Ekonomika ISSN 1392-1258 eISSN 2424-6166

2026, vol. 105(2), pp. 6–23 DOI: https://doi.org/10.15388/Ekon.2026.105.2.1

Rytė Panciriovaitė

Artea Bank, Vilnius, Lithuania

E-mail: ryte.panciriovaite@evaf.stud.vu.lt

ORCiD: https://orcid.org/0009-0008-6047-6218)

Dr. Linas Jurkšas*

Assistant Professor at the Department of Finance, Vilnius University, Vilnius, Lithuania

https://ror.org/03nadee84

E-mail: linas.jurksas@evaf.vu.lt

ORCiD: https://orcid.org/0000-0002-9017-5968

Abstract. How do geopolitical factors ripple through the European sovereign bond yields? And does this effect differ between Eastern and Western European markets? These two crucial, but not yet fully answered questions motivated us to investigate the link between geopolitical factors and sovereign bond yields in Eastern and Western Europe. We thus leverage a panel dataset covering 16 European countries from 2015 to 2025, both at daily and monthly frequencies. The first set of panel regression models revealed that rising geopolitical tensions exert a robust, direct and statistically significant effect on sovereign yields even with a lag. The second set of panel models undercover that this effect is much stronger in Eastern Europe than in the Western European region. This gap persists across frequencies and model specifications, thus highlighting the heightened vulnerability of less liquid, lower-rated Eastern markets. These and other findings in the study could help investors adjust their portfolios more effectively in response to geopolitical shocks, and assist supervisors in safeguarding financial stability.

Keywords: geopolitics, geopolitical shock, sovereign yield, sovereign bond, Eastern and Western Europe.

_________

* Correspondent author.

Received: 15/07/2025. Accepted: 16/03/2026

Copyright © 2026 Rytė Panciriovaitė, Linas Jurkšas. Published by Vilnius University Press

This is an Open Access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

The academic literature contains a large number of studies on bond yields and their determinants. Bond yields are most often related to macroeconomic indicators such as interest rates, the level of public debt, or inflation. These relationships have been explored in papers by Poghosyan (2014), Jurkšas and Kropienė (2014), Husein and Endri (2024), Varirahartia and Santoso (2022), Fatmawatie et al. (2024), Sehgal and Singh (2024), Yakubovskiy et al. (2021), Hsing (2015), Perovic (2015), alongside many others. Additionally, there is a substantial amount of academic literature examining the impact of various external factors on financial markets, including investor behaviour or central bank policies (Husein & Endri, 2024; Varirahartia & Santoso, 2022; Heryán & Ziegelbauer, 2016). However, geopolitical risk is becoming an increasingly relevant factor due to the rising frequency of military conflicts and other geopolitical shocks. Gopinath (2024) identifies the COVID-19 pandemic and the Russian invasion of Ukraine as the most significant shocks of recent years. These events have forced countries to reassess their trading partners and redirect Foreign Direct Investment (FDI) flows. Nevertheless, the impact of a war or another geopolitical shock can vary significantly from region to region. For instance, Swistek and Paul (2023) claim that, in this context, the Baltic Sea has become the epicentre of geopolitical interests and conflicts. They also acknowledge the growing threat of the entire Arctic and North Atlantic region becoming a potential zone of conflict. The recent crisis in the Middle East and an increased hostility between the US and People’s Republic of China over Taiwan have also raised concerns about geopolitical stability (Dieckelmann et al., 2024).

Due to the increasing focus on geopolitical risk, researchers are including this factor more frequently when evaluating its impact on various asset classes, the financial system and markets (Bondarenko et al., 2023; Jawadi et al., 2024; Ahmed et al., 2024; Bossman & Gubareva, 2023; Dieckelmann et al., 2024). However, despite the growing focus on geopolitical risk, its impact on bond markets and cross-country differences remains insufficiently explored in academic literature. While previous studies covering Europe provide valuable insights, they do not explicitly differentiate between regional groups. For instance, Afonso et al. (2024) analyse the impact of geopolitical risk on the risk of sovereign debt in 26 European countries. Meanwhile, Bratis et al. (2024) examine the performance of EMU members during both crisis and non-crisis periods, whereas Dieckelmann et al. (2024) highlight the safe-haven effects in Germany. While these contributions deepen our understanding of how geopolitics influences European bond markets, they tend to treat countries either in aggregate or in isolation, rather than by comparing different regions. What is still missing is a comparison between Western and Eastern Europe. This has become even more important in recent years due to the significant increase in geopolitical pressure in Europe amid emerging conflicts. Furthermore, given that Eastern and Western countries are characterised by different economic and political circumstances, it is likely that the impact of geopolitical risks on bond markets may also differ.

This paper aims to identify the impact of geopolitical factors on sovereign bond yields in Eastern and Western Europe. By addressing this gap, the study provides new theoretical and practical insights into how geopolitical tensions are transmitted across regions. A better understanding of the impact of geopolitical factors on sovereign bonds could help investors build investment portfolios that protect and grow their capital. Meanwhile, market supervisors and regulators could gain insight into how geopolitical risk affects the stability of financial systems in different European regions.

The constructed panel regression models reveal that the impact of geopolitical factors on European bond yields was significant and direct between 2015 and 2025. Notably, the effect is stronger in Eastern Europe than in the Western European region, which indicates that Eastern European markets are more sensitive to changes in the global geopolitical situation. The strongest effects were found in Hungary, while somewhat weaker but still statistically significant effects were also observed in the sovereign bond markets of Poland, Latvia and Lithuania. While the impact of geopolitical risk was not statistically significant for other markets, the estimate was positive for all countries.

This paper is divided into the following sections. The second section discusses the relationship between geopolitical risk and sovereign bond yields in the relevant academic literature. The third section presents the data and methodology of the study. The fourth section discusses the results of the constructed models, and the fifth section provides further discussion of these results. Whereas, the final section concludes this research.

Researchers analysing sovereign bond yields typically discover that they are influenced by various macroeconomic factors. The most common approach is to investigate how exchange rates, foreign exchange reserves, inflation, interest rates and public debt levels impact sovereign bond yields (Table 1). For instance, Afonso et al. (2015) identified three primary risk factors influencing sovereign bond yield developments: credit, liquidity, and international risks. Pinho and Barradas (2021) provide similar insights, identifying liquidity risk, deficits and inflation rates as the main factors leading to changes in government bond yields. Poghosyan (2014) also confirmed the positive correlation between the debt-to-GDP ratio and government bond yields in the long run. Hsing (2015) showed that higher government debt-to-GDP ratios lead to higher Spanish government bond yields and a positive correlation with short-term Treasury bill rates, US 10-year government bond yields, and expected inflation rates. Similarly, Perović (2015) found that government debt and primary deficits positively impact long-term government bond yields in Europe. However, results can often differ, even though the direction of most factors’ effects is clear and intuitive. Such diverging results may be due to the different research methods employed or the specific characteristics or economic conditions of the analysed markets.

Geopolitics and the associated risks are becoming an increasingly relevant research topic. The ever-changing and intensifying geopolitical shocks, not only in Europe but worldwide, have encouraged researchers to examine the impact of geopolitical risks on economic and social processes, as well as on different markets. Caldara and Iacoviello (2022) define geopolitical risk as the risk associated with wars, terrorism and international tensions that affect the evolution of relations between countries. The authors developed a geopolitical risk index by monitoring the number of press articles on geopolitics; an increase in the index’s value indicates a rising likelihood or intensity of adverse geopolitical events.

Major geopolitical events, such as the outbreak of the pandemic and the Russian invasion of Ukraine, have had a profound impact on investor behaviour and asset allocation. As geopolitical risk increased, confidence declined, and market sentiment became more pessimistic, encouraging a shift towards safer assets or regions and increasing volatility. During the pandemic, government bonds strengthened their role as a safe-haven asset because investors quickly replaced equities with safer securities. Baur and Smales (2020) demonstrated that, while equities and bonds are generally negatively affected by geopolitical risk, gold and silver can serve as hedges against it. Similarly, Sójka, Demir, and Zaremba (2022) found that, during the Russia–Ukraine conflict, the most resilient asset classes were gold, silver, green bonds, the Swiss Franc, and real estate. Nittayakamolphun, Bejrananda, and Pholkerd (2024) also identified gold, US government bonds, and the US dollar as safe assets during periods of heightened geopolitical tension.

|

Study |

Variable |

Relationship with sovereign yields |

|

Afonso et al. (2015), Yakubovskiy et al. (2021), Husein and Endri (2024), Fatmawatie et al. (2024) |

Exchange rate |

Positive |

|

Hsing (2015) |

Negative |

|

|

Varirahartia and Santoso (2022) |

None |

|

|

Hussain and Endri (2024), Varirahartia and Santoso (2022), Sehgal and Singh (2024) |

Foreign exchange reserves |

Negative |

|

Pinho and Barradas (2021), Hsing (2015) |

Inflation |

Positive |

|

Poghosyan (2014), Varirahartia and Santoso (2022) |

Negative |

|

|

Husein and Endri (2024), Fatmawatie et al. (2024) |

None |

|

|

Poghosyan (2014), Husein and Endri (2024), Varirahartia and Santoso (2022), Fatmawatie et al. (2024), Sehgal and Singh (2024) |

Interest rate |

Positive |

|

Yakubovskiy et al. (2021), Hsing (2015), Poghosyan (2014), Perović (2015) |

Level of public debt |

Positive |

|

Pinho and Barrad (2021), Yakubovskiy et al. (2021) |

Negative |

|

|

Hsing (2015), Sehgal and Singh (2024) |

GDP growth rate |

Negative |

|

Varirahartia and Santoso (2022) |

Redemption date |

Positive |

|

Hsing (2015) |

Yields on other sovereign bonds |

Positive |

|

Heryán and Ziegelbauer (2016) |

Negative |

Source: compiled by author based on the results of the studies listed in the table.

However, the impact of geopolitics on bond yields is often ambiguous (Table 2). Subramaniam (2022) found that bond yields in BRICS countries were affected differently by changes in geopolitical risk. Tang et al. (2023) state that, in the long run, bond yields are negatively affected by economic policy uncertainty and geopolitical shocks, as investors tend to shift their investments towards safer options such as bonds. Similar conclusions were also reached by Jalkh and Bouri (2022). Bratis et al. (2024) confirmed that government bond yields and geopolitical risk are more negatively correlated during times of crisis. According to the authors, however, this relationship is not as strong after crises in most of the countries studied, which means that an increase in geopolitical risk does not pose a significant threat to financial markets. Importantly, many other authors obtained opposite results. For example, Lee et al. (2022) found that geopolitical threats directly and significantly affect bond returns in China. De Wet (2023) also found that Australian government bond yields tend to rise when geopolitical risks increase, which suggests that investors should exercise caution with these securities. Authors focusing on the European region also provide mixed results. For example, Afonso et al. (2024) analysed the impact of geopolitical risk and uncertainty on the debt risk of 26 European countries, finding that geopolitical tensions lead to rising government bond yields. They also determined that tensions in the Middle East negatively impact European sovereign bond returns. In contrast, Dieckelmann et al. (2024) found that, among euro area countries, Germany was the only case where yields fell under heightened geopolitical uncertainty, reflecting the safe-haven status of Bunds.

|

Study |

Region/country |

Impact of increased geopolitical risk on yields |

|

|

Dieckelmann et al. (2024) |

Developed markets |

Germany |

Declining yields |

|

Tang et al. (2023), Jalkh and Bouri (2022) |

USA |

Declining yields |

|

|

De Wet (2023) |

Australia |

Increasing yields |

|

|

Afonso et al. (2024), Bratis et al. (2024) |

Group of European countries |

Declining yields |

|

|

Beirne et al. (2021) |

Developed countries group |

Declining yields |

|

|

Lee et al. (2022) |

Emerging markets |

China |

Increasing yields |

|

Subramaniam (2022) |

Declining yields |

||

|

Subramaniam (2022) |

India |

Increasing yields |

|

|

Subramaniam (2022) |

Brazil |

Declining yields |

|

|

Beirne et al. (2021) |

Group of developing countries |

Declining yields |

|

Source: compiled by the authors and based on the results of the studies listed in the table.

In summary, relevant studies have shown that the results of geopolitical risk impact analyses depend on the research method chosen and the context. When examining the significance and impact of these risks, it is important to consider the broader context during the relevant period. Differences in the impact of geopolitical risk on bond yields may be due to variations in economic development or region. For this reason, further research is needed to shed more light on the dynamics of bonds in different countries and the factors affecting them. With regard to these studies, it would be valuable to investigate the dynamics of yields in different European countries and the factors influencing them, particularly with the objective to establish whether these differences are more pronounced between Eastern and Western European countries.

To determine the impact of geopolitical risk on sovereign bonds in Eastern and Western Europe, and to compare results between regions, we carried out a panel regression analysis for the period between 2015 and the beginning of 2025. The dependent variable is an index based on 10-year sovereign bond yields. Bonds of this duration are typically considered the benchmark and are often used to analyse yield dynamics. All data were obtained from Bloomberg.

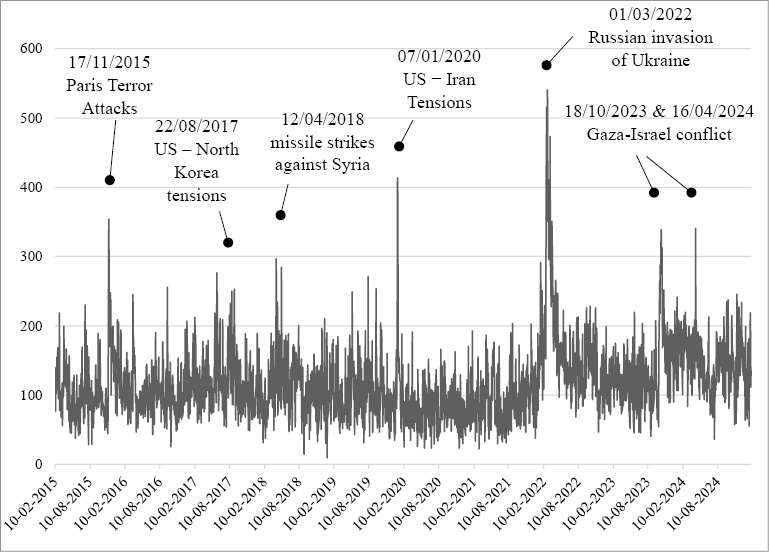

The most important explanatory variable for changes in sovereign yields is the Geopolitical Risk Index, as introduced by Caldara and Iacoviello (2022). This index tracks media activity by counting the number of articles published on geopolitical tensions, war, and conflict risks. Figure 1 illustrates the evolution of the index from 10 February 2015 to 31 January 2025. While there is no clear prevailing trend in the values of the index, some short-term spikes reflecting significant geopolitical events are visible. The more pronounced spikes until 2022 are recorded on 17 November 2015, following the terrorist attacks in Paris, and on 22 August 2017, amid the North Korean crisis. Significant spikes in the index also occurred on 12 April 2018 due to missile strikes against Syria, and on 7 January 2020 due to the escalation of tensions between the US and Iran. The largest increase in the index occurred in March 2022, i.e., at the start of Russia’s invasion of Ukraine. The index peaked at over 500 points, reaching its highest value during the entire sample period between 2015 and 2025. Two further pronounced peaks observable between 2023 and 2024 are related to the escalation of the Gaza–Israel conflict.

We investigate the impact of geopolitical risks on 16 European countries, separating them into Eastern and Western groups. The Eastern group is formed based not only on membership of the European Union and the United Nations’ regional classification, but also on the geopolitical environment. Consequently, countries bordering Russia, Belarus or Ukraine are included in the Eastern group due to the somewhat larger threat of conflict and political tensions within these countries. This group includes Finland, Latvia, Lithuania, Poland, Slovakia, the Czech Republic, Hungary, Romania, and Bulgaria. Most of these countries were also analysed in a study by Perović (2015)1. The Western group was formed on the basis of European Union and United Nations membership and geographical distance from conflict areas. The size of the economy and market depth of each country were also assessed to create a group of strong, relatively stable markets. Previous research also shows that financial markets in Eastern Europe are often characterised by unstable liquidity conditions and extreme liquidity events, whereas larger markets in Western Europe are typically deeper and more liquid (Galloppo, Paimanova, & Aliano, 2015). Accordingly, the Western group consists of Austria, Belgium, France, Germany, the Netherlands, Portugal, and Spain. These selection criteria ensure that the chosen countries represent distinct geographical and structural markets, enabling a meaningful East–West comparison.

Source: constructed by the authors with Bloomberg-sourced data and based on Caldara and Iacoviello (2022).

In line with the findings presented in the literature review, it is important to control for other factors that could explain bond yield dynamics. Inflation is one of the main control variables used by several other authors: Bondarenko et al. (2023), Jawadi et al. (2024), Baur and Smales (2020), and Afonso et al. (2024), to give a few examples. The widely used 5-year/5-year daily inflation swap rate was included. For the robustness check using monthly data, the Harmonised Index of Consumer Prices (HICP) is used for each country2. The Krippner (2020) shadow interest rate is used as the monetary policy proxy, as it encompasses not only the short-term interest rate, but also asset purchases and other non-standard measures by construction. This indicator is particularly relevant given that interest rates reached the effective lower bound in the euro area between 2014 and 2022. Afonso et al. (2024), among others, also included interest rates in regression models in their analysis of the impact of geopolitical risk on bond markets. We also use stock indices for each country because stock markets are often found to be correlated with investors’ behaviour in bond markets. Furthermore, stock indices depict prevailing financial market sentiment. Various stock market indices were used in the studies of Jawadi et al. (2024), Baur and Smales (2020), Tang et al. (2023), and Wang et al. (2019).

We conducted our study using panel regression analysis. This method allows us to combine, compare and analyse information from different countries and time periods more efficiently than estimating separate time-series or cross-sectional models. This research method has also been chosen in other relevant studies, such as those by Dieckelmann et al. (2024), Jalkh and Bouri (2022), and Afonso et al. (2024). We constructed two different panel models: a general model that does not distinguish between Eastern and Western regions, and a model with an interaction variable that allows us to statistically assess whether the effects differ between these two regions.

First, a general model is created which includes all countries:

Yield_Chgi,t = α + β1 * GPRt + β2 * SIRt + β3 * Infl_Swapt + β4 * Log_Stocki,t + ui + εi,t (1)

Where:

Yield_Chgi,t – bond yields in country i on time period t;

GPRt – geopolitical risk index in period t;

SIRt – Krippner shadow interest rate change in period t;

Infl_Swapt – the change of the 5-year/5-year inflation swap rate in period t;

Log_Stocki,t – the logarithmic return of stock market indices in period t for country i;

ui – random effects at country level.

Our main hypothesis is that geopolitical risk has a statistically significant impact on sovereign bond yields. If β1 is statistically significant, this hypothesis is rejected and it is confirmed that geopolitical risk has a significant impact on yields.

We also constructed a second model which focused on regional differences:

Yield_Chgi,t = β0 + β1 GPRt + β2Regioni + β3 (GPRt * Regioni) + Xi,t γ + εi,t (2)

Where:

Regioni– binary variable (‘1’ – for Eastern Europe, ‘0’ – for Western Europe);

GPRt * Regioni – an interaction term that shows whether the impact of geopolitical risk differs between regions;

Xi,– a vector set of control variables.

Our additional hypothesis states that the impact of geopolitical risk on bond yields is significantly stronger in Eastern than in Western Europe. If β3 is found to be positive and statistically significant in a model that isolates regional differences, then, this hypothesis is rejected, confirming that the impact of geopolitical risk is stronger in Eastern Europe. If β3 is statistically insignificant, then this hypothesis is rejected.

To further assess the impact of geopolitical risk on different bond markets, the study builds separate regression models for each country. These models follow the same principle as the main model; the structure of the variables and their lags remain unchanged. The country-by-country analysis enables us to determine whether the impact of geopolitical risk and the sensitivity of bond markets vary between countries. To check the robustness of the results, the research was also conducted with different lags and data frequencies, i.e., daily versus monthly.

This section of the paper presents the results of an empirical study investigating the impact of geopolitical risk on the sovereign bond yields of Eastern and Western European countries. First, we discuss the characteristics of the selected variables and how they were prepared for further analysis. Next, the results of a panel regression analysis are presented, showing the overall impact of geopolitical risk for the group of countries as a whole, and the difference between the Eastern and Western European regions. Finally, conclusions are drawn, assessing the impact of geopolitical factors on individual countries.

To perform panel regression correctly, it is necessary to assess the statistical properties of the selected variables and carry out any required data transformations. First, a stationarity test was carried out for each selected variable, with transformations implemented based on the obtained results. Stationarity was assessed by using the Im-Pesaran-Shin (IPS) panel unit root test, which enables panel data to be examined in different groups. The stationarity test results for daily data showed that indicators of 10-year sovereign bond yields, shadow interest rates, inflation expectations, and stock market indices were non-stationary. The transformations performed (daily changes and logarithmic differences) allowed us to generate stationary data suitable for further analysis. The geopolitical risk index did not require further adjustments, as the test confirmed its stationarity.

The descriptive statistics of the daily stationary variables show that the yield changes of sovereigns in Eastern Europe have a higher mean and standard deviation (Table 3). A comparison of the maximum and minimum values across regions reveals significantly larger differences in the East. This suggests that bond markets in Eastern European countries are not only more volatile, but also more sensitive to short-term shocks. Similar results are observed with stock market index returns. The geopolitical risk index shows high volatility due to the excessive divergence between the minimum and maximum values. This suggests that the index is highly sensitive to short-term shocks reflecting various geopolitical events or rising tensions. However, the movements in shadow interest and inflation swap rates do not exhibit particularly high volatility or excessively divergent extreme values.

|

Variable |

Region |

Average |

Median |

Standard deviation |

Minimum value |

Maximum value |

|

Changes in 10-year sovereign bond yields |

Eastern Europe |

0.000760 |

-0.000200 |

0.0567 |

-1.06 |

2.09 |

|

Western Europe |

0.000589 |

-0.000300 |

0.0484 |

-0.359 |

0.410 |

|

|

Logarithmic returns of stock market indices |

Eastern Europe |

0.000258 |

0.000140 |

0.0108 |

-0.226 |

0.121 |

|

Western Europe |

0.000149 |

0.000479 |

0.0120 |

-0.161 |

0.104 |

|

|

Geopolitical risk index |

118.009 |

108.841 |

53.606 |

9.492 |

540.827 |

|

|

Krippner shadow interest rate change |

0.00164 |

-0.0000237 |

0.0197 |

-0.171 |

0.123 |

|

|

5-year/5-year inflation swap rate change |

0.000190 |

0 |

0.0236 |

-0.185 |

0.267 |

|

Next, the optimal lag period was determined for each independent variable by using the Akaike Information Criterion (AIC). For the geopolitical risk index, the AIC most often suggested a lag of seven days, which is a result confirmed in 13 out of 16 countries. For the stock market index, different lags were suggested; however, a 1-day lag was chosen as stock markets are expected to react quickly to ongoing developments. For shadow interest rates and inflation expectations, the AIC generally recommended lag periods of 9 and 3 days, respectively.

Additional model checks and adjustments were also carried out. The results of the Breusch-Pagan test revealed heteroskedasticity, with a p-value lower than 0.05. The Breusch-Godfrey/Wooldridge test detected autocorrelation in the errors, with a p-value of less than 0.05. Given these results, Arellano standard errors were used, which are robust to both heteroskedasticity and autocorrelation and are widely applied in empirical panel data research. Unlike conventional White robust errors, which only address heteroskedasticity, the Arellano estimator extends the covariance correction to the panel data setting. This is achieved by treating each country as a cluster, thereby allowing for arbitrary serial correlation of errors within clusters (Millo, 2017). In addition, the model was checked for multicollinearity. As the estimated VIF values did not exceed 10, there is no indication of multicollinearity, and no further corrections were needed.

This section of the study presents the results of various panel regression models investigating the impact of geopolitical factors on sovereign bond yields. The two constructed panel regression models produced almost identical results: all explanatory variables were statistically significant at the 5% level (Table 4). The geopolitical risk index was found to have a statistically significant and positive effect on sovereign bond yields for the panel of the 16 countries studied. These results allow us to reject the null hypothesis and confirm that geopolitical risk has a statistically significant impact on sovereign bond yields. The control variables also demonstrate a statistically significant relationship with bond yields, and importantly, with the expected signs. Stock market changes are found to have an inverse relationship, while the shadow interest rate and inflation expectations have a direct link with sovereign bond returns. The results for the control variables are consistent with those of other relevant studies (Pinho & Barradas, 2021; Hsing, 2015; Poghosyan, 2014; Hussain & Endri, 2024; Varirahartia & Santoso, 2022; Fatmawatie et al., 2024; Sehgal & Singh, 2024).

|

Variable |

Fixed effects model |

Random effects model |

||

|

Coefficient |

p-value |

Coefficient |

p-value |

|

|

Constant |

- |

- |

-2.1671e-03 |

0.0006022 *** |

|

Geopolitical risk index |

2.3923e-05 |

9.300e-07 *** |

2.3924e-05 |

9.226e-07 *** |

|

Stock market index returns |

-6.2502e-02 |

0.006820 ** |

-6.2370e-02 |

0.0069214 ** |

|

Change in the shadow interest rate |

3.7005e-02 |

0.005299 ** |

3.7005e-02 |

0.0052895 ** |

|

Change in inflation expectations |

6.7707e-02 |

9.656e-10 *** |

6.7708e-02 |

9.509e-10 *** |

|

Hausman test p-value: 0.9994 |

||||

Once the fixed and random effects regression models have been constructed, a Hausman test is performed to determine the most appropriate model. The null hypothesis of the test states that the random effects estimator is both consistent and efficient, whereas the fixed effects estimator is only consistent. The test result revealed a p-value of 0.9994, which is significantly higher than the conventional threshold of 5%. This means that we cannot reject the null hypothesis that there is no systematic difference between the two estimators. This suggests that the random effects model is consistent and efficient in this instance. It is important to note, however, that the estimates for the two methods are very similar. The coefficient for the Geopolitical Risk Index implies that a one-point increase in the index raises 10-year sovereign yields by approximately 0.0024 basis points. This effect can be interpreted in the context of significant geopolitical risk spikes in the past. For instance, during the Russian invasion of Ukraine in March 2022, the index surged by over 400 points (Figure 1), which translates to an estimated yield increase of around 90–100 basis points.

Once the impact of geopolitical factors on the overall group of countries has been assessed, it is important to identify any regional differences. To distinguish between the results for Eastern and Western European countries, the baseline panel regression model includes an interaction variable between the geopolitical risk index and region (East versus West). The results of this model reveal that the impact of geopolitical risk on sovereign bond yields differs significantly between these two groups, as the interaction variable (GPR x Region) has been found to be statistically significant (Table 5). This interaction variable shows that a 1-point increase in the geopolitical risk index has an effect that is almost 5 times stronger for the Eastern group of countries than for the Western group after 7 days. It is important to note that bond markets do not react immediately to geopolitical factors, but a delay is involved. This finding is crucial for investors, who may also make decisions with some delay following a surge in geopolitical tensions.

|

Variable |

Fixed effects model |

Random effects model |

||

|

Coefficient |

p-value |

Coefficient |

p-value |

|

|

Constant |

- |

- |

-3.7879e-04 |

0.01007 * |

|

GPR x Region |

2.8365e-05 |

0.006988 ** |

2.8365e-05 |

0.00699 ** |

|

Region |

- |

- |

-3.1790e-03 |

0.01058 * |

|

Geopolitical risk index |

7.9675e-06 |

< 2.2e-16 *** |

7.9677e-06 |

< 2.2e-16 *** |

|

Stock market index returns |

-6.2778e-02 |

0.013714 * |

-6.2684e-02 |

0.01382 * |

|

Change in the shadow interest rate |

3.7006e-02 |

0.044989 * |

3.7005e-02 |

0.04500 * |

|

Change in inflation expectations |

6.7707e-02 |

3.634e-06 *** |

6.7707e-02 |

3.635e-06 *** |

|

Hausman test p-value: 1 |

||||

These results allow us to conclude that the impact of geopolitical risk is much stronger in Eastern Europe than in Western Europe. This is potentially due to the fact that the latter region is characterised by greater economic resilience and stability, higher market liquidity, and lower vulnerability in general than Eastern European countries. Consequently, Western Europe’s sovereign bond markets are more stable and better equipped to absorb geopolitical risk shocks. Conversely, the greater exposure to geopolitical risk in Eastern Europe may suggest that bond market participants are more sensitive to emerging geopolitical threats, demanding a higher risk premium and leading to higher sovereign bond yields.

For the robustness check, the lag of the geopolitical risk index was reduced to one day3. The results still show that the impact of geopolitical risk on changes in sovereign bond yields is statistically significant. The estimated impact of geopolitical risk is of a similar strength and maintains the same positive direction. However, there is a significant difference between the models being compared: the one-day lag no longer captures the difference in the impact of geopolitical risk across regions. In this case, the interaction variable is not statistically significant (p-value = 0.69937). This suggests that bond markets react similarly in the short term, but that the difference between Eastern and Western European markets becomes more evident over a longer time horizon.

To assess how the results may change depending on the frequency of the data and to highlight longer-term trends, the influence of geopolitical factors is analysed by using monthly data. Similar results are shown by the fixed and random effect models: the geopolitical risk index is statistically significant in both models and has a positive effect on changes in sovereign bond yields4. It could be argued that the bond market might react with a delay of one month, as well as during the first several days. The interaction variable is also found to have a statistically significant positive effect on the Eastern European group. This further supports the hypothesis that Eastern and Western European markets react differently to geopolitical signals, with the effect being observed even with a one-month lag.

To gain further insight into the impact of geopolitical factors on yields in specific markets, a regression analysis was conducted on a country-by-country basis. The same model variables and lag periods were used as in the main panel model with daily data. This methodological consistency enables more robust comparisons to be made between the results obtained by different models.

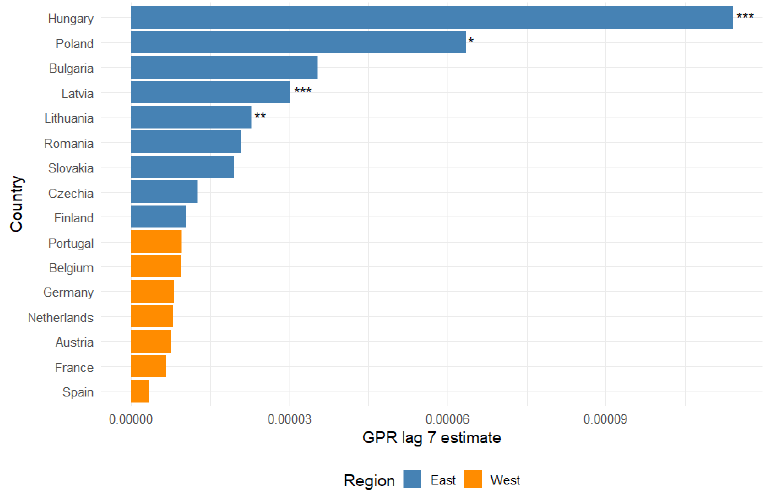

The results of the sixteen regression models show that geopolitical risk has a statistically significant lagged impact on several countries, although the strength of this impact varies considerably (Figure 2). The strongest effects are found in Hungary, although statistically significant effects are also evident in the sovereign bond markets of Poland, Latvia, and Lithuania. These countries, which are denoted by significant geopolitical exposure, belong to the Eastern European group. In contrast, Western European countries exhibit very low coefficients with low significance (p-values), which indicates greater resilience to geopolitical pressures and more stable bond markets. These results confirm the importance of geopolitical factors in influencing bond markets in countries that are more directly exposed to a higher risk of potential conflicts and threats.

The impact of geopolitical risk was found to be positive for both Eastern and Western regions: when geopolitical risk increased, bond yields also increased. No countries were found to have falling sovereign bond yields as geopolitical risk increased over the entire sample period (2015–2025). This suggests that investors across Europe view geopolitical risk as a negative signal requiring a higher risk premium, an effect which may manifest itself with a delay. It may also result from a more rapid sell-off of bonds when risks surge. Similarly, although yields on Western European sovereign bonds do not tend to fall when geopolitical risk rises, the effect on this group was found to be statistically insignificant. This confirms again that Western Europe is less sensitive to geopolitical events worldwide.

Taken together, the results of both panel models show that the impact of geopolitical risk is statistically significant and positive for all constructed models. While previous studies (Bondarenko et al., 2023; Jawadi et al., 2024; Ahmed et al., 2024; Bossman & Gubareva, 2023; Dieckelmann et al., 2024) have confirmed the impact of geopolitical risk on financial markets, this study also reveals regional variations in responses to geopolitical shocks around the world. Furthermore, this research takes into account the varying frequencies and lags of the data. According to the study, the Eastern European region is more sensitive to increased geopolitical tensions than Western markets. While bond markets react similarly in the short term, differences between regions become more pronounced over a longer period. The similarity in the initial reactions of both regions could be attributed to a common ‘flight-to-safety’ response, where investors rush to move their assets away from risk in the aftermath of a geopolitical event. This leads to broadly comparable short-term movements across European bond markets. However, as initial uncertainty eases down, investors begin to reassess the relative riskiness of different regions. At this stage, structural factors such as the market size, liquidity, and institutional stability may become more important. Consequently, yields in Eastern Europe may increase more strongly with a delay, while Western markets may stabilise more quickly. The differential impact of geopolitical risk on markets was also described by Ahmed et al. (2024). According to these authors, German and French financial markets are more resilient to local and global geopolitical shocks. A study by Bossman and Gubareva (2023) also highlighted differences between markets, identifying how the magnitude of the reaction depends on market development. Interestingly, monthly cross-sectional data revealed significant differences between Eastern and Western European countries, with Eastern Europe recording a more pronounced impact of geopolitical tensions on yields. These findings are important for investor behaviour, as investors look for safer markets or financial instruments in times of major shocks, moving away from less safe markets in the process.

Regression models for individual markets showed that the geopolitical risk factor has a positive impact on all countries, although this effect is insignificant for Western European countries. Over the whole sample period of 2015–2025, we did not find any market whose sovereign bond yields would fall as geopolitical risk increased. However, this effect was statistically significant only for four countries on the Eastern flank. These results are consistent with those of other similar studies. For example, Bratis et al. (2024) determined the significance of geopolitical risk for the bonds of European Economic and Monetary Union countries in their study, but this effect was not strong for most of the countries studied and did not pose a significant threat to financial markets. Based on the results of Bratis et al. (2024) and the present study, it can be argued that the magnitude of the effect varies according to the region, lag period, and data frequency, and that these factors must be considered when interpreting results.

The low impact of geopolitical risk may be due to the fact that the geopolitical risk index is a common global measure of risk, which means that its values and short-term fluctuations may not always accurately reflect the geopolitical situation in each country. Additionally, smaller effects may be observed because bond yields may be more strongly influenced by factors not included in this study. Geopolitical factors are unlikely to be the main determinant of bond market movements over the long term, but they are likely to become more pronounced during periods of heightened geopolitical risk. Lastly, the findings are based on the 2015–2025 period which could lead to different trends due to specific market conditions and geopolitical tensions. Future research could address these limitations by using country-specific geopolitical risk indicators, including a broader set of macroeconomic variables or exploring alternative econometric methods. Also, expanding the analysis beyond Europe could provide valuable insights into how the transmission of geopolitical shocks differs across global sovereign bond markets.

Based on the analysis carried out, investors and other market participants should consider the geopolitical context, especially when investing in Eastern European bond markets. This region tends to be more reactive to geopolitical developments; therefore, diversification of portfolios and reacting quickly to shocks can help limit losses. However, significant regional differences in the lagged geopolitical risk index mean that investors need to adjust their portfolios even after a change in the geopolitical situation.

This study examines the significant relationship between geopolitical shocks and European sovereign yields, and whether this effect differs between Eastern and Western countries. We use panel regressions on a dataset covering 16 European countries, with daily and monthly data from 2015 to 2025. Two distinct types of panel regression are conducted: the first type focuses on the impact of the geopolitical factor on the panel of 10-year European sovereign bond yields, while the second type concentrates on the differences between Eastern and Western countries. This study is highly relevant, given both the growing frequency of geopolitical shocks and the lack of research focusing on regional differences across European countries.

The results of the first set of panel models show that an increase in geopolitical risk has had a positive and statistically significant impact on European sovereign bond yields during the period covered by the sample. This effect was confirmed by both the random and fixed effects models, for daily and monthly data. These results suggest that investors perceive geopolitical shocks as an important risk factor leading to a higher risk premium.

The results of the second set of panel regression models show that there are significant differences in the impact of geopolitical risk on various bond markets. The effect was found to be five times stronger in Eastern Europe than in Western Europe. These results suggest that Eastern European markets are more sensitive to changes in the global geopolitical situation. This may be related to the lower liquidity and stability of bond markets in Eastern European countries and the higher risk of a direct link to conflicts in this region.

We did not find any country whose sovereign bonds would show complete resilience to geopolitical risks. The strongest effects were found in Hungary, while somewhat weaker effects that were still statistically significant were also found in the markets of Poland, Latvia, and Lithuania. Although the impact of geopolitical risk was not statistically significant for other markets, the estimate was positive for all countries.

Overall, the results suggest that the impact of geopolitical risk on sovereign bond markets in Europe is diverging. The intensity of the effect varies depending on the region, the frequency of the data, and the estimation methodology used. Data with a daily frequency are more sensitive and reveal more significant correlations between geopolitical factors and bond returns. This suggests that, due to its characteristics and inherent short-term shocks, geopolitical risk should be modelled on a daily basis. Furthermore, the effects are found to intensify with a lag of more than one day. These findings could help investors adjust their portfolios more effectively in response to geopolitical shocks and assist supervisors in safeguarding financial stability.

Author contributions:

Rytė Panciriovaitė: conceptualization, methodology, formal analysis, investigation, writing – original draft, writing – review and editing, visualization.

Linas Jurkšas: conceptualization, methodology, writing – review and editing.

Afonso, A., Alves, J., & Monteiro, S. (2024). Beyond borders: Assessing the influence of Geopolitical tensions on sovereign risk dynamics. European Journal of Political Economy, 83, 102550. https://doi.org/10.1016/j.ejpoleco.2024.102550

Afonso, A., Arghyrou, M., & Kontonikas, A. (2015). The Determinants of Sovereign Bond Yield Spreads in the EMU. SSRN Electronic Journal. http://dx.doi.org/10.2139/ssrn.2611958

Ahmed, F., Gurdgiev, C., Sohag, K., Islam, M. M., & Zeqiraj, V. (2024). Global, local, or glocal? Unravelling the interplay of geopolitical risks and financial stress. Journal of Multinational Financial Management, 75, 100871. https://doi.org/10.1016/j.mulfin.2024.100871

Baur, D. G., & Smales, L. A. (2020). Hedging geopolitical risk with precious metals. Journal of Banking and Finance, 117, Article 105823. https://doi.org/10.1016/j.jbankfin.2020.105823

Będowska-Sójka, B., Demir, E., & Zaremba, A. (2022). Hedging Geopolitical Risks with Different Asset Classes: A Focus on the Russian Invasion of Ukraine. Finance Research Letters, 50, 103192. https://doi.org/10.1016/j.frl.2022.103192

Beirne, J., Renzhi, N., Sugandi, E., & Volz, U. (2021). COVID-19, asset markets and capital flows. Pacific Economic Review, 26(4), 498-538. https://doi.org/10.1111/1468-0106.12368

Bondarenko, Y., Lewis, V., Rottner, M., & Schüler, Y. S. (2023). Geopolitical risk perceptions. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.4441353

Bossman, A., & Gubareva, M. (2023). Asymmetric impacts of geopolitical risk on stock markets: A comparative analysis of the E7 and G7 equities during the Russian-Ukrainian conflict. Heliyon, 9(2), e13626. https://doi.org/10.1016/j.heliyon.2023.e13626

Bratis, T., Kouretas, G. P., Laopodis, N. T., & Vlamis, P. (2024). Sovereign credit and geopolitical risks during and after the EMU crisis. International Journal of Finance & Economics, 29(3), 3692-3712. https://doi.org/10.1002/ijfe.2852

Caldara, D., Iacoviello, M., 2022. Measuring geopolitical risk. American Economic Review, 112(4), 1194–1225. https://doi.org/10.1257/aer.20191823

De Wet, M. C. (2023). Geopolitical Risks and Yield Dynamics in the Australian Sovereign Bond Market. Journal of Risk and Financial Management, 16(3), 144. https://doi.org/10.3390/jrfm16030144

Dieckelmann, D., Kaufmann, C., Larkou, C., McQuade, P., Negri, C., Pancaro, C., & Rößler, D. (2024). Turbulent times: geopolitical risk and its impact on euro area financial stability. Financial Stability Review, European Central Bank, vol. 1. https://www.ecb.europa.eu/press/financial-stability-publications/fsr/special/html/ecb.fsrart202405_01~4e4e30f01f.en.html

Fatmawatie, N., Endri, E., & Husein, D. (2024). Macroeconomic factors and government bond yield in Indonesia. Public and Municipal Finance, 13(1), 95–105. https://doi.org/10.21511/pmf.13(1).2024.08

Galloppo, G., Paimanova, V., Aliano, M. (2015), Volatility and Liquidity in Eastern Europe Financial Markets under Efficiency and Transparency Conditions, Economics and Sociology, Vol. 8, No 2, pp. 70-92. DOI: 10.14254/2071-789X.2015/8-2/6

Gopinath, G. (2024). Speech: Geopolitics and its Impact on Global Trade and the Dollar. IMF. https://www.imf.org/en/News/Articles/2024/05/07/sp-geopolitics-impact-global-trade-and-dollar-gita-gopinath

Heryán, T., & Ziegelbauer, J. (2016). Volatility of Yields of Government Bonds Among GIIPS Countries During the Sovereign Debt Crisis in the Euro Area. Equilibrium. Quarterly Journal of Economics and Economic Policy, 11(1), pp. 61-74. https://journals.economic-research.pl/eq/article/view/145

Hsing, Y. (2015). Determinants of the Government Bond Yield in Spain: A Loanable Funds Model. International Journal of Financial Studies, 3(3), 342-350. https://doi.org/10.3390/ijfs3030342

Husein, D., & Endri, E. (2024). Determinants of Indonesia Government Bonds Yield Period 2019-2022. Devotion Journal of Research and Community Service, 5(1), 67–74. https://doi.org/10.59188/devotion.v5i1.660

Yakubovskiy, S., Dominese, G., Rodionova, T. ., & Derenko, V. (2021). Determinants of the Government Bond Yields of Italy, Spain, Portugal and Greece. Journal Global Policy and Governance, 10(1), 23-34. https://doi.org/10.14666/2194-7759-10-1-002

Jalkh, N., & Bouri, E. (2022). Global geopolitical risk and the long- and Short-Run impacts on the returns and volatilities of US treasuries. Defence and Peace Economics, 35(3), 339–366. https://doi.org/10.1080/10242694.2022.2150808

Jawadi, F., Rozin, P., Gnegne, Y., & Cheffou, A. I. (2024). Geopolitical risks and business fluctuations in Europe: A sectorial analysis. European Journal of Political Economy, 85, 102585. https://doi.org/10.1016/j.ejpoleco.2024.102585

Jurkšas, L., & Kropienė, R. (2014). Macroeconomic Determinants of Lithuanian Government Security Prices. Ekonomika, 93(4), 7-23. https://doi.org/10.15388/Ekon.2014.93.5037

Krippner, L. (2020). Shadow interest rates | LJKMFA https://www.ljkmfa.com/visitors/

Lee, C., Tang, H., & Li, D. (2022). The roles of oil shocks and geopolitical uncertainties on China’s green bond returns. Economic Analysis and Policy, 74, 494-505. https://doi.org/10.1016/j.eap.2022.03.008

Malešević Perović, L. (2015). The impact of fiscal positions on government bond yields in CEE countries. Economic Systems, 39(2), 301-316. https://doi.org/10.1016/j.ecosys.2014.10.006

Millo, G. (2017). Robust Standard Error Estimators for Panel Models: A Unifying Approach. Journal of Statistical Software, 82(3), 1–27. https://doi.org/10.18637/jss.v082.i03

Nittayakamolphun, P., Bejrananda, T., & Pholkerd, P. (2024). Geopolitical Risk And Responses To Financial Markets. ABAC Journal, Vol. 44 No. 4. https://doi.org/10.59865/abacj.2024.12

Pinho, A., & Barradas, R. (2021). Determinants of the Portuguese government bond yields. International Journal of Finance & Economics, 26(2), 2375–2395. https://doi.org/10.1002/ijfe.1912

Poghosyan, T. (2014). Long-run and short-run determinants of sovereign bond yields in advanced economies. Economic Systems, 38(1), 100-114. https://doi.org/10.1016/j.ecosys.2013.07.008

Sehgal, S., & Singh, J. (2024). Impact of global and domestic factors on Indian government bond yields. Asia-Pacific Financial Markets. https://doi.org/10.1007/s10690-024-09459-6

Subramaniam, S. (2022). Geopolitical uncertainty and sovereign bond yields of BRICS economies. Studies in Economics and Finance, 39(2), 311–330. https://doi.org/10.1108/sef-05-2021-0214

Swistek, G., & Paul, M. (2023). Geopolitics in the Baltic Sea Region: the “Zeitenwende” in the context of critical maritime infrastructure, escalation threats and the German willingness to lead. SWP Comment, No. 9/2023, Stiftung Wissenschaft und Politik (SWP), Berlin. https://doi.org/10.18449/2023C09

Tang, Y., Chen, X. H., Sarker, P. K., & Baroudi, S. (2023). Asymmetric effects of geopolitical risks and uncertainties on green bond markets. Technological Forecasting and Social Change, 189, 122348. https://doi.org/10.1016/j.techfore.2023.122348

Triki, M. B., & Ben Maatoug, A. (2021). The GOLD market as a safe haven against the stock market uncertainty: Evidence from geopolitical risk. Resources Policy, 70, 101872. https://doi.org/10.1016/j.resourpol.2020.101872

Varirahartia, D., & Santoso Marsoem , B. (2022). Effect of Bonds Maturity Date, Interest Rates, Inflation, Exchange Rates and Foreign Exchange Reserves on Yield To Maturity of Government Bonds 2014-2020. Jurnal Syntax Admiration, 3(2), 373-387. https://doi.org/10.46799/jsa.v3i2.398

1 The author also included Slovenia, but, in this study, this country is replaced by Finland due to the prevailing higher geopolitical tensions in the country and the adjacent territorial borders with Russia. Although Finland is often grouped with Western or Northern Europe in other classifications (at least when it is not related to geopolitics), its direct 1340 km border with Russia and historical exposure to regional security concerns justify its inclusion in the Eastern group. This classification is based on the assumption that geographical proximity to Russia means that geopolitical shocks have a stronger impact on sovereign bond yields, thereby making Finland’s risk profile more similar in this respect to Eastern European countries than to Western European markets.

2 Different inflation rates were chosen due to the limited availability of data – the Harmonised Index of Consumer Prices (HICP) is not published daily, and therefore it was decided to include inflation expectations.

3 Model results are not presented for the sake of brevity, but can be made available by the authors upon reasonable request.

4 The results of the models are also not presented for brevity but can be provided by the authors upon reasonable request.