Ekonomika ISSN 1392-1258 eISSN 2424-6166

2026, vol. 105(2), pp. 40–62 DOI:https://doi.org/10.15388/Ekon.2026.105.2.3

Dr. Karim Farag

Lecturer in Finance and Accounting

Faculty of Economics and Business Administration

Berlin School of Business and Innovation (BSBI), Berlin, Germany

karim.shehata@berlinsbi.com

https://orcid.org/0009-0005-5561-3482

Dr. Lawrence Ibeh

Lecturer in Data Science

Faculty of Computer Science and Informatics

Berlin School of Business and Innovation (BSBI), Berlin, Germany

lawrence.ibeh@berlinsbi.com

https://orcid.org/0009-0008-5935-3464

Dr. Noah Mutai

Lecturer in Applied Statistics

Faculty of Economics and Business Administration

Berlin School of Business and Innovation (BSBI), Berlin, Germany

noah.mutai@berlinsbi.com

https://orcid.org/0000-0001-9677-223X

Abstract. Artificial intelligence (AI) has become a contentious topic in the financial services sector, especially regarding its capacity to provide more accurate bank risk predictions than the traditional econometric models. However, limited research has so far been conducted in the MENA countries. In this context, the study aims to forecast bank stability across the MENA region by first validating the variables using econometric methods, and then, by applying machine learning (ML) algorithms to develop early warning systems that would improve risk assessment and financial resilience. By using panel data from 2000 to 2020, the research analyzed a sample of 33 listed commercial banks from six MENA countries. The findings demonstrated that econometric analysis confirms the importance of conventional bank-specific and macroeconomic variables in influencing bank stability, while the ML results indicated that the Gradient Boosting machine learning model achieved the highest accuracy score, with bank profitability (ROA), asset size, solvency, unemployment, and inflation identified as the most influential features. In this regard, in order to enhance predictive accuracy and address stability concerns, the study recommends that banks in the MENA region should adopt this machine learning approach. Additionally, it advises that regulators should utilize ML insights to develop policies aimed at strengthening the financial stability of MENA banks.

Keywords: Machine learning; Bank stability; Gradient Boosting; Early warning systems; MENA banking sector.

________

Received: 29/09/2025. Accepted: 16/03/2026

Copyright © 2026 Karim Farag, Lawrence Ibeh, Noah Mutai. Published by Vilnius University Press

This is an Open Access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Long-term bank stability is essential for maintaining an efficient financial system that supports economic growth in countries. However, banks face various risks, including operational risk, liquidity risk, interest rate risk, insolvency risk, technology risk, foreign currency risk, income diversification risk, sovereignty risk, political risk, economic risk, and credit risk, all of which affect their financial stability at different levels. Among these, credit risk and capital risk are the most critical because of their severe impact on bank stability (Abdou et al., 2025). Credit risk results in higher loan losses, which are absorbed by a bank’s equity capital, thereby impacting its solvency; consequently, capital risk arises, threatening the bank’s stability and survival. Capital risk refers to the possibility that a bank’s capital may be inadequate to cover losses from loans and other investments (Hamada et al., 2025).

Farag et al. (2025) suggest that banks remain stable when they maintain consistent earnings, lower levels of credit risk, and an appropriate amount of equity capital relative to risky assets to absorb unexpected losses. For this reason, academics and risk managers use measures such as the bank Z-score, non-performing loan (NPL) ratio, and capital adequacy ratio (CAR) to assess their financial stability. The bank Z-score is calculated by dividing the sum of the Return on Assets (ROA) and CAR by the standard deviation of the ROA; a higher Z-score indicates greater financial stability in banks.

Shehata and Ali (2025) claim that banks play a crucial role in fostering global economic growth. They perform extensive credit assessments on loan applications to allocate funds to qualified borrowers, thereby supporting efficient economic development. However, as the environment becomes more dynamic due to rapid technological advances, banks must adapt to survive. Therefore, banks need to go beyond traditional econometrics by adopting artificial intelligence to improve predictions of bank stability.

Farag et al. (2025) found that bank-specific and macroeconomic variables significantly influence bank stability in European countries and identified that machine learning algorithms play a crucial role in enhancing the prediction of bank stability. Meanwhile, Eldomiaty et al. (2022), Moudud-Ul-Huq et al. (2022), Mabkhot & Al-Wesabi (2022), Djebali (2024), Alaoui and Raghibi (2025), and Afzal et al. (2025) used traditional econometric methods and discovered that bank-specific and macroeconomic factors greatly affect the financial stability of banks in the MENA region. However, they did not employ machine learning to develop more precise predictive models for bank stability in the region. Therefore, this research raises the question: Do machine learning algorithms provide more accurate predictions of bank stability compared to the traditional econometric methods?

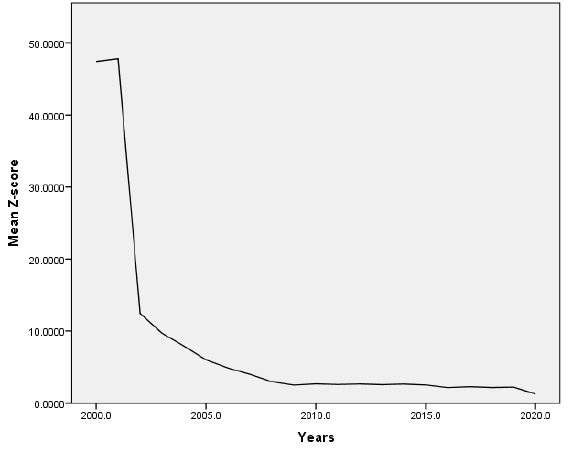

Additionally, Figure 1 shows the evolution of the Z-score for banks in the MENA countries from 2000 to 2020. The Z-score sharply declined between 2000 and 2003, then remained at lower, stable levels from 2003 to 2019 before gradually dropping again. Consequently, banks in the MENA region exhibited low Z-scores, which indicates an increased insolvency risk.

Source: Created by the author by using SPSS software.

As a result, MENA banks are more susceptible to financial shocks, which highlights the importance of further research to identify factors that affect bank stability, and to create AI-based models that provide better insights for regulators and banking professionals. This can improve prediction accuracy and address low z-score levels.

Eldomiaty et al. (2022) employed the Pooled Ordinary Least Squares (OLS) model to examine the factors influencing bank stability, by using a sample of 33 listed commercial banks from six MENA countries. Their results showed that bank efficiency, measured by the cost-income ratio, and unemployment negatively impact bank stability. They explain that a decrease in the cost-to-income ratio indicates an improved bank efficiency, which, in turn, enhances stability. Additionally, Moudud-Ul-Huq et al. (2022) employed the GMM method and found that market competition has a positive influence on bank stability in MENA countries. Mabkhot and Al-Wesabi (2022) employed the Panel Dynamic OLS Estimator to explore macroeconomic factors affecting bank stability in the Gulf Cooperation Council (GCC) countries.

Abdou et al. (2025) define credit risk as the likelihood of borrowers failing to meet their loan commitments, measured by the Non-Performing Loan (NPL) ratio. Rising NPL ratios weaken solvency levels, leading to a decreased bank stability. Essentially, a bank’s stability depends on its asset quality, which is affected by credit risk exposure. Giraldo et al. (2024) found that financial openness boosts bank stability by reducing the credit risk and increasing the Capital Adequacy Ratio (CAR) and liquidity. They also noted that inflation and oil prices undermine the bank stability, as spikes in oil prices raise inflation, lower asset quality, and increase instability. Lachaab (2023) argues that credit risk negatively affects bank stability in the MENA region, as higher NPL ratios erode the asset quality, decrease capital, and threaten the overall stability. Ghenimi et al. (2017) describe liquidity risk as the risk of not having enough liquid assets to meet short-term obligations, which negatively impacts stability.

Khemiri (2023) clarified that the Loan-To-Deposit (LTD) ratio has been used as a measure of liquidity risk. An increase in the LTD ratio worsens the liquidity risk by encouraging excessive lending driven by deposits, which raises both credit risk and liquidity risk, which are both detrimental to stability. Djebali (2024) employed GMM to study how economic and financial freedom affected bank stability from 2005 to 2020. Their findings show that financial freedom, investment freedom, and the overall economic freedom are positively associated with bank stability in the MENA countries, thus implying that an increased economic freedom fosters innovation and entrepreneurship which strengthen banks. The regression results of Alaoui and Raghibi (2025) demonstrated that liquidity creation positively influences bank stability, but only up to a threshold of 52.32%, beyond which, the benefit diminishes. This suggests that moderate liquidity creation supports the financial health of African banks.

Moreover, Afzal et al. (2025) used GMM to examine fintech’s impact on bank stability, analyzing data from 94 banks across ten MENA countries from 2011 to 2023. Their results showed that fintech positively affects bank stability, motivating banks to adopt technological solutions. Shehata and Ali (2025) applied machine learning algorithms to predict bank performance in Egypt, by using Return on Assets (ROA) as a proxy and considering both bank-specific and macroeconomic data. The Random Forest and Logistic Regression models achieved accuracy scores of 94%, demonstrating machine learning’s effectiveness in prediction. The feature importance analysis identified corporate credit risk, capital risk, efficiency, size, and income diversification as significant factors influencing bank performance. Finally, Abdou et al. (2025) and Hamada et al. (2025) used machine learning techniques to assess Egyptian banks, finding that the Random Forest model accurately predicts bank stability by combining CAMELS-based variables with macroeconomic indicators such as GDP growth, inflation, and unemployment.

Tanaka et al. (2016) used a random forest model with a sample of 18,391 banks from OECD countries from 1986 to 2014. The results showed that the random forest outperformed standard Early Warning Systems in predicting bank failures. Additionally, Chiaramonte and Casu (2017) employed a pooled logit model with a sample of 513 banks, and their findings indicated that boosting liquidity and capital levels reduces the likelihood of bank failure in Europe. Furthermore, Ekinci and Erdal (2017) used machine learning methods to forecast bank failures with a sample of 37 Turkish banks, covering panel data from 1997 to 2001, while considering CAMELS-based variables. The results suggest that hybrid ensemble learning models are reliable in predicting bank failures in Turkey. Likewise, Bongini et al. (2018) applied regression to a sample of 355 banks from Central, Eastern, and Southeastern European countries from 1995 to 2017. Their findings suggest that the estimated model is weak and cannot be relied upon as a tool for predicting bank stability.

Furthermore, Gogas et al. (2018) employed SVM on a sample of 1,433 US banks for a panel data set from 2007–2013, with the model achieving an accuracy score of 99.22%. Le and Viviani (2018) used a sample of 3,000 U.S. banks, by applying machine learning algorithms with CAMELS-based variables, and found that k-nearest neighbors and artificial neural networks are the most accurate models for predicting bank failures. Moreover, Jing and Fang (2018) utilized machine learning algorithms such as logit, neural networks, and Support Vector Machines (SVM) to predict bank failure in the US during 2002–2010, by using CAMELS-based variables. The empirical findings show that the logit model is robust and reliable for predicting bank failures.

Kolari et al. (2019) used the AdaBoost ensemble to predict financial distress in 91 European banks, based on variables from the CAMELS system. The results indicated that the model could identify over 98% of failing and passing banks in the training sample, thus confirming its accuracy in forecasting bank stability. Ali and Puah (2019) used regression analysis to examine factors affecting bank stability in Pakistan. They found that the bank size, funding risk, liquidity risk, and profitability all significantly impact stability, by arguing that an increasing bank size enhances financial health through diversification, reduces failures, and stabilizes Pakistani banks.

Additionally, Carmona et al. (2019) noted that lower levels of retained earnings relative to average equity, ROA, and CAR increase the risk of bank failures in US credit markets. Shrivastava et al. (2020) applied regression and machine learning techniques to data from 58 Indian banks from 2000 to 2017, and went on to find that AdaBoost achieved the highest accuracy in predicting bank stability. Furthermore, Petropoulos et al. (2020) used machine learning models based on CAMELS variables to predict bank insolvencies in US banks, with the Random Forest model showing the highest accuracy for identifying distress. In this context, Liu et al. (2021) argued that traditional models like econometrics are less reliable for building robust estimates due to criticism of their restrictive regression assumptions. Trung et al. (2021) applied regression to investigate the determinants of bank stability using a sample of 27 Vietnamese banks with panel data from 2008 to 2019. Their findings demonstrated that credit growth, liquidity, and bank size are positively associated with stability, implying that greater credit expansion and diversification reduce risk and increase profitability, leading to more stability.

Chand et al. (2021) performed fixed-effect regression with the Z-score as a proxy for bank stability and found that the bank size and the Herfindahl-Hirschman index have a significantly positive impact on stability, which suggests that greater concentration and diversification bolster stability. Kharabsheh and Gharaibeh (2022) used pooled effect regression on 13 banks listed on the Amman Stock Exchange from 2011 to 2018, discovering that SME loans and the Capital Adequacy Ratio (CAR) positively influence bank stability in Jordan, while liquidity risk, credit risk, and financial inclusion negatively affect it. They argue that higher CAR provides a buffer against losses, thus improving stability, while increases in the credit risk raise non-performing loans, thus harming profitability and stability. Additionally, Shahriar et al. (2023) applied fixed-effect regression on panel data from 2004–2018, revealing that the net interest margin positively impacts stability, which indicates that more profitable banks are less prone to risky investments, and thus are more stable.

Yitayaw et al. (2023) used a two-step GMM on Ethiopian banks from 2014 to 2020, finding that lending rates and GDP growth promote stability, as thriving economies enhance the repayment ability and reduce credit risks. Le and Mishra (2023) applied GMM to 6,433 banks from 109 countries between 2005 and 2019, discovering that the climate risk negatively affects the financial stability of small banks with a low CAR. Kanapiyanova et al. (2023) used a two-step system GMM to examine the drivers of bank stability in QISMUT countries from 2011 to 2018, identifying that the bank efficiency, profitability, and inflation influence stability. Yakubu & Bunyaminu (2023) demonstrated via GMM that regulatory capital requirements improve stability in Sub-Saharan Africa, and asserted that well-capitalized banks have larger loss buffers, which enhances stability. Iqbal et al. (2024) used GMM on Islamic banks in 16 Asian countries from 2010 to 2019, finding that liquidity risk, GDP growth, and inflation significantly affect stability.

Kaur and Kaur (2025) employed panel regression to analyze bank stability factors in India from 2005 to 2022, revealing that banks with higher profitability and capital relative to assets are more stable. Farag et al. (2025) combined econometrics and machine learning to predict European bank stability, finding that income diversification, ROA, and inflation significantly influence the bank Z-score. The machine learning models identified profitability, credit risk, income diversification, capital risk, unemployment, and inflation as the most important features in this regard. The Random Forest and SVM models achieved scores of 96.39% and 97.59%, respectively, underscoring the importance of both bank-specific and macroeconomic variables in predicting stability.

Based on a comprehensive review of current studies, most research has concentrated on Western and Asian countries, while Eldomiaty et al. (2022), Moudud-Ul-Huq et al. (2022), Mabkhot and Al-Wesabi (2022), Djebali (2024), Alaoui and Raghibi (2025), and Afzal et al. (2025) employed traditional econometrics to examine the factors influencing bank stability in the MENA region. Consequently, to the best of the researchers’ knowledge, although ML has already demonstrated superior prediction accuracy over econometrics in the United States and Europe, no prior studies have utilized machine learning algorithms to forecast bank stability in MENA countries, which highlights the importance of this research in filling such a methodological gap in the literature. Therefore, this study aims to implement machine learning algorithms after validating the selected variables using panel regression models to predict bank stability in the MENA region. The study compares the performance of different models with the objective to determine the most accurate and suitable predictive ML model, thereby underscoring the novelty and significance of this research in addressing the literature gap and developing early warning systems that enhance risk assessment and financial resilience.

Accordingly, the paper has presented the following hypotheses in the framework of the present research:

H1: Bank-specific factors (such as their credit risk, operating efficiency, capital risk, and profitability) influence bank stability.

H2: Macroeconomic factors (such as GDP, inflation, and unemployment) influence bank stability.

H3: Machine learning algorithms, particularly the Gradient Boosting model, provide more accurate predictions of the bank stability compared to the traditional methods, like Logistic Regression.

This study aims to predict bank stability by using nine independent variables: six bank-specific variables (bank profitability, efficiency, asset size, capital risk, liquidity, and credit risk) and three macroeconomic variables (economic growth, inflation, and unemployment), along with one dependent variable (bank stability) measured by the Z-score, as shown in Table 1. Additionally, as shown in Table 2, this research focuses on the MENA region, including six countries (Kingdom of Saudi Arabia (KSA), Kuwait, Qatar, UAE, Egypt, and Morocco), with an unbalanced dataset comprising 685 observations from 2000 to 2020. Bank-specific data are collected from financial statements of published annual reports, while macroeconomic data are sourced from the World Development Indicators database.

|

Variables |

Measurements |

|---|---|

|

Dependent Variable: |

|

|

Z Score |

Zscore = CAR + ROA / σROA Capital Adequacy Ratio (CAR) = Capital/Total Assets ratio ROA = Net profit/Total assets σROA = Volatility of Banks’ ROA being measured by the standard deviation of ROA for the first two years rolling up to 20 years. The rolling basis ensures that the time-varying volatility of ROA is accommodated. |

|

Independent Variables: |

|

|

Bank-specific variables: |

|

|

Profitability |

ROA ROE = Net profit/Total equity NIM = (Interest income – Interest expenses)/Average earning assets |

|

Operating Efficiency |

Expenses to income ratio = Total expenses / Total income |

|

Asset Size |

Log to total assets |

|

Capital risk |

CAR |

|

Liquidity risk |

Loan/deposit ratio = Total loans / Total deposits |

|

Credit risk |

Non-Performing Loan ratio = Non-performing loans/Total loans |

|

Macroeconomic variables: |

|

|

Inflation |

% change in CPI |

|

Unemployment |

Unemployment rate |

|

Economic growth |

Real GDP growth rate |

|

Banks |

Country |

|

National Commercial Bank (NCB) |

KSA |

|

Saudi Hollandi Bank (Alawwal) |

KSA |

|

Riyad Bank (RIBL) |

KSA |

|

Saudi British Bank (SAAB) |

KSA |

|

Samba Financial Group |

KSA |

|

Arab National Bank (ANB) |

KSA |

|

Banque Saudi Fransi JSC |

KSA |

|

National Bank of Kuwait |

Kuwait |

|

Gulf Bank |

Kuwait |

|

Commercial Bank of Kuwait (CBK) |

Kuwait |

|

Burgan Bank (BURG) |

Kuwait |

|

Al Ahli Bank of Kuwait (ABK) |

Kuwait |

|

Qatar National Bank |

Qatar |

|

Commercial Bank of Qatar (COMB) |

Qatar |

|

Doha Bank |

Qatar |

|

Ahli Bank (AABQ) |

Qatar |

|

Al Khalij Commercial Bank (KCB) |

Qatar |

|

Abu Dhabi Commercial Bank (ADCB) |

UAE |

|

National Bank of Fujairah PJSC |

UAE |

|

The National Bank of Ras Al-Khaimah |

UAE |

|

Commercial Bank International (CBI) |

UAE |

|

National Bank of Umm Al-Qaiwain (NBQ) |

UAE |

|

Mashreqbank |

UAE |

|

The National Bank of Kuwait – Egy |

Egypt |

|

Société Arabe Internationale de Banque |

Egypt |

|

Suez Canal Bank |

Egypt |

|

Credit Agricole Egypt (CIEB) |

Egypt |

|

Commercial International Bank (CIB) |

Egypt |

|

Egyptian Gulf Bank (EGB) |

Egypt |

|

Attijariwafa Bank |

Morocco |

|

Banque Centrale Populaire (BCP) |

Morocco |

|

Crédit Agricole du Maroc (CDM) |

Morocco |

|

Bank of Africa Banque Marocaine du Commerce Extérieur (BCME) |

Morocco |

The study aims to improve the prediction accuracy of bank stability by using machine learning algorithms in its pursuit to find more unbiased and robust models. In doing so, the research first applied econometrics by using the fixed and random effects logit estimations to validate the selected independent variables, and then employed different types of machine learning algorithms, such as decision trees, Support Vector Machine (SVM), and Gradient Boosting, to identify the most fit predictive ML.

The paper performs a binary classification of bank stability in the MENA region by using the Z-score, which is transformed into a dichotomous outcome (High stability = 1, top 34% by Z-score; Not high = 0, bottom 66%). Predictors include bank-specific variables (ROE, ROA, NIM, Operating Efficiency, Asset Size, Solvency, Liquidity, Credit Risk) and macroeconomic variables (Inflation, Unemployment, GDP).

The binary classification threshold based on the Z-score (34th/66th percentile split) was selected by using both empirical and theoretical reasoning. First, the Z-score distribution in this dataset is highly right-skewed, which means that fixed cutoff values are not meaningful indicators of stability. Using the empirical percentile ensures that the classification reflects the actual distribution of bank insolvency risk.

Second, the 34th percentile corresponds approximately to one standard deviation below the mean in a normal distribution. This aligns with conventional financial distress modelling, where a one-standard-deviation threshold is often used to identify institutions with materially higher risk levels.

Third, this threshold results in a reasonably balanced binary classification. More extreme splits (e.g., bottom 10%) would lead to severe class imbalance, making machine learning models difficult to train, whereas a median split (50/50) would not sufficiently differentiate lower-risk and higher-risk banks. The 34% cutoff therefore strikes an appropriate balance between statistical validity and practical model performance.

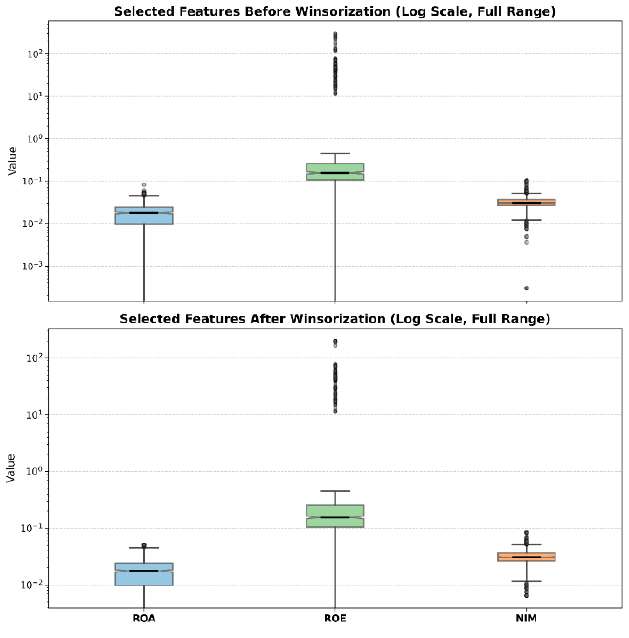

Data are read from CSV files. It specifically involved normalizing variable names, converting all predictors into a numeric format, and winsorizing values at the 1st and 99th percentiles so that to reduce the impact of outliers. Records with missing values were excluded. The dataset was split into training and testing subsets (75/25) using stratified sampling to preserve class balance. Features were standardized when training the SVM classifier in order to ensure scale invariance, while tree-based models were trained on raw values. As seen in Figure 2, there is a reduction in extreme values for ROA, ROE, and NIM Preprocessing, therefore substantially reducing the impact of outliers while preserving the central distribution of key variables.

Three classifiers are fit:

Performance is evaluated on the test set using Accuracy, F1 (binary), and AUC (Area Under the ROC Curve). We visualize per-model confusion matrices, per-model ROC curves, an all-models combined ROC plot, and feature importances for tree-based models and SVM-based permutation.

The study employed descriptive statistics, as shown in Table 3, to describe the collected data in terms of the number of observations, minimum, maximum, and standard deviation. The study used unbalanced data with 685 observations. The mean of the ROA is 1.8%, while the maximum reached 8.24% and the minimum is -8.5%. The standard deviation of .013 indicates stability in the profitability levels among the banks of the MENA countries. Conversely, bank efficiency, as measured by the cost-to-income ratio, has a mean of 39%, indicating that expenses account for 39% of the total income, which suggests moderate efficiency in banks. However, the standard deviation is high, reaching 0.15, which reveals that banks are experiencing substantial volatility in their efficiency, placing pressure on financial stability. Meanwhile, the NPL ratio has a mean of 6.9%, indicating that banks are exposed to high credit risk levels, which jeopardizes their survival and growth in credit markets, along with a standard deviation of 11.4%, illustrating high credit risk volatility. Furthermore, the Z-score has the highest STDEV, implying there are significant fluctuations in bank stability among the banks. Regarding the descriptive statistics of macroeconomic data, inflation has the highest STDEV, reaching .06, compared to GDP and UNEMP, with a mean of 6.3%, exceeding normal inflation rates, which consequently places more inflationary pressure on banks. In this respect, the credit risk and inflation could be the main factors influencing bank stability in the MENA region and play a pivotal role in improving the prediction performance of bank stability.

|

N |

Minimum |

Maximum |

Mean |

Std. Deviation |

|

|

ROA |

685 |

-.0858 |

.0824 |

.017520 |

.0127982 |

|

Cost/income |

685 |

.0000 |

1.7762 |

.393919 |

.1518838 |

|

ROE |

685 |

-3.04363 |

297.17390 |

9.4810034 |

32.67340404 |

|

Size |

661 |

1.79458 |

19.27612 |

6.91455 |

3.56576 |

|

Total Capital Ratio |

685 |

.0000 |

.4200 |

.178498 |

.0526152 |

|

Loans/deposits |

685 |

-1.3599 |

1.2597 |

.586270 |

.2901104 |

|

NIM |

685 |

.0000 |

.1024 |

.032048 |

.0122588 |

|

NPL |

685 |

.0000 |

.9494 |

.068730 |

.1136277 |

|

inflation |

685 |

-.0486 |

.2951 |

.063191 |

.0612430 |

|

unemployment |

685 |

.0011 |

.1358 |

.071579 |

.0404800 |

|

GDP |

685 |

-.08077 |

.28082 |

.035262 |

.049356 |

|

Z-score |

685 |

-2.5608 |

631.1473 |

8.039822 |

37.5390785 |

|

Valid N (listwise) |

661 |

In this section, the research examines the significance level of the selected conventional bank-specific and macroeconomic variables on the financial stability of the banks of the MENA region by employing panel regression models, such as the fixed and random effects logit estimations, with the objective to validate the importance of the variables before being applied to the ML.

The Hausman test was performed to compare the fixed-effects and random-effects specifications, as shown in Table 4. The test evaluates whether the regressors are correlated with the unobserved individual effects. The results were significant, indicating that this correlation cannot be ignored. Therefore, the fixed-effects estimator is the more reliable option, as demonstrated in Table 4. The differing significance levels of ‘Asset Size’ and ‘Inflation’ between the two models are consistent with this outcome: the random-effects estimates become biased when the correlation assumption is violated. Hence, the fixed effects model provides the appropriate basis for interpretation.

|

Test |

Degrees of freedom |

p-value |

Preferred model |

Justification |

|

12.47 |

4 |

0.014 |

Fixed effects |

The test indicates a correlation between regressors and unit effects; FE is consistent, while RE is not. |

As shown in the Tables (5–9) of the econometric analysis, the conventional bank-specific and macroeconomic variables significantly influence the financial stability of banks in the MENA region. Return on assets (ROA), which is a measure of profitability, was found to have a statistically significant positive effect on bank stability, thereby illustrating that an increasing profitability enhances bank stability, whereas the firm size, measured by the logarithm of assets, had a statistically significant negative relationship with bank stability, thus suggesting that size has limitations in enhancing the financial stability of banks. In other words, expanding assets would enhance diversification to mitigate the overall risk and strengthen financial stability in banks, but with limits. In Table 9, the results after taking the log demonstrate that NPL, which measures credit risk, has a significant negative impact on bank stability. This indicates that higher NPL raises loan losses, adversely affecting the banks’ solvency and profitability, thereby reducing bank stability.

(A) Pooled Logit with year-fixed effects; cluster-robust SE at bank level. Report odds ratios, 95% CIs, p-values; LR test vs. null; joint Wald tests for (i) bank-specific block, (ii) macro block.

|

|

Estimate |

Std. Error |

z value |

Pr(>|z|) |

|

ROA |

116.4593 |

29.9670 |

3.8863 |

0.0001 |

|

Efficiency |

-0.6441 |

1.6678 |

-0.3862 |

0.6994 |

|

Size |

-0.1483 |

0.0858 |

-1.7292 |

0.0838 |

|

NPL |

-5.5718 |

4.3806 |

-1.2719 |

0.2034 |

|

NIM |

12.0948 |

17.4031 |

0.6950 |

0.4871 |

|

GDP |

-7.9174 |

5.0929 |

-1.5546 |

0.1200 |

|

Inflation |

1.5386 |

4.5759 |

0.3362 |

0.7367 |

|

Unemployment |

-3.2908 |

10.8504 |

-0.3033 |

0.7617 |

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ‘ 1

Log-Likelihood: -207.3 Adj. Pseudo R2: 0.450483

BIC: 643.2 Squared Cor.: 0.597613

(B) FE Logit (conditional logit) with bank FE + year FE; cluster at bank. (If separation issues are encountered, fall back to LPM with bank FE + year FE + cluster-robust SE.)

|

|

Estimate |

Std.Error |

z value |

Pr(>|z|) |

|

ROA |

116.4593 |

29.9670 |

3.8863 |

0.0001*** |

|

Efficiency |

-0.6441 |

1.6678 |

-0.3862 |

0.6994 |

|

Size |

-0.1483 |

0.0858 |

-1.7292 |

0.0838* |

|

NPL |

-5.5718 |

4.3806 |

-1.2719 |

0.2034 |

|

NIM |

12.0948 |

17.4031 |

0.6950 |

0.4871 |

|

GDP |

-7.9174 |

5.0929 |

-1.5546 |

0.1200 |

|

Inflation |

1.5386 |

4.5759 |

0.3362 |

0.7367 |

|

Unemployment |

-3.2908 |

10.8504 |

-0.3033 |

0.7617 |

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ‘ 1

|

(Intr) |

roa |

effcnc |

size |

npl |

nim |

gdp |

infltn |

unmply |

|

|

roa |

-0.078 |

||||||||

|

efficiency |

-0.265 |

0.347 |

|||||||

|

size |

-0.2 |

-0.259 |

0.159 |

||||||

|

npl |

-0.369 |

0.216 |

0.204 |

0.117 |

|||||

|

nim |

0.255 |

-0.454 |

-0.005 |

-0.023 |

-0.106 |

||||

|

gdp |

-0.201 |

-0.253 |

-0.125 |

0.397 |

0.075 |

-0.011 |

|||

|

inflation |

0.129 |

-0.212 |

0.09 |

-0.146 |

-0.026 |

0.113 |

-0.169 |

||

|

unemploymnt |

-0.053 |

0.131 |

-0.385 |

-0.1 |

0.008 |

-0.252 |

0.421 |

-0.317 |

|

|

years |

-1 |

0.074 |

0.258 |

0.197 |

0.366 |

-0.258 |

0.198 |

-0.129 |

0.052 |

(D) Continuous robustness: Panel FE on Z-score (or log(1+Z-score) to handle the skew) with bank and year FE; cluster at bank; F-tests for joint significance. (These ties refer back to our original Z-score construction.)

|

|

Estimate |

Std.Error |

t value |

Pr(>|t|) |

|

ROA |

5.2918 |

81.2502 |

0.0651 |

0.9502 |

|

Efficiency |

2.9389 |

15.2561 |

0.1926 |

0.8536 |

|

Size |

-0.2515 |

0.2986 |

-0.8425 |

0.4318 |

|

NPL |

-11.9333 |

9.7143 |

-1.2284 |

0.2653 |

|

NIM |

456.9089 |

318.5952 |

1.4341 |

0.2015 |

|

GDP |

-8.8859 |

26.8309 |

-0.3312 |

0.7518 |

|

Inflation |

80.3088 |

84.6476 |

0.9487 |

0.3794 |

|

Unemployment |

-77.5615 |

134.5420 |

-0.5765 |

0.5853 |

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ‘ 1

RMSE: 34.1 Adj. R2: 0.128307

Within R2: 0.038768

|

Z-score (FE) |

log(1+Z) (FE) |

|

|---|---|---|

|

ROA |

5.292 |

33.673*** |

|

(81.250) |

(6.129) |

|

|

Efficiency |

2.939 |

-0.105 |

|

(15.256) |

(0.352) |

|

|

Size |

-0.252 |

-0.012 |

|

(0.299) |

(0.012) |

|

|

NPL |

-11.933 |

-1.314** |

|

(9.714) |

(0.432) |

|

|

NIM |

456.909 |

-1.616 |

|

(318.595) |

(3.723) |

|

|

GDP |

-8.886 |

-0.250 |

|

(26.831) |

(0.661) |

|

|

Inflation |

80.309 |

1.091 |

|

(84.648) |

(1.111) |

|

|

Unemployment |

-77.562 |

0.761 |

|

(134.542) |

(2.047) |

|

|

Observations |

685 |

677 |

|

R2 |

0.172 |

0.659 |

|

Within R2 |

0.039 |

0.350 |

Following the validation of the selected variables by using econometrics, in the next section, the paper employs Machine Learning (ML) to create a robust and unbiased predictive model by using Decision Tree, SVM, and Gradient Boosting algorithms.

In this section, the study employs machine learning algorithms, starting with 5-fold cross-validation to ensure robustness, followed by evaluating the accuracy of the ML models (Logistic Regression, Decision Tree, SVM, and Gradient Boosting algorithms), then conducting the ROC analysis, confusion matrix and finally, implementing the Feature Importance.

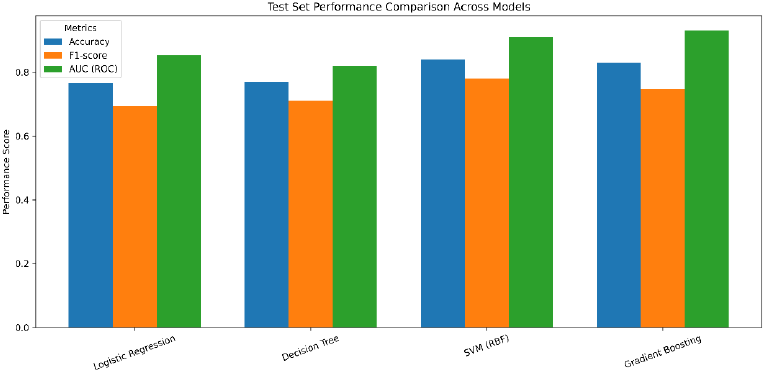

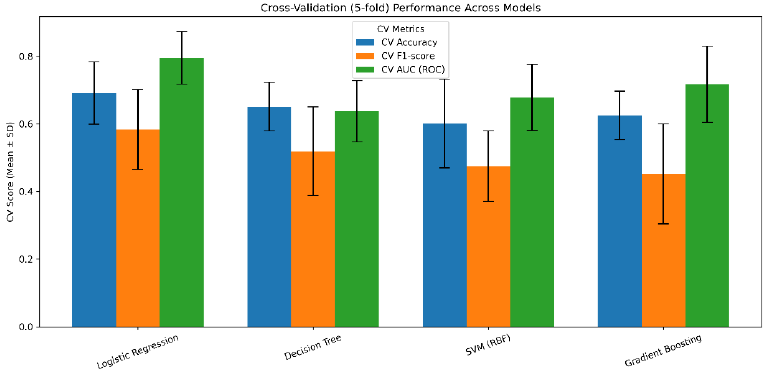

Table 10 demonstrates clear differences between traditional statistical modelling (Logistic Regression) and machine learning models across both test performance and cross-validation robustness.

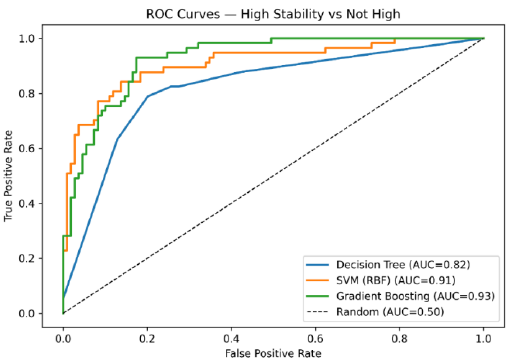

Gradient Boosting and SVM demonstrate the highest predictive performance on the test set, with AUC scores of 0.93 and 0.91, respectively. These values indicate strong discriminatory power and support the hypothesis that ML models outperform the traditional methods in predicting bank stability.

Logistic Regression, while performing reasonably well on the test set (AUC = 0.853), shows much more stable performance during cross-validation**, achieving the highest CV AUC (0.795). This stability indicates that Logistic Regression generalizes more consistently across the folds, although its peak performance remains lower than that of the ML models.

Machine learning models (especially Gradient Boosting and SVM) exhibit higher variance in cross-validation results, suggesting that while they can achieve higher performance on specific training–test splits, their results are more sensitive to data fluctuations.

Decision Tree is the weakest performer overall, with the lowest CV AUC (0.637). This is expected as single-tree models tend to overfit and lack the ensemble strengths of advanced ML methods.

Overall, the combined evidence supports the study’s hypothesis (H3) that machine learning models – and particularly ensemble and kernel-based approaches – can exceed traditional logistic regression in predictive capability. However, cross-validation results highlight that Logistic Regression remains the most stable and robust model across repeated sampling.

|

Model |

Test Accuracy |

Test F1 |

Test AUC |

CV Accuracy (Mean) |

CV Accuracy (SD) |

CV |

CV F1 (SD) |

CV AUC (Mean) |

CV AUC (SD) |

|

Logistic Regression |

0.765 |

0.693 |

0.853 |

0.691 |

0.092 |

0.583 |

0.118 |

0.795 |

0.078 |

|

Decision Tree |

0.77 |

0.71 |

0.82 |

0.651 |

0.072 |

0.519 |

0.131 |

0.637 |

0.090 |

|

SVM (RBF) |

0.84 |

0.78 |

0.91 |

0.601 |

0.131 |

0.475 |

0.104 |

0.678 |

0.098 |

|

Gradient Boosting |

0.83 |

0.748 |

0.93 |

0.625 |

0.072 |

0.452 |

0.148 |

0.717 |

0.112 |

The combined ROC plot, as shown in Figure 5, shows that Gradient Boosting consistently lies above the other curves across thresholds, with SVM remaining close behind. Both models substantially exceed the chance line (AUC = 0.5), supporting robust rank-ordering of stability risk.

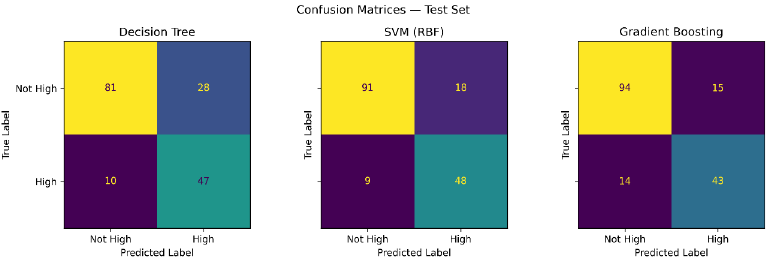

Per-model confusion matrices, as shown in Figure 6, indicate that Gradient Boosting and SVM improve true positive recognition of High stability while maintaining controlled false positives relative to the Decision Tree, which exhibits more threshold-sensitive trade-offs.

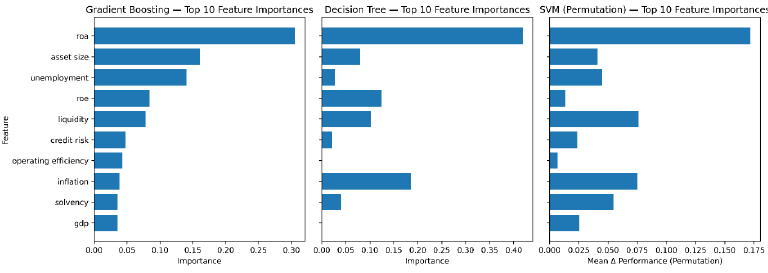

Figure 7 and Table 11 present the feature importance of the top 10 variables. Across all three models, several consistent predictors of bank stability emerge. Gradient Boosting assigns the highest weight to ROA (0.305), followed by Asset Size (0.160) and Unemployment (0.140), thus emphasizing the importance of profitability, size, and labor-market conditions in identifying stable banks. The Decision Tree similarly highlights ROA (0.419) and also considers Inflation (0.185) and ROE (0.125), indicating that tree splits often depend on profitability and macroeconomic thresholds.

The SVM permutation analysis supports these findings by providing a model-agnostic perspective. Here, ROA (0.172) and Liquidity (0.076) are the leading predictors, with Inflation (0.075) and Solvency (0.055) also playing significant roles. Compared to the tree-based methods, the SVM assigns more importance to liquidity and solvency indicators, aligning with theoretical expectations regarding capital adequacy and liquidity buffers in banking stability.

|

Feature |

Gradient Boosting |

Decision Tree |

SVM (Permutation) |

|

ROA |

0.3054 |

0.4189 |

0.1719 |

|

Asset size |

0.1604 |

0.0801 |

0.0412 |

|

Unemployment |

0.1402 |

0.0271 |

0.0450 |

|

ROE |

0.0843 |

0.1245 |

0.0135 |

|

Liquidity |

0.0782 |

0.1023 |

0.0763 |

|

Credit risk |

0.0475 |

0.0214 |

0.0237 |

|

Operating efficiency |

0.0430 |

0.0000 |

0.0072 |

|

Inflation |

0.0384 |

0.1854 |

0.0751 |

|

Solvency |

0.0360 |

0.0404 |

0.0548 |

|

GDP |

0.0360 |

0.0000 |

0.0255 |

The results suggest that profitability (ROA), the asset size, and macroeconomic variables, such as unemployment and inflation, are key factors across the models. Liquidity and solvency are more strongly emphasized when assessed through permutation importance, which highlights their stabilizing role. By contrast, Credit Risk (NPL ratio), while relevant, receives comparatively lower weights in all three approaches.

These patterns suggest that while profitability remains the dominant signal, structural resilience (size, solvency, liquidity) and broader economic conditions (unemployment, inflation) are also central to explaining variation in bank stability in the MENA region (see Figure 4, Table 3).

The econometric results confirm that profitability (ROA) is the strongest and most consistent determinant of bank stability across all model specifications, reinforcing the machine learning finding that profitability is the leading predictor of resilience among MENA banks. In both fixed and random effects logit estimations, a higher ROA significantly increases the likelihood of stability, suggesting that well-managed, profitable banks are better positioned to withstand shocks. Moreover, the random effects model identifies efficiency as a positive contributor and the bank size as a mild stabilizing factor, though the latter’s significance varies. Negative coefficients on inflation and the Net Interest Margin (NIM) indicate that macroeconomic pressures and excessive reliance on interest-based income can weaken stability, which is consistent with the macro-level variability captured in the machine learning results.

Furthermore, the Fixed Effects Logit model applied to the logarithmic variable showed that credit risk has a significantly negative effect on bank stability, while unemployment was insignificant. In contrast, the Machine Learning results indicated a relatively low importance for credit risk and attributed high importance to the unemployment rate. This discrepancy can be explained by the fact that econometric models assume ceteris paribus conditions, which highlight the significance of variables with causal effects; hence, the coefficients are based on the assumption that other factors stay constant, showing a strong impact on dependent variables. Conversely, ML methods focus on prediction accuracy and evaluate feature importance by their contribution to reducing the overall error. Therefore, if credit risk or unemployment rate correlates with other independent variables, its predictive power is likely to diminish.

Gradient boosting outperforms other machine learning methods because it can capture complex nonlinear relationships and feature interactions inherent in financial data. Unlike a decision tree, which is prone to overfitting, and Support Vector Machines (SVM), which depend on the kernel choice and parameter tuning, gradient boosting provides a better bias-variance balance and is more resistant to outliers and imbalanced data, thus improving predictive accuracy.

Therefore, the results support H1 that the bank-specific variables significantly influence bank stability, aligned with the previous articles of Ali and Puah (2019), Trung et al. (2021), Kanapiyanova et al. (2023), Kaur and Kaur (2025), and Farag et al. (2025). Additionally, the research findings also support H2 that the macroeconomic variables significantly influence bank stability and are consistent with the studies of Yakubu & Bunyaminu (2023), Kanapiyanova et al. (2023), Giraldo et al. (2024), and Farag et al. (2025). Furthermore, the study also supports H3 that Machine learning, specifically using the Gradient boosting method, can provide more accurate predictions of the bank stability compared to the traditional methods like Logistic Regression, which is consistent with the studies of Hamada et al. (2025) and Farag et al. (2025).

The study developed a reliable and robust ML predictive model using Gradient boosting to deliver an early forecast, improving the prediction of bank stability. This approach addresses the methodological gap identified in the literature and broadens the understanding of the determinants of bank stability.

Overall, the econometric evidence aligns with the hybrid model’s central argument: internal fundamentals – namely, profitability, efficiency, and prudent balance sheet management – remain the primary drivers of bank stability, while external macroeconomic variables exert a secondary but nontrivial influence. The convergence between econometric and AI-based findings strengthens the robustness of the hybrid approach, validating its use for early warning and policy applications in the MENA banking context.

Due to bank-specific data availability constraints in MENA countries, the study was limited to the period of 2000–2020, with six countries selected based on the largest banks in terms of assets and market share to support generalization of the results for the rest of the region. However, this limited sample may have failed to capture heterogeneity across all MENA countries, especially those with differences in regulatory frameworks, economic structures, and financial systems. Therefore, the results might be sensitive to country selection and may not be representative of the entire region. Moreover, given that the dataset comprises 685 observations, which is typically considered moderate, the potential for overfitting persists for decision tree models, as these models are acutely sensitive to the sample size due to their method of partitioning data into progressively smaller subsets based on feature splits. However, employing Gradient boosting helps in reducing variance and improving the robustness compared to the decision tree.

The findings show that ensemble methods (Gradient Boosting) and kernel methods (SVM with RBF) deliver strong discriminatory performance in predicting bank stability, thus surpassing the more interpretable but weaker Decision Tree baseline. This aligns with previous research on tabular financial data, where boosting effectively combines weak signals from multiple predictors, and kernel methods detect nonlinear relationships that simple splits might miss. From a practical perspective, the prominence of ROA, Asset Size, Solvency, and Liquidity as key predictors matches the established banking theory: banks that are more profitable, larger, and better-capitalized with stronger liquidity buffers tend to be more resilient. The comparatively lower, yet still significant, importance placed on Credit Risk is notable, while the appearance of Inflation and Unemployment in some models suggests that macroeconomic conditions influence stability but are not the main factors. These results emphasize the complementary roles of internal balance-sheet fundamentals and external economic conditions in shaping bank soundness in the MENA region.

Practically, the paper suggests that bankers, such as risk managers and credit risk analysts of the MENA banks, consider the results of econometrics and machine learning to enhance their credit decisions and address their bank stability issues. In other words, bankers could use the developed machine learning models to improve their risk management performance. Conversely, from a theoretical perspective, the paper recommends that, in future work, the authors consider factors beyond the variables used in this study, whether employing the same methodology or applying Artificial Neural Network (ANN) models and comparing them to the traditional machine learning models. This could enhance the accuracy of predictive models, leading to better risk management, higher stability levels, and improved financial resilience in the MENA region.

The literature highlights the limited adoption of Machine Learning (ML) in the banking sector within the MENA region, along with low Z-scores, which expose banks to a high level of insolvency risk. This situation urges policymakers or central banks in the MENA region to introduce new regulations requiring banks to utilize ML-based models alongside the traditional econometric models so that to improve risk management and provide better insights into bank stability determinants. The study developed a gradient boosting-based predictive model of bank stability that regulators can use to gain better insights into banks’ risk exposure, potentially improving their decisions and control over banks’ risk behavior. However, the black box of machine learning models restricts transparency and interpretability relative to econometric models, potentially impeding their adoption. Therefore, considering the results of the SHAP could ensure accountability.

This study has empirically demonstrated that machine learning can be effectively employed to forecast bank stability; overall, Gradient Boosting and SVM models offer robust, theory-aligned tools for early warning in the MENA region, with the asset size, credit risk, and solvency recognized as the most critical predictors. These findings suggest that early-warning systems for supervisory monitoring should focus on core financial fundamentals – capital adequacy, profitability, asset size, and liquidity – while also integrating macroeconomic indicators as contextual variables.

Abdou, D.M.S., Farrag, K., and Ali, L. (2025). Detecting Credit Risk in Egyptian Banks: Does Machine Learning Matter?. Ekonomika, 104(2), 78–94. https://doi.org/10.15388/Ekon.2025.104.2.5

Afzal, A.M., Abu Khalaf, B., Al-Naimi, M.S., and Samara, E. (2025). The Impact of Fintech on the Stability of Middle Eastern and North African (MENA) Banks. Risks, 13(6), 106. https://doi.org/10.3390/risks13060106

Alaoui Mdaghri, A. and Raghibi, A. (2025). On the nonlinear relationship between bank liquidity creation and financial stability: the moderating role of institutional quality in African economies. Journal of Business Economics, 95, 871–915. https://doi.org/10.1007/s11573-025-01226-x

Ali, M. and Puah, C.H. (2019). The internal determinants of bank profitability and stability: An insight from banking sector of Pakistan. Management research review, 42(1), 49–67. https://doi.org/10.1108/MRR-04-2017-0103

Carmona, P., Climent, F. and Momparler, A. (2019). Predicting failure in the US banking sector: An extreme gradient boosting approach. International Review of Economics & Finance, 61, 304–323. https://doi.org/10.1016/j.iref.2018.03.008

Chand, S.A., Kumar, R.R. and Stauvermann, P.J. (2021). Determinants of bank stability in a small island economy: a study of Fiji. Accounting Research Journal, 34(1), 22–42. https://doi.org/10.1108/ARJ-06-2020-0140

Chiaramonte, L. and Casu, B. (2017). Capital and liquidity ratios and financial distress. Evidence from the European banking industry. The British accounting review, 49(2), 138–161. https://doi.org/10.1016/j.bar.2016.04.001

Djebali, N. (2024). Assessing the determinants of banking stability in the MENA region: what role for economic and financial freedom? Journal of Banking Regulation, 25(2), 127–144. https://doi.org/10.1057/s41261-023-00220-z

Ekinci, A. and Erdal, H.İ. (2017). Forecasting bank failure: Base learners, ensembles and hybrid ensembles. Computational Economics, 49(4), 677–686. https://doi.org/10.1007/s10614-016-9623-y

Eldomiaty, T., Youssef, A., and Mahrous, H. (2022). The Robustness of the Determinants of Overall Bank Risks in the MENA Region. Journal of Risk and Financial Management, 15(10), 445. https://doi.org/10.3390/jrfm15100445

Farag, K., Ali, L., Mutai, N.C., Luqman, R., Mahmoud, A. and Krasniqi, N. (2025). Machine Learning for Predicting Bank Stability: The Role of Income Diversification in European Banking. FinTech, 4(2), 21. https://doi.org/10.3390/fintech4020021

Ghenimi, A., Chaibi, H. and Omri, M.A.B. (2017). The effects of liquidity risk and credit risk on bank stability: Evidence from the MENA region. Borsa Istanbul Review, 17(4), 238–248. https://doi.org/10.1016/j.bir.2017.05.002

Giraldo, C., Giraldo, I., Gomez-Gonzalez, J.E., and Uribe, J.M. (2024). Financial integration and banking stability: A post-global crisis assessment. Economic Modelling, 139, 106835. https://doi.org/10.1016/j.econmod.2024.106835

Gogas, P., Papadimitriou, T., and Agrapetidou, A. (2018). Forecasting bank failures and stress testing: A machine learning approach. International Journal of Forecasting, 34(3), 440–455. https://doi.org/10.1016/j.ijforecast.2018.01.009

Hamada, M. A., Farag, K., and Abiche, A. E. (2025). Early Prediction Detection of Retail and Corporate Credit Risks Using Machine Learning Algorithms. Emerging Science Journal, 9(2), 995–1012. https://doi.org/10.28991/ESJ-2025-09-02-025

Iqbal, M., Hakim, L., and Aziz, M.A. (2024). Determinants of Islamic bank stability in Asia. Journal of Islamic Accounting and Business Research. https://doi.org/10.1108/JIABR-07-2022-0174

Jing, Z. and Fang, Y. (2018). Predicting US bank failures: A comparison of logit and data mining models. Journal of Forecasting, 37(2), 235–256. https://doi.org/10.1002/for.2487

Kanapiyanova, K., Faizulayev, A., Ruzanov, R., Ejdys, J., Kulumbetova, D. and Elbadri, M. (2023). Does social and governmental responsibility matter for financial stability and bank profitability? Evidence from commercial and Islamic banks. Journal of Islamic Accounting and Business Research, 14(3), 451–472. https://doi.org/10.1108/JIABR-01-2022-0004

Kaur, M. and Kaur, M. (2025). Determinants of banking stability in India. The Bottom Line, 38(1), 49–70. https://doi.org/10.1108/BL-04-2023-0120

Kharabsheh, B. and Gharaibeh, O.K. (2022). Determinants of banks’ stability in Jordan. Economies, 10(12), 311. https://doi.org/10.3390/economies10120311

Khemiri, M.A. (2023). Testing the Non-Linear Relationship between Liquidity Risk and Bank Stability in the MENA Region. International Journal of Economics and Financial Issues, 13(4), 125. https://doi.org/10.32479/ijefi.14536

Kolari, J.W., López-Iturriaga, F.J. and Sanz, I.P. (2019). Predicting European bank stress tests: Survival of the fittest. Global Finance Journal, 39, 44–57. https://doi.org/10.1016/j.gfj.2018.01.015

Lachaab, M. (2023). The Cyclical Behavior of Credit and Liquidity Risks on Bank Stability in MENA Countries with a Dual Banking System. International Journal of Empirical Economics, 2(2). https://doi.org/10.1142/S2810943023500063

Le, A.T., Tran, T.P., and Mishra, A.V. (2023). Climate risk and bank stability: International evidence. Journal of Multinational Financial Management, 70, 100824. https://doi.org/10.1016/j.mulfin.2023.100824

Le, H.H. and Viviani, J.L. (2018). Predicting bank failure: An improvement by implementing a machine-learning approach to classical financial ratios. Research in international business and finance, 44, 16–25. https://doi.org/10.1016/j.ribaf.2017.07.104

Liu, L.X., Liu, S. and Sathye, M. (2021). Predicting bank failures: a synthesis of literature and directions for future research. Journal of Risk and Financial Management, 14(10), 474. https://doi.org/10.3390/jrfm14100474

Mabkhot, H. and Al-Wesabi, H.A.H. (2022). Banks’ financial stability and macroeconomic key factors in GCC countries. Sustainability, 14(23), 15999. https://doi.org/10.3390/su142315999

Moudud-Ul-Huq, S., Biswas, T., Abdul Halim, M., Mateev, M., Yousaf, I. and Abedin, M.Z. (2022). The effects of bank competition, financial stability and ownership structure: evidence from the Middle East and North African (MENA) countries. International Journal of Islamic and Middle Eastern Finance and Management, 15(4), 717–738. https://doi.org/10.1108/IMEFM-05-2020-0214

Petropoulos, A., Siakoulis, V., Stavroulakis, E. and Vlachogiannakis, N.E. (2020). Predicting bank insolvencies using machine learning techniques. International Journal of Forecasting, 36(3), 1092–1113. https://doi.org/10.1016/j.ijforecast.2019.11.005

Shahriar, A., Mehzabin, S., Ahmed, Z., Döngül, E.S. and Azad, M.A.K. (2023). Bank stability, performance and efficiency: an experience from West Asian countries. IIM Ranchi journal of management studies, 2(1), 31–47. https://doi.org/10.1108/IRJMS-02-2022-0017

Shehata, K. and Ali, L. (2025). January. Early Prediction of Bank Performance Using Machine Learning Algorithm. In International Conference on Mathematical Modeling and Computational Science (pp. 27-40). Cham: Springer Nature Switzerland. https://doi.org/10.1007/978-3-031-91005-0_4

Shrivastava, S., Jeyanthi, P.M. and Singh, S. (2020). Failure prediction of Indian Banks using SMOTE, Lasso regression, bagging and boosting. Cogent Economics & Finance, 8(1), 1729569. https://doi.org/10.1080/23322039.2020.1729569

Tanaka, K., Kinkyo, T. and Hamori, S. (2016). Random forests-based early warning system for bank failures. Economics Letters, 148, 118–121. https://doi.org/10.1016/j.econlet.2016.09.024

Trung, N.D., Quynh, N.T.N. and Luan, L.D. (2021, January). Determinants of bank stability: Evidence from Vietnam. A Bayesian approach. In International econometric conference of Vietnam (pp. 609-624). Cham: Springer International Publishing. https://doi.org/10.1007/978-3-030-77094-5_46

Yakubu, I.N. and Bunyaminu, A. (2023). Regulatory capital requirement and bank stability in Sub-Saharan Africa. Journal of Sustainable Finance & Investment, 13(1), 450–462. https://doi.org/10.1080/20430795.2021.1961558

Yitayaw, M.K., Mogess, Y.K., Feyisa, H.L., Mamo, W.B., and Abdulahi, S.M. (2023). Determinants of bank stability in Ethiopia: A two-step system GMM estimation. Cogent Economics & Finance, 11(1), 2161771. https://doi.org/10.1080/23322039.2022.2161771