3.166718 |

|

J-B. |

40.6155 |

121.22 |

12.2239 |

127.0506 |

18.96265 |

77.548 |

30.28374 |

77.39272 |

|

Prob. |

0.00000 |

0.0000 |

0.00221 |

0.000000 |

0.000076 |

0.0000 |

0.000000 |

0.000000 |

|

Sum |

689173.6 |

43.213 |

0.01973 |

1335643. |

8084871. |

50.127 |

0.004243 |

33708464 |

|

Obs. |

219 |

219 |

219 |

219 |

221 |

221 |

221 |

221 |

A two-stage process was followed to examine the dynamic relationships between COVID-19 and stock market variables. In the first stage, a time-varying symmetric causality test based on Hacker and Hatemi-J’s (2006) research was performed, whereas in the second stage, a time-varying asymmetric causality test developed according to Hatemi-J (2012) was performed.

Time-Varying Causality Tests

Many structural changes, such as economic and political events, can take the relationship between variables to different dimensions. For this reason, many authors (such as Arslantürk, et al., 2011; Balcılar & Özdemir, 2013; Inglesi-Lotz, et al., 2014; Yılancı & Bozoklu, 2014; Zeren & Koç, 2016; Jammazi, et al., 2017; Kanda, et al., 2018; Erdoğan, et al., 2019) have emphasized the importance of time-varying analysis methods when examining the relationships between macroeconomic variables.

Because of the traditional VAR model framework, commonly used test statistics such as the Wald, likelihood ratio (LR), and Lagrange multiplier (LM) test used to measure Granger causality can have nonstandard asymptotic properties if variables considered in VAR are integrated or cointegrated. To overcome this problem, Toda and Yamamoto (1995) and Dolado and Lütkepohl (1996) proposed a solution that guarantees standard asymptotic distribution for Wald tests performed on coefficients of VAR (p) processes where variables are at the level of I (1). These solutions require that at least one coefficient matrix be unconstrained under the null hypothesis. The time-varying causality test used in the present study is based on the bootstrap causality test developed by Hacker and Hatemi-J (2006) based on the causality test of Toda and Yamamoto (1995). In order to test bootstrap LR Granger causality, the bivariate basic VAR (p) model was defined as follows (Balcilar, et al., 2010):

(1)

(1)

In the model, while  n-dimensional vectors,

n-dimensional vectors,  was expressed as the n × n matrix of the parameters obtained for p delay,

was expressed as the n × n matrix of the parameters obtained for p delay,  defined the nonsingular covariance matrix and the zero-mean independent white noise process. Here the p lag length was determined according to Akaike Information Criteria (AIC).

defined the nonsingular covariance matrix and the zero-mean independent white noise process. Here the p lag length was determined according to Akaike Information Criteria (AIC).

Toda and Yamamoto (1995) proposed an extended VAR (p + d) model to test the causality relationship between integrated variables:

(2)

(2)

In the model, p represented the optimal lag length, and d represented the maximum degree of integration. Before making an estimate, some definitions were made for the sample size T. Here the  matrix

matrix  matrix is expressed as follows:

matrix is expressed as follows:

,

,  matrix

matrix

,

, and

and  ,

,  was defined as the matrix; in line with this information, the VAR

was defined as the matrix; in line with this information, the VAR model estimated could be expressed as follows:

model estimated could be expressed as follows:

(3)

(3)

In summary, the modified Wald test (MWALD) by Toda and Yamamoto (1995) to test Granger causality between variables was defined as follows:

(4)

(4)

In the equation, Θ, the Kronecker factor, and  make up a matrix.

make up a matrix.  as

as and

and

Hacker and Hatemi-J (2006) suggested that if the MWALD test, which has an χ2 distribution, were performed by using the bootstrap technique, it could eliminate some problems (such as misleading results if the correct size was not provided in a finite sample). Thus, more reliable critical values could be obtained, and deviations in estimation could be reduced.

The basis of the causality method that changes over time was the method developed by Hacker and Hatemi-J (2006). However, although Hacker and Hatemi-J (2006) took into account the entire sample in the causality test, the subperiods of the sample were taken into account in the causality test that changed over time. Thus, a causality test was applied to each subperiod.

The important factor in this method was to determine the length (number of windows) of the subperiod as stated by Brooks and Hinich (1998). Accordingly, the number of windows was determined based on Caspi’s (2017) study. The number of windows of the study was determined to be 29 when using the formula T (0.01 + 1.8 / √T).

Then, the following stages were followed for the implementation of the method: in the first stage, the Hacker and Hatemi-J (2006) causality test was applied for the interval from the first observation to the 29th observation. In the second stage, the first observation was discarded; this test was applied to the observation interval with the second observation (29 + 1), and the test was continued until the last observation in the data range was used by making the first observation at each new stage and adding a new observation to the last observation. To test the significance of these results, the test statistic obtained at each observation interval was normalized with the bootstrap critical value. The point to be emphasized here is that not only the Wald test statistics but also the bootstrap critical values changed with time. Therefore, the test statistic obtained at each observation interval would be normalized with the 10% bootstrap critical value obtained during this observation interval. The periodic test statistic value for each subperiod was calculated as follows:

(5)

(5)

The values were plotted to interpret the resulting Wald test statistics. In this graph, there is a causality relationship between the periods when these test statistics values were greater than 1 (Erdoğan et al., 2019; Yılancı & Bozoklu, 2014).

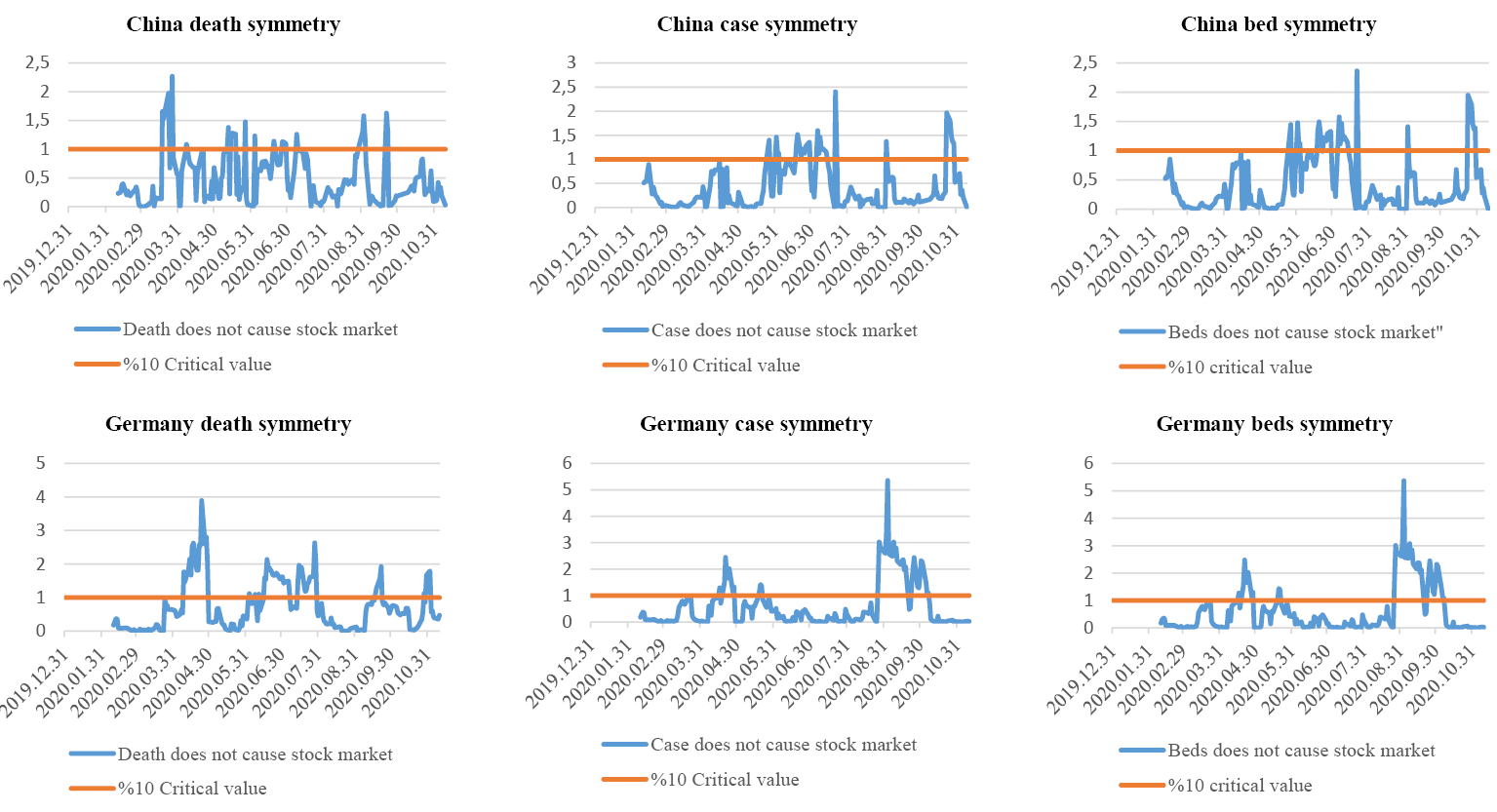

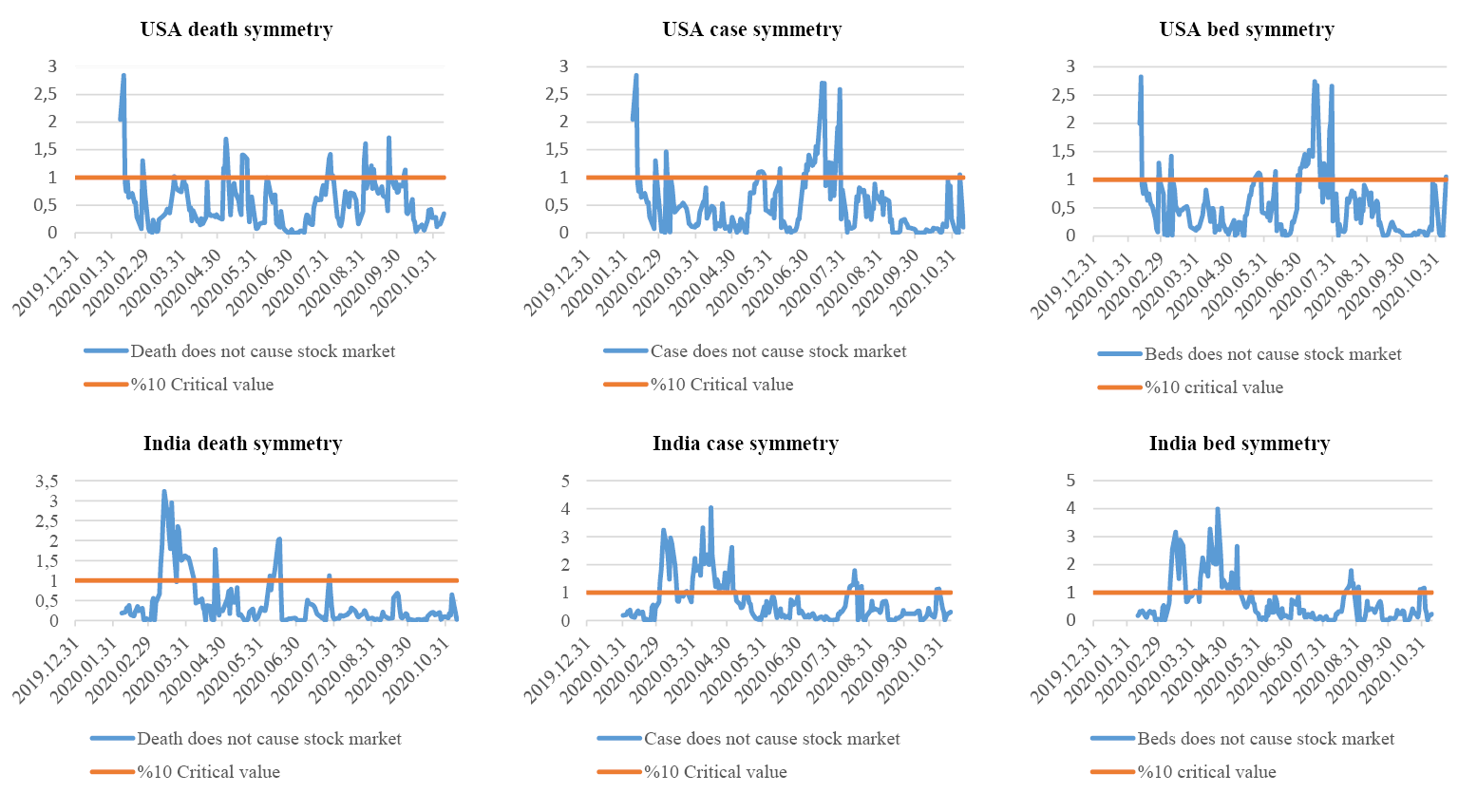

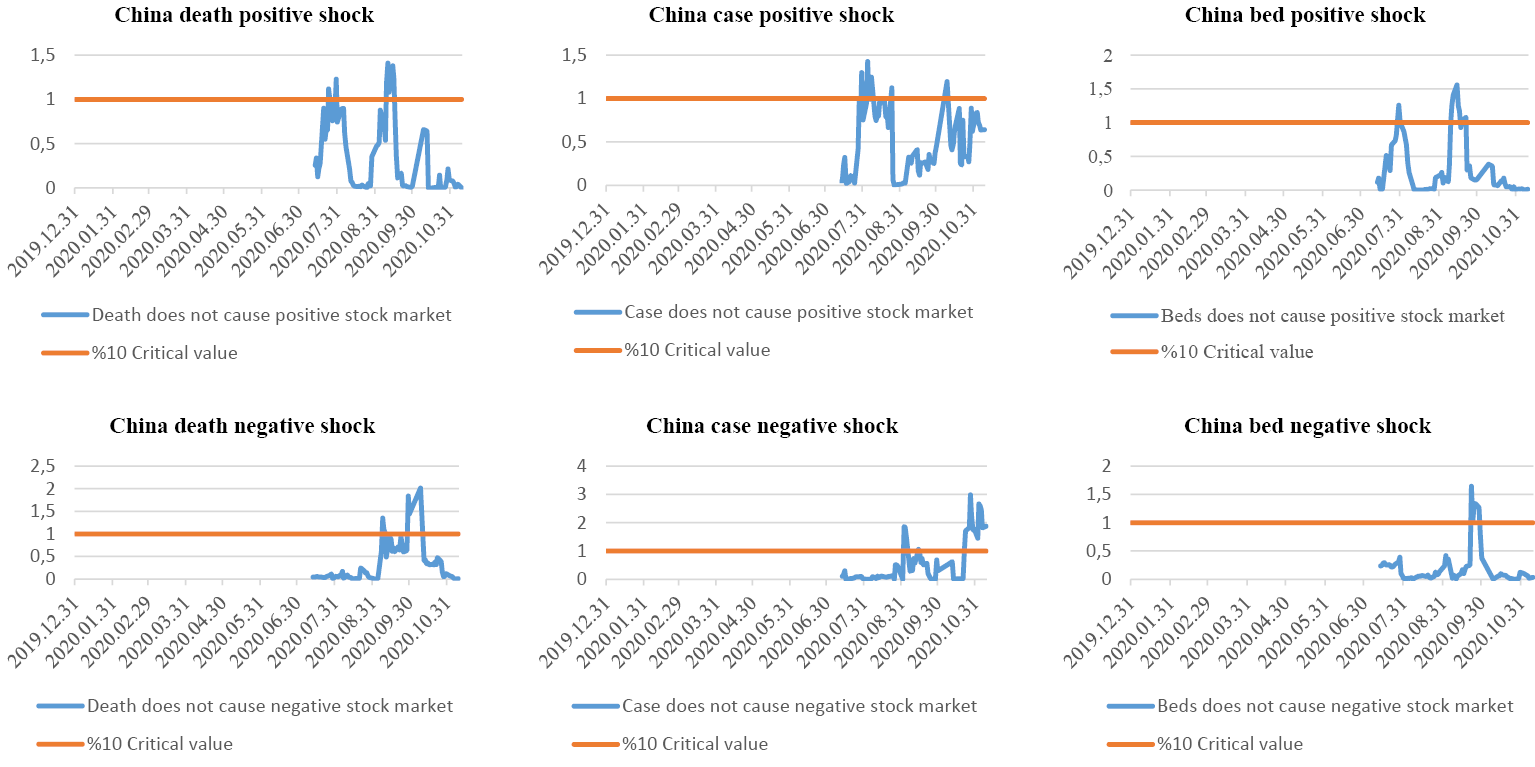

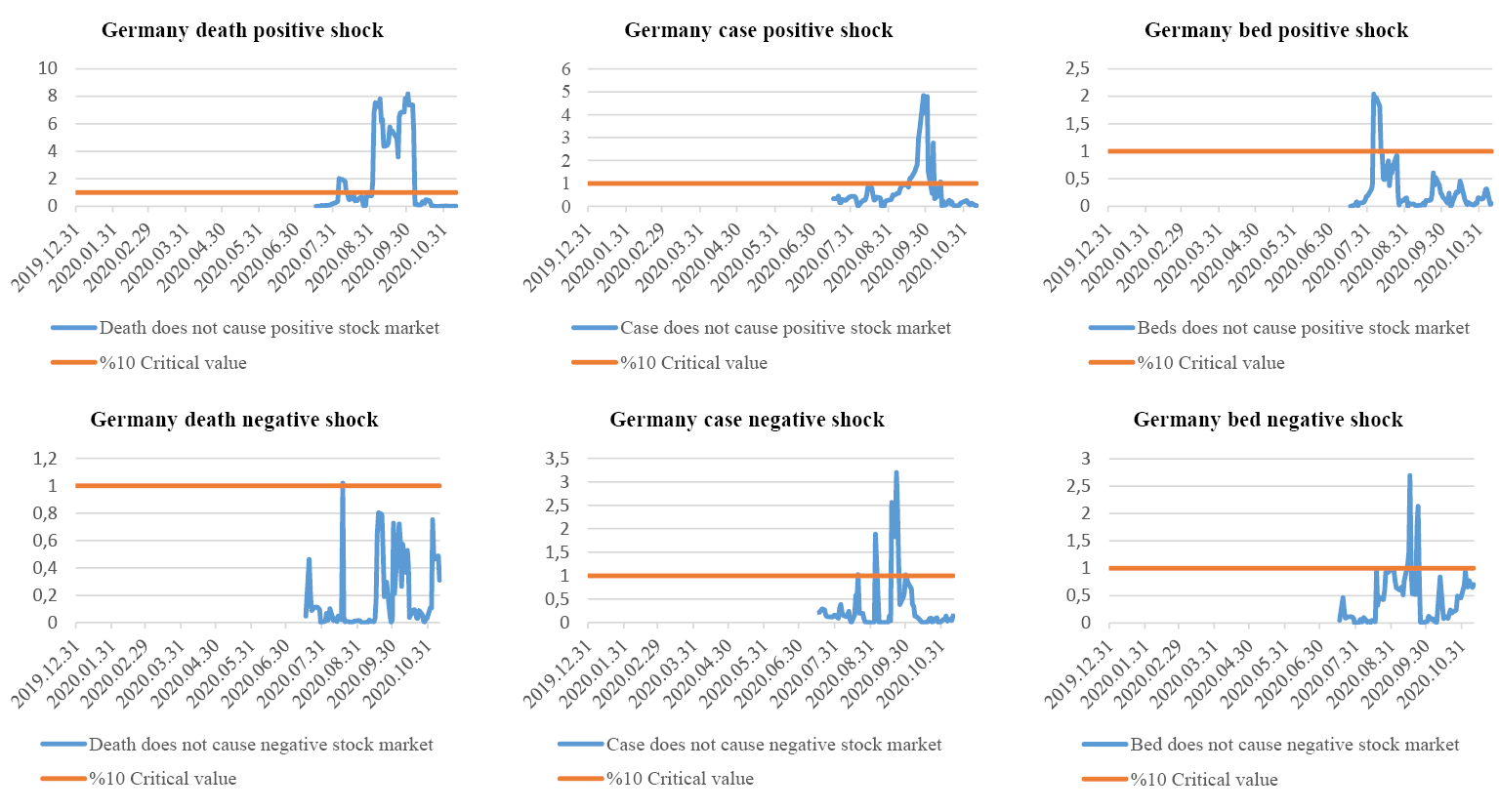

Graph 1. Time Varying Symmetric Causality Test Results

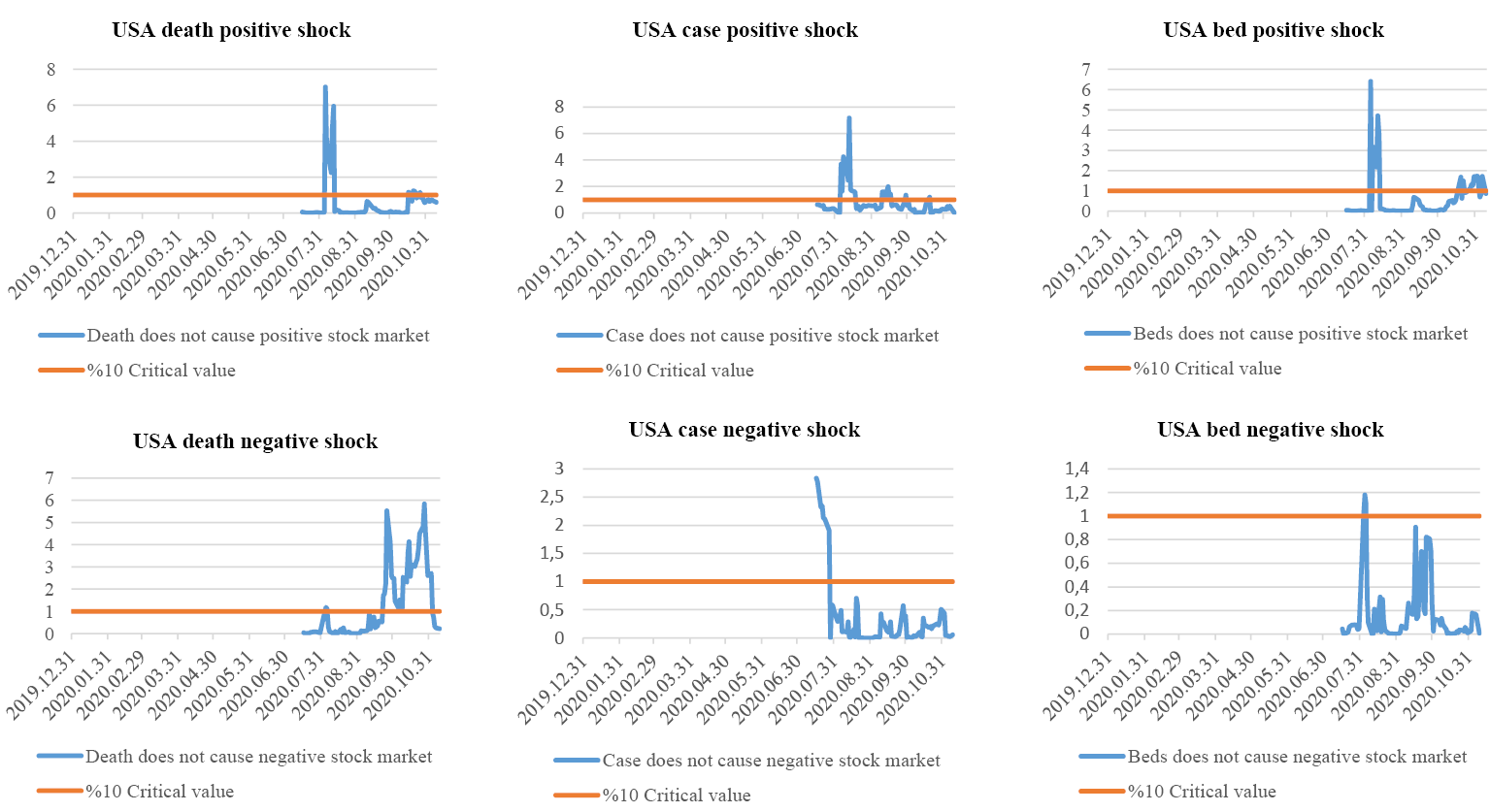

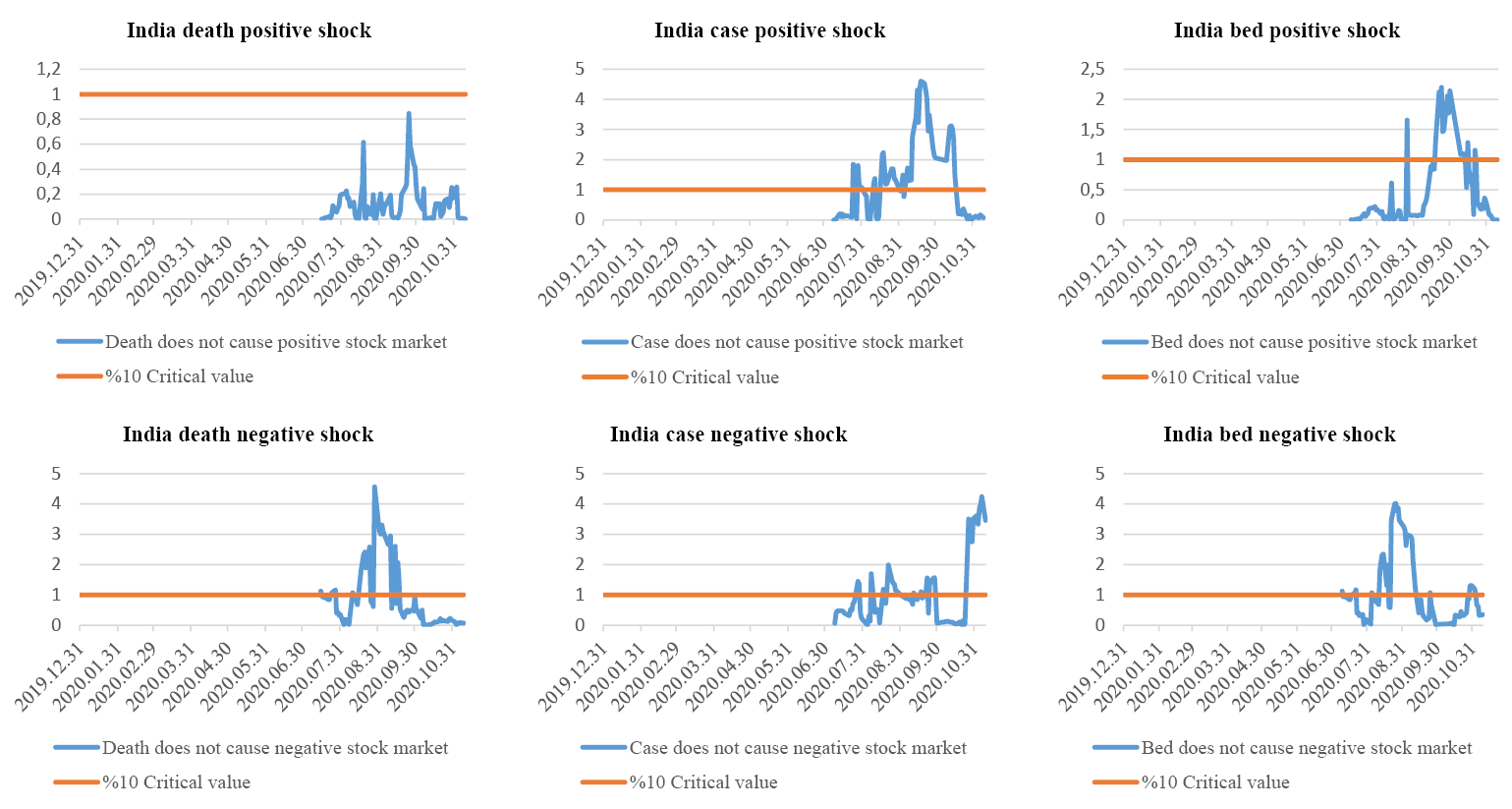

Empirical Results: Time-Varying Symmetric Causality Test. According to the findings of the causality test, which changed over time, the stock markets were affected in all countries when the cases first appeared. The first official data on COVID-19 in China were cases on December 31 and deaths on January 11. However, the effects of COVID-19 on the stock market emerged about one month later. Based on the auxiliary variables used to measure the impact of the pandemic in China, a causality relationship was found on these dates for death (February 7–September 22), case (April 14–October 29) and bed (April 14–September 2). The first official data on COVID-19 in Germany were a case on January 28 and deaths on March 10. The effects of these variables on the stock market coincided with death (March 2–November 2), case (March 9–October 7), and bed (March 9–October 7). Therefore, it can be extrapolated that the German stock exchange is affected not only by country-specific news but also by news from other countries. The first official data on COVID-19 for the United States were case (January 21) and death (March 1). The reaction of the U.S. stock market to the pandemic coincided with the first official figures announced in China when the pandemic started. Thus, the causality relationship for the United States manifested as death (December 31–October 7), case (December 31–November 6), and bed (December 31–November 6). The first official data on COVID-19 for India were case (January 30) and death (March 13). The reaction of the Indian stock market to COVID-19 occurred instantly. Therefore, the causality relationship coincides with death (January 30–July 27), case (January 23–August 24), and bed (January 31–November 9). In addition, the causality relationship among countries differs in terms of bed capacity. Although the number of case and bed affected the stock markets of Germany and the United States on the same dates, these dates differed for China and India. The sudden increase in the number of case due to the pandemic in Germany and the United States compared with other countries and the relatively high elderly population affected how this situation manifested itself.

Time-Varying Asymmetric Causality Test

Tests developed for causality analysis (Hacker & Hatemi, 2006; Hsiao, 1981; Sims, 1972; Toda & Yamamoto, 1995) accept that the effect of positive shocks is the same as the effect of negative shocks. However, in financial markets, in the presence of asymmetric information and the heterogeneity of market participants, positive and negative shocks of the same magnitude do not draw similar reactions. In this case, the results obtained from the aforementioned tests can be misleading. It was first suggested by Granger and Yoon (2002) that the relationship between positive and negative shocks could differ from the relationship between variables. The researchers stated that the economic series are cointegrated when they react to shocks together; when they react separately, there cannot be a cointegration relationship between them. Therefore, they separated the data into cumulative positive and negative changes and examined the long-term relationship between these parts. Hatemi-J (2012) adapted the Granger and Yoon (2002) approach for causality analysis. The aim of this asymmetric causality test is to find the hidden structure that will help illustrate the dynamics of the series as in the cointegration analysis of Granger and Yoon (2002) and allow the development of predictions for the possible future. Hatemi-J (2012) defined the two series  and

and  , whose causality relationship is investigated, as follows:

, whose causality relationship is investigated, as follows:

(1)

(1)

(2)

(2)

and

and  in the definition of the variable indicate their initial values, while

in the definition of the variable indicate their initial values, while  and

and  within the variables indicate the total shocks. These shocks are defined as follows:

within the variables indicate the total shocks. These shocks are defined as follows:

,

,

(3)

(3)

The relationship can be indicated as  and

and  . If

. If  and

and  variables are redefined, they become

variables are redefined, they become

(4)

(4)

The positive and negative shocks in each variable are expressed in Equation (5) in the cumulative form.

,

,  ,

,  ,

, , (5)

, (5)

where  indicates positive shocks of the first variable,

indicates positive shocks of the first variable,  indicates negative shocks of the first variable,

indicates negative shocks of the first variable,  indicates positive shocks of the second variable, and finally,

indicates positive shocks of the second variable, and finally,  indicates negative shocks of the second variable.

indicates negative shocks of the second variable.

In this study, the stability of the causality relationship between positive and negative shocks will be tested using the time-varying form of the asymmetric causality test developed by Hatemi-J (2012). The subsample size for the asymmetric causality analysis that changes over time is 29, as in the symmetric analysis. Subsequent operations are repeated as in the symmetric analysis. In addition, the appropriate delay length in this study was decided using the information criterion contributed by Hatemi-J (2003), and an additional delay was added to the VAR model, which was determined according to this appropriate delay length, following the suggestion of Dolado and Lütkopohl (1996).

Empirical Results: Time-Varying Asymmetric Causality Test. The method used here allows the detection of negative shocks (positive: decrease in the number of case and death) and positive shocks (negative: increase in the number of case and death) as positive shocks (increase in the stock market) and negative shocks (decrease in the stock market), respectively, during the COVID-19 pandemic period. Although these positive and negative developments and their effects on negative and positive shocks of countries appear in detail in Appendix Tables A.1 and A.2, they are summarized here in general terms.

The positive developments experienced globally during the pandemic process generally cause positive shocks in the stock markets of the countries subject to analysis. The positive development experienced in this process are as follows: statements were made that serious progress has been made in vaccination studies, and with the discovery of new information about the structure of the virus, public awareness was raised regarding the importance of masks, hygiene, and maintaining distance in combating the virus.

Negative global developments caused negative shocks in the stock markets of some countries. These negative developments can be summarized as follows: the number of cases began to increase rapidly as countries loosened measures due to economic concerns, although a solution to the pandemic had not been found, and people did not take the virus seriously. With these increases, it was reported that a second wave would occur and that this would be even more severe. Concerns were raised about whether the proposed vaccines would be effective as well as what their side effects would be. Uncontrollable increases in the number of cases raised concerns that the health system would not be successful in combating the pandemic because of the insufficient number of beds, the inadequacy of health care workers, and the increase in the number of cases among health care professionals. The increases in the number of case and death increased fear among the people. In addition, one of the important developments that would cause these negative shocks was the U.S. president’s statements that he would withdraw his support from the WHO because of the tension between the United States and the WHO.

Graph 2. Time Varying Asymmetric Causality Test Results

The reasons for the positive and negative shocks experienced could stem from global developments as well as from country-specific developments during the pandemic process. These developments are summarized according to country (China, Germany, the United States, and India).

When the results of the asymmetric causality test were evaluated, it was revealed that while positive developments experienced on a global scale in the fight against the pandemic caused positive shocks for each country, the positive developments specific to the country also affected the positive shocks. Accordingly, China, the country where the pandemic first occurred, gained experience earlier than the other countries in combating the pandemic. The positive atmosphere caused positive shocks in this country to emerge earlier than in other countries.

Although negative shocks in China were expected to emerge in the early periods, it was observed that the negative atmosphere originating from China did not create a negative shock for the Chinese stock market during this period. Therefore, it could be argued that the negative shocks that occurred in China were not caused by specific negative shocks but by negative developments around the world. China, the world’s most important exporting country, was able to cope with the pandemic in a short time. However, the negative atmosphere created by the global pandemic and the ensuing shrinking of the economies of the countries to which it exported were effective in creating the negative shocks on the Chinese stock market during this period. On a global scale, negative news such as the uncontrollable increase in the number of case and death, the increasing prospect that a perfect vaccine would not be possible, and the statement that Denmark would cull minks after the discovery of a new mutated coronavirus species could be given as the sources of negative shocks in China.

The positive shocks affecting Germany in the period subject to analysis stemmed from the positive developments in the world and Europe. This process coincided with the period when the severity of the pandemic decreased, and normalization steps were taken in European countries. These positive developments were mainly the result of EU countries’ starting to relax their COVID-19 measures by opening their borders to 15 countries in early July, 2020. In addition, leaders of EU countries agreed to provide aid packages to reduce the devastating effects of the pandemic on the economy.

During the process of combating the pandemic in Germany, there were positive developments that created positive shocks, but also negative developments that caused negative shocks. The negative developments that caused negative shocks can be summarized as follows: an uncontrollable increase in the number of cases in Europe, problems with medical equipment (such as masks and respiratory devices), and the probability that the health system would not be successful in its struggle against the pandemic. In particular, the insufficient numbers of bed and health care professionals as well as the rise in cases among health care workers increased concerns.

In addition to the positive shocks arising from the positive developments in the world, the positive developments experienced specifically in the United States have been a source of these positive shocks. Some of the positive developments experienced specifically in the United States in the current periods can be summarized as follows: allowing plasma therapy for COVID-19 patients, the recovery of the U.S. president from the coronavirus, the U.S. Food and Drug Administration’s (FDA) approval of the use of the antiviral drug Remdesivir in the treatment of COVID-19.

The negative developments that caused negative shocks can be summarized as follows: the United States ranking first in number of cases as a result of the rampant spread of the virus, problems related to medical equipment (such as masks and respiratory devices); general elections in the United States; expectations that the health care system would be unsuccessful in combating the pandemic due to the inadequate number of beds; the limited number of health care workers; and the escalation in the number of cases among health care professionals.

No positive developments occurred to create a positive shock specific to India. As in China, positive shocks in India stemmed from positive developments on the global scale. The pandemic emerged in India after China, Germany, and the United States, and the experiences of these countries in combating the pandemic (the effectiveness of some medicines in the treatment of the corona virus, the application of plasma therapy, etc.) were perceived as positive developments, causing the emergence of positive shocks.

The source of the negative shocks in India was the fear that the second worldwide wave would occur just as the pandemic was starting in the country. This would cause the number of cases to increase in a noticeably short time, and India would jump to second place in the number of cases after the United States. Therefore, the inadequacy of the current health care system increased negative expectations that India would not be able to prevent the number of cases from increasing.

Conclusion

In this study, the time-varying causality and asymmetric causality relationship between COVID-19 (case rate, mortality rate, and bed capacity) and stock market closing prices in selected countries (United States, Germany, China, and India) was investigated. We have analyzed this relationship, considering that it may change over time and that the responses to negative and positive shocks in the relevant variables may differ.

Two waves were noted by the WHO during the period under analysis. The date of the first wave of the pandemic fell to June, when countries entered a period of normalization; the second wave covered the period when the cases increased again after the normalization process.

In this study, the causality relationship between COVID-19 and the stock markets of selected countries was tested symmetrically and asymmetrically. According to the findings of the causality test that changes over time, the virus affected the stock markets in all countries when cases first appeared. We have found a causality relationship between the countries’ stock markets and the auxiliary variables (death, cases, and beds) we used to measure the impact of COVID-19 in the countries included in the analysis. The study has also shown that the causality relationship changes over time, so the frequency and persistence of the relationship would also differ for distinct shocks. According to the asymmetric causality findings that change over time, the asymmetric effect of the pandemic on the stock market in countries emerged during the second wave. The effect of COVID-19 (case rate, mortality rate, and bed capacity) on the stock market changed over time in the countries subject to the analysis (except for the negative shock of the number of deaths in India).

The findings in other studies in the literature (Özparlak, 2020; Topçu & Gülal, 2020; Baek et al., 2020; Khan et al., 2020; Ashraf, 2020; Al-Awadhi et al., 2020; and He et al., 2020) were similar to those of this study. Zeren and Hızarcı (2020), Barut and Yerdelen Kaygın (2020), and Hacıevliyagil and Gümüş (2020) found a relationship between the stock markets of some countries and the cases and mortality, but not for other countries.

Although the findings in this study support the findings of other studies in the literature, the effect of COVID-19 on the stock market appeared to be short term. Given that the method used has a more advanced technique than the methods used in other studies, it reveals the reaction time to shocks and the type of shock, making the findings of this study remarkable. The major contribution of this study has been to examine whether psychological factors such as panic and fear that occur when the bed capacities of countries are insufficient in the face of increasing cases could influence the stock market. Thus, the periods in which this effect occurred (or not) were analyzed.

Besides the death (mortality rate) and case (case rate) variables used in the literature, when the effects of the information on bed capacity on the stock market were evaluated according to the efficient market hypothesis, it arose that whereas the reaction of the market to official information about COVID-19 was delayed in China, in other countries, its effect on the stock market was immediate. In line with this information, the stock markets of other countries have stronger structures than that of the Chinese market, which is in the medium-strong form.

As this study was carried out while the pandemic process and the effects continued, it could be analyzed by increasing the number of countries and diversifying financial and economic indicators in the subsequent studies.

References

Al-Awadhi, A. M., Alsaifi, K., Al-Awadhi, A., & Alhammadi, S. (2020). Death and Contagious Infectious Diseases: Impact of the COVID-19 Virus on Stock Market Returns. Journal of Behavioral and Experimental Finance, 1-5. https://dx.doi.org/10.1016%2Fj.jbef.2020.100326

Alfaro, L., Chari, A., Greenland, A., & Schott, P. K. (2020). Aggregate and Firm-Level Stock Returns During Pandemics, in Real Time. National Bureau of Economic Research, 1-31.

Arslanturk, Y., Balcilar, M., & Ozdemir, Z. (2011). Time-Varying Linkages between Tourism Receipts and Economic Growth in a Small Open Economy. Econ. Modell. 28(1), 664–671.

Ashraf, B. N. (2020). Stock Markets’ Reaction to COVID-19: Cases or Fatalities? Research in International Business and Finance, 1-7. https://dx.doi.org/10.1016%2Fj.ribaf.2020.101249

Baek, S., Mohanty, S. K., & Glambosky, M. (2020). COVID-19 and Stock Market Volatility: An Industry Level Analysis. Finance Research Letters, 37, 1-10. https://dx.doi.org/10.1016%2Fj.frl.2020.101748

Baker, S. R., Bloom, N., Davis, S. J., Kost, K., Sammon, M., & Viratyosin, T. (2020). The Unprecedented Stock Market Reaction to COVID-19. Review of Asset Pricing Studies, 1-17.

Balcilar, M., Ozdemir, Z. A., & Arslanturk, Y. (2010). Economic Growth and Energy Consumption Causal Nexus Viewed Through a Bootstrap Rolling Window. Energy Economics, 32(6), 1398–1410. https://doi.org/10.1016/j.eneco.2010.05.015

Balcilar, M., & Ozdemir, Z. (2013). Asymmetric and Time-Varying Causality between Inflation and Inflation Uncertainty in G-7 Countries. J. Political Econ., 60(1), 1–42. https://doi.org/10.1111/sjpe.12000

Barut, A., & Yerdelen Kaygın, C. (2020). Examining the Impact of COVID-19 Pandemics upon Selected Share Indices (COVID-19 pandemisinin seçilmiş borsa endeksleri üzerine etkisinin incelenmesi). Gaziantep University Journal of Social Sciences 2020 Special Issue, 59-70. http://dx.doi.org/10.21547/jss.773237

Brooks, C., & Hinich, M. (1998). Episodic Nonstationarity in Exchange Rates. Appl. Econ. Lett., 5(11), 719–722. https://doi.org/10.1080/135048598354203

Caspi, I. (2017). Rtadf: Testing For Bubbles with Eviews. Journal of Statistical Software, 81(1), 1-16. http://dx.doi.org/10.18637/jss.v081.c01

Dolado, J., & Lütkepohl, H. (1996). Making Wald Tests Work for Cointegrated VAR Systems. Econometric Theory, 15(4), 369-386. https://doi.org/10.1080/07474939608800362

Erdem, O. (2020). Freedom and Stock Market Performance during COVID-19 Outbreak. Finance Research Letters, 36, 1-6. https://dx.doi.org/10.1016%2Fj.frl.2020.101671

Erdoğan, S., Gedikli, A., & Kırca, M. (2019). A Note on Time-Varying Causality between Natural Gas Consumption and Economic Growth in Turkey. Resources Policy, 64, 1-7.

European Centre for Disease Prevention and Control. (2020). COVID-19 Situation Update Worldwide, as of 11 December 2020. European Centre for Disease Prevention and Control, https://www.ecdc.europa.eu/en/geographical-distribution-2019-ncov-cases/. Accessed November 11, 2020.

Fama, E. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. J. Financ., 25, 383–417. https://doi.org/10.1111/j.1540-6261.1970.tb00518.x

Gormsen, N. J., & Koijen, R. S. (2020). Coronavirus: Impact on Stock Prices and Growth Expectations. Chicago Üniversitesi, Becker Friedman Institute for Economics Working Paper.

Granger, C. (1969). Investigating Causal Relations by Econometric Models and Crossspectral Methods. Econometrica , 37(3), 424–438.

Granger, C., & Yoon, G. (2002). Hidden Cointegration. Department of Economics Working Paper University of California, No:2002-02.

Hacıevliyagil, N., & Gümüş, A. (2020). Epidemic Disease-Stock Market Relationship in Most Affected COVID-19 Countries (COVID-19’un en etkili olduğu ülkelerde salgın-borsa ilişkisi). Gaziantep University Journal of Social Sciences 2020 Special Issue, 354-364.

Hatemi-J, A. (2003). A New Method to Choose Optimal Lag Order in Stable and Unstable VAR Models. Applied Economics Letters, 10(3), 135-137. https://doi.org/10.1080/1350485022000041050

Hacker, R., & Hatemi-J, A. (2006). Tests for Causality between Integrated Variables Using Asymptotic and Bootstrap Distributions: Theory and Application. Appl. Econ., 38(13), 1489–1500. https://doi.org/10.1080/00036840500405763

Hatemi-J, A. (2012). Asymmetric Causality Tests with an Application. Empirical Economics, 43(1), 447-456.

He, Q., Liu, J., Wang, S., & Yu, J. (2020). The Impact of COVID-19 on Stock Markets. Economic and Political Studies, 8(3), 275-288. https://doi.org/10.1080/20954816.2020.1757570

Hsiao, C. (1981). Autoregressive Modelling and Money-Income Causality Detection. Journal of Monetary Economics, 7(1), 85-106. https://doi.org/10.1016/0304-3932(81)90053-2

Inglesi-Lotz, R., Balcilar, M., & Gupta, R. (2014). Time-Varying Causality between Research Output and Economic Growth in US. Scientometrics, 100(1), 203–216. https://doi.org/10.1007/s11192-014-1257-z

Jammazi, R., Ferrer, R., Jareño, F., & Shahzad, S. (2017). Time-Varying Causality Between Crude Oil and Stock Markets: What Can We Learn from a Multiscale Perspective? Int. Rev. Econ. Financ., 49, 453–483.

Kanda, P., Burke, M., & Gupta, R. (2018). Time-Varying Causality between Equity and Currency Returns in the United Kingdom: Evidence from over Two Centuries of Data. Physica A: Statistical Mechanics and its Applications, 506, 1060–1080. https://doi.org/10.1016/j.physa.2018.05.037

Khan, K., Zhao, H., Zhang, H., Yang, H., Shah, M. H., & Jahange, A. (2020). The Impact of COVID-19 Pandemic on Stock Markets: An Empirical Analysis of World Major Stock Indices. Journal of Asian Finance, Economics and Business, 7(7), 463 – 474. https://doi.org/10.13106/jafeb.2020.vol7.no7.463

Liu, H., Manzoor, A., Wang, C., Zhang, L., & Manzoor, Z. (2020). The COVID-19 Outbreak and Affected Countries Stock Markets Response. International Journal of Environmental Research and Public Health, 17, 1-19.

Lyócsa, Š., Baumöhl, E., Výrostde, T., & Molnár, P. (2020). Fear of the Coronavirus and the Stock Markets. Finance Research Letters, 36, 1-7. https://dx.doi.org/10.1016%2Fj.frl.2020.101735

Machmuddah, Z., Utomo, S. D., Suhartono, E., Ali, S., & Ghulam, W. A. (2020). Stock Market Reaction to COVID-19: Evidence in Customer Goods Sector with the Implication for Open Innovation. J. Open Innov. Technol. Mark. Complex, 6(99), 1-13. https://doi.org/10.3390/joitmc6040099

Mishra, A. K., Rath, B. N., & Dash, A. K. (2020). Does The Indian Financial Market Nosedive Because of the COVID-19 Outbreak, In Comparison to After Demonetisation and The GST? Emerging Markets Finance and Trade, 2162-2180. https://doi.org/10.1080/1540496X.2020.1785425

Narayan, P., Phan, D., & G.Liu. (2020). Covid-19 Lockdowns, Stimulus Packages, Travel Bans, and Stock Returns. Finance Research Letters, 1-7. https://dx.doi.org/10.1016%2Fj.frl.2020.101732

OECD. (2020). Global Financial Markets Policy Responses to COVID-19. Paris: OECD.

Okorie, D., & Lin, B. (2020). Stock Markets and the COVID-19 Fractal Contagion Effects. Finance Research Letters, 1-8.

Onali, E. (2020). COVID-19 and Stock Market Volatility. SSRN, 1-24. https://ssrn.com/abstract=3571453/. Accessed September 22, 2020.

Özparlak, G. (2020). Long and Short Run Impact of COVID-19 on Financial Markets. Journal of Business, Economics and Finance (JBEF), 9(2), 155-170. https://doi.org/10.17261/Pressacademia.2020.1221

Sharif, A., Aloui, C., & Yarovaya, L. (2020). COVID-19 Pandemic, Oil Prices, Stock Market, Geopolitical Risk and Policy Uncertainty Nexus in the Us Economy: Fresh Evidence from the Wavelet-Based Approach. International Review of Financial Analysis, 70, 1-9. https://dx.doi.org/10.1016%2Fj.irfa.2020.101496

Sims, C. (1972). Money, Income, and Causality. American Economic Review, 62(4), 540-552.

Toda, H., & Yamamoto, T. (1995). Statistical Inference in Vector Autoregressions with Possibly Integrated Processes. J. Econom., 66(1), 225–250. https://doi.org/10.1016/0304-4076(94)01616-8

Topcu, M., & Gülal, Ö. S. (2020). The Impact of COVID-19 on Emerging Stock Markets. Finance Research Letters, 1-4. https://doi.org/10.1016/j.frl.2020.101691

Wagner, A. F. (2020). What the Stock Market Tells Us About the Post- COVID-19 World. Nature Human Behaviour, 4, 440.

WHO. (2020). World Health Organization. https://www.who.int/emergencies/diseases/novel-coronavirus-2019/. Accessed September 10, 2020

World Bank. (2020, November 11). Hospital beds (per 1,000 people). https://data.worldbank.org/indicator/SH.MED.BEDS.ZS/. Accessed September 10, 2020

Yılancı, V., & Bozoklu, Ş. (2014). Price and Trade Volume Relationship in Turkish Capital Market: Time-Varying Asymmetric Causality Analysis. Ege Akademik Bakis (Ege Acad.Rev.), 14(2), 211–220.

Zeren, F., & Hızarcı, A. E. (2020). The Impact of COVID-19 Coronavirus on Stock Markets: Evidence from Selected Countrıes. Muhasebe ve Finans İncelemeleri Dergisi, 3(1), 78-84. https://doi.org/10.32951/mufider.706159

Zeren, F., & Koç, M. (2016). Time Varying Causality between Stock Market and Exchange Rate: Evidence from Turkey, Japan and England. Econ. Res. Ekonomska Istraživanja , 29(1), 696–705. http://dx.doi.org/10.1080/1331677X.2016.1193950

Zhang, D., Hu, M., & Ji, Q. (2020). Financial Markets under the Global Pandemic of COVID-19. Finance Research Letters, 1-6. https://dx.doi.org/10.1016%2Fj.frl.2020.101528

Appendix

Table A.1. Positive shock dates

|

Variables |

News |

Positive shock dates |

|||

|

USA |

India |

China |

Germany |

||

|

Variables |

News |

Positive shock dates |

|||

|

USA |

India |

China |

Germany |

||

|

Death |

17 June: The number of cases worldwide exceeded 8 million 200 thousand, loss of life exceeded 446 thousand. 20 June: The number of cases worldwide exceeded 8 million 700 thousand and more than 15 thousand deaths in three days to total 461 thousand. 5 July: WHO announced that it has decided to terminate the experiments to determine whether hydroxychloroquine, known as a malaria drug, is beneficial for hospitalized Corona virus patients. 8 July: The Trump administration officially launched the process of withdrawal from WHO after the tension experienced during the Corona virus outbreak*. 16 July: The UK, USA and Canada accused Russia of attempting to steal data to develop a vaccine against the Corona virus. The Kremlin denied the accusation. 29 July: The number of Corona virus cases worldwide has approached 17 million. According to official statements, approximately 665 thousand people have lost their lives since the last week of December. 1 August: Corona virus measures taken by the German government in Berlin were protested by thousands of people*. 1 September: More than 500 thousand people applied for the Corona virus test campaign launched in Hong Kong. However, many Hong Kong residents are skeptical of this Chinese campaign and are concerned that DNA samples will be collected from Hong Kong residents*. 3 September: The number of cases has exceeded 26 million in the Corona virus outbreak worldwide. The pandemic has been encountered in more than 200 countries around the world, according to official data. At the end of eight months, more than 867 thousand people died worldwide. 5 September: In a study conducted in the USA, it was predicted that the loss of life in the country will reach 410 thousand by 1 January 2021*. 8 September: Nine leading vaccine manufacturers in America and Europe made a statement regarding their concerns that accelerated vaccination studies would bring new risks with them. 9 September: AstraZeneca announced that it had suspended global trials of the vaccine after one of the subjects participating in the vaccine study incurred an unexplained disease. 10 September: The number of casualties in the Corona virus pandemic exceeded 900 thousand and the number of people infected with the virus exceeded 28 million worldwide. 15 September: WHO stated that the number of cases would soon exceed 29 million worldwide, and the death toll would reach approximately one million. 20 September: The former head of the US Food and Drug Administration said that another pandemic was expected to occur in the country in autumn and winter*. 27 October: The US National Institute of Allergy and Infectious Diseases stated that a drug developed for corona treatment was not effective. |

between 25 June and 5 August between 11 August and 2 November |

between 5 June and 15 July between 16 June and 25 July between 1 July and 10 August between 8 July and 24 August between 21 July and 17 September |

between 29 July and 10 September between 19 August and 9 October |

between 7 July and 18 August |

|

Case |

22 June: WHO announced that there has been a record increase in the number of Corona virus cases worldwide. For the first time since the pandemic started, 183 thousand new cases were diagnosed in one day. 24 June: States in the USA took Corona measures against each other*. 27 June: The number of cases exceeded 10 million worldwide and the USA, where there were mor than 2 million 500 thousand, was the country most affected by the pandemic. 30 June: Anthony Fauci, president of the US National Institute of Allergy and Infectious Diseases, said cases are increasing rapidly in some areas and the US is “heading in the wrong direction”*. 3 July: In Latin America, the number of cases increased by approximately 600 thousand in the preceding week, reaching 2 million 734 thousand, surpassing the number of cases in Europe and becoming the region with the highest number of cases after the USA*. 6 July: India ranked third in highest number of cases in the world (surpassing Russia) with numbers approaching 700 thousand*. 11 July: WHO announced a record increase globally with 228 thousand 102 registered new cases in the previous 24 hours. 12 July: Florida broke the daily case number record with 15 thousand new cases. Accordingly, if Florida were a country, (with a total figure of over 300 thousand) it would be fourth highest in number of cases in the world, after the USA, Brazil and India*. 13 July: Approaching 145 thousand loss of life in Latin America exceeded the total number of fatalities in USA and Canada (144 thousand 28 deaths). 14 July: Due to the increase in the number of cases in the state of California, USA, the governorship decided to re-close bars, the indoor parts of restaurants, gyms and churches*. 17 July: After the USA and Brazil, the number of cases exceeded 1 million in India. 687 people had died in the preceding 24 hours*. 18 July: Highest case increase in 19 states in a day in the USA*. 19 July: WHO announced that the record had been broken by an increase of approximately 260 thousand in the number of cases over the previous 24 hours. 23 July: According to the data of the Reuters news agency, the number of Corona virus cases exceeded 4 million in the USA, where a total of 1 million cases was reached in 98 days. The number of cases increased from 3 million to 4 million in just 16 days*. 28 July: WHO says, “People still think of the virus as seasonal. What we all need to understand is that this is a new virus and it behaves differently and that the pandemic was accelerating again because the number of large meetings was on the rise.” 30 July: More than 50 thousand new cases of Corona virus were detected in one day in India. The number of people contracting the Corona virus in the previous 24 hours in the country was announced as 52 thousand 123. The total number of cases seen in the country also increased to 1 million 600 thousand*. |

between 8 June and 27 July |

between 17 June ve 28 July between 30 June and 7 August between 8 July and 17 August between 13 July and 28 August |

between 23 July and 4 September between 4 September and 9 November |

between 13 July and 20 August between 27 July and 4 September between 10 August and 24 September between 20 August and 30 September |

|

Case |

3 August: WHO stated that there might not be a “magic wand” such as the development of the “perfect vaccine” for Corona virus, so normalization could be “a long road”. 5 August: WHO reported that the number of young people among those infected with the virus had tripled in the previous five months. 14 August: Loss of life in India exceeded 48 thousand. The country rose to fourth place after the USA, Brazil and Mexico, overtaking England in the number of casualties*. 18 August: WHO warned that the Corona virus outbreak was spread by those aged 20 to 40 who were unaware that they were carrying the virus and that this posed a danger to risk groups. 28 August: 77,266 new cases were recorded in one day in India*. 12 September: The top official in the field of infectious diseases in the USA, Dr. Anthony Fauci, said that after the pandemic, life could only return to normal towards the middle or end of next year*. 16 September: USA ranks first in the number of cases*. 5 November: Denmark announced that the minks that reportedly carry the virus would be killed. 6 November: WHO announced that global vaccination programs were interrupted as medical resources were largely devoted to combating the pandemic. |

||||

|

Bed |

7 September: The number of cases is increasing rapidly in India. The country rose to second place in the world rankings with more than 4 million 208 thousand cases seen to date. According to official data in India, more than 71 thousand people had died due to the pandemic so far*. 16 September: In India, which ranks second after the USA in the number of cases, the number of corona virus detected cases exceeded 5 million*. 17 September: WHO announced that, on average, one out of every 7 Corona cases worldwide was a healthcare worker. According to the same figures, in some countries, one in three cases was a healthcare worker. 25 September: According to the Johns Hopkins Corona Virus Research Center‘s statement, the USA, which ranked first in the list of countries with the most cases, was followed by India with 5.8 million cases and Brazil with 4.6 million cases*. 26 September: WHO warned that until an effective vaccine was found and widely used, deaths due to Corona virus could reach 2 million around the world. 28 September: The Johns Hopkins University Corona Virus Research Center announced that the number of people who had died throughout the world due to the virus pandemic was rapidly approaching 1 million. In the statement, it was noted that the number of Corona virus cases had exceeded 33 million worldwide. 29 September: According to the data and calculations of the Reuters news agency, more than 5,400 people were dying every 24 hours worldwide due to the Corona virus pandemic. This meant 226 deaths per hour, and one person dying every 16 seconds. In other words, 340 people had died worldwide due to the Corona virus during a 90-minute football match. |

between 3 August and 11 September between 7 August and 29 September between 8 September and 9 November between 1 June and 9 July 10 June and 21 July

|

between 12 August and 28 September |

between 4 August and 16 September between 12 August and 23 September |

|

|

Bed |

30 September: It was announced that the number of cases in India could be approximately 10 times higher than the official figures given. According to the research of the Medical Research Council of India, the number of infected people might have exceeded 63 million*. 2 October: Trump and his wife tested positive*. 8 October: The number of cases had exceeded 36 million worldwide. According to the figures compiled by the Corona virus monitoring program of Johns Hopkins University, at least 36 million 166 thousand 500 people worldwide had been diagnosed with Corona virus, more than 1 million of them had died. 12 October: According to a study published in the Virology Journal, the Corona virus can survive for 28 days on paper money, glass and steel surfaces at 20 degrees. The flu virus can survive for 17 days in the same environments and temperatures. 15 October: WHO announced that when the Corona virus vaccine is approved, young and healthy individuals might have to wait until 2022 to be vaccinated. The U.S. Centers for Disease Control and Prevention (CDC) announced that the Corona virus vaccine might not be recommended for children in the first stage. 16 October: WHO determined that four drugs (Remdesivir, hydroxyl-chloroquine, lopinavir / ritonavir and interferon) had “little or no effect” on whether patients died within one month or whether hospitalized patients recovered. 19 October: The number of corona virus cases had exceeded 40 million worldwide. With the approach of the winter months in the northern hemisphere, a serious increase in the number of cases had started to be seen. 21 October: One of the volunteers who participated in the trials of the vaccine developed by the Brazilian National Health Surveillance Agency (Anvisa), the British company AstraZeneca and the University of Oxford, passed away, but the trials will continue. 22 October: The number of countries with more than 1 million confirmed cases worldwide rose to 7. According to data collected by Johns Hopkins University, the United States is followed by India, Brazil, Russia and Argentina. 24 October: On the previous day, the highest number of cases was recorded since the first days of the pandemic in America*.

|

between 25 June and 4 August between 2 July and 18 August between 14 July and 11 September between 14 August and 24 September between 11 September and 2 November |

|

||

Note: * country-specific positive news

Table A.2. Negative shock dates

|

Variables |

Events |

Negative Shock Dates |

|||

|

USA |

India |

China |

Germany |

||

|

Variables |

Events |

Negative Shock Dates |

|||

|

USA |

India |

China |

Germany |

||

|

Death |

16 June: Based on the results of a study conducted at Oxford University, it was announced that the drug Dexamethasone reduced the mortality rate among the most severe Corona patients by about a third, which could be a turning point in the treatment of the Corona virus. 18 June: WHO reported that it hopes millions of doses of the vaccine can be produced by the end of 2020 and 2 billion doses by the end of 2021. 23 June: The French pharmaceutical company Sanofi stated that it hoped to get approval for the vaccine developed with British Glaxo Smith Kline (GSK) in the first half of 2021, earlier than the anticipated date. 2 July: Tesla announced that they had developed a mobile molecule printer to be used in the production of the Corona virus vaccine that German biotech firm CureVac is working on. 15 July: Moderna announced in the early stages of its vaccine research that the vaccine was safe and that 45 healthy volunteers had been immunized. 20 July: The vaccine developed by AstraZeneca-Oxford University was announced to be safe and effective in immunization in the first clinical trials. 22 July: The head of the WHO Emergency Program said that „good progress“ had been made in vaccine development, and that the vaccine could be used in early 2021. 27 July: Moderna announced that the third phase tests to be carried out on 30 thousand people had been initiated and that the first trial vaccine had been given to a volunteer. 6 August: Trump said that it was possible for the vaccine to hit the market ahead of the US elections on November 3*. 11 August: Russian President Putin announced that Russia was the first country to register a vaccine against the virus and that his daughter had been vaccinated. 13 August: Argentina and Mexico announced that they would produce AstraZeneca‘s vaccine for all Latin American countries. Parana State of Brazil also reported that they would test and produce Russia‘s new vaccine. 24 August: Trump announced that the US Food and Drug Administration (FDA) would allow the use of plasma therapy for recovering patients in emergency situations*. 31 August: The European Commission announced that it would contribute 400 million Euros to the vaccination program led by WHO. 13 September: The New England Journal of Medicine stated that wearing a mask contributes to the formation of immunity against the virus and this can further reduce the spread of the virus. 29 June: The U.S. Department of Health and Social Services announced that an agreement with Gilead Sciences had been reached to purchase a significant amount of drugs for Covid treatment*. |

between 26 June and 12 August between 8 September and 26 October between 8 September and 26 October |

between 16 June and 24 July between 22 June and 30 July between 30 July and 15 September |

between 26 June and 7 August between 17 July and 26 August between 23 July and 6 October |

|

|

Case |

23 September: Johnson & Johnson announced that the final stage had been reached in single-dose vaccine trials. 4 October: White House doctor said Trump‘s condition was improving*. 5 October: Trump was discharged from the Medical Center where he had been treated for the Corona virus*. 10 October: Trump physically appeared in public for the first time 9 days after being diagnosed with Corona*. |

between 26 June and 17 August between 29 July and 16 September between 18 August and 29 September between 9 September and 19 October |

between 16 June and 31 July between 1 July and 16 October |

between 22 June and 30 July between 25 June and 7 August between 21 August and 10 October |

between 5 August and 10 October |

|

Bed |

20 October: Johns Hopkins University revealed that antibodies used to develop convalescent plasma therapy were stronger in patients who had suffered the most severe COVID-19 and recovered. 23 October: In the USA, FDA approved the use of the antiviral drug Remdesivir, which became the first drug to be licensed*. 29 October: Moderna announced that preparations had started to put the vaccine on the market. |

between 26 June and 12 August between 9 September and 6 November |

between 16 July 25 August between 10 August and 12 October between 27 August and 15 October between 3 September and 21 October |

between 19 June and 31 July between 30 July and 21 September |

between 26 June ve 10 August |