Organizations and Markets in Emerging Economies ISSN 2029-4581 eISSN 2345-0037

2026, vol. 17, no. 1(34), pp. 81–94 DOI: https://doi.org/10.15388/omee.2026.17.4

Exchange Rate Unification in Nigeria: Volatility Dynamics and Short-Term Forecasts

Idowu Ayodeji

Obafemi Awolowo University, Nigeria

ioayodeji@oauife.edu.ng, idowu.sayo@yahoo.com

Abstract. Nearly two years after Nigeria’s exchange rate unification policy was introduced, questions remain about its effectiveness. This study uses the Exponential GARCH model to examine: (1) the impact of the policy on exchange rate returns and volatility, (2) whether it has achieved its intended goal of long-term stabilization, and (3) what forecasts reveal about future exchange rate dynamics. Results indicate that while the policy did not significantly affect mean returns, it led to a significant increase in volatility (4.3757, p < 0.05). However, volatility began to subside from Q4 2024, suggesting a market adjustment phase. Forecasts show a continued decline in volatility through mid-2025, implying the policy may be on track toward achieving its long-term goals. The study recommends ongoing monitoring of exchange rate behaviour, complementary short-term measures to manage short-term volatility while allowing the unification policy to mature further, and improved policy communication with market participants to support sustained stability.

Keywords: exchange rate unification, Nigeria, volatility persistence, market stability, exponential GARCH Model, Naira/USD Exchange Rate, emerging markets

Received: 5/5/2025. Accepted: 12/3/2026

Copyright © 2026 Idowu Ayodeji . Published by Vilnius University Press. This is an Open Access article distributed under the terms of the Creative Commons Attribution Licence, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

1. Introduction

Exchange rate volatility remains a pressing concern in emerging economies, where fluctuations can significantly affect macroeconomic stability, trade balances, and foreign investment. Central banks often intervene, either through direct market operations or policy announcements, to stabilize exchange rates, but the effectiveness of such interventions remains contested (Neely, 2005). In 2023, the Central Bank of Nigeria (CBN) introduced an exchange rate unification policy to address persistent challenges in the country’s foreign exchange (FX) market. The policy consolidated multiple official and investor exchange rates into a single, market-determined rate, aiming to boost FX supply, strengthen customer confidence, curb speculative behaviour, and ultimately stabilize the market (Olaniwun Ajayi LP, 2023). It aligned with international best practices, including recommendations from the International Monetary Fund (IMF) in 2021. While some immediate effects were anticipated, the more substantial benefits, such as long-term stabilization, are expected to materialize over time, with any initial disruptions gradually subsiding (Ozili, 2024).

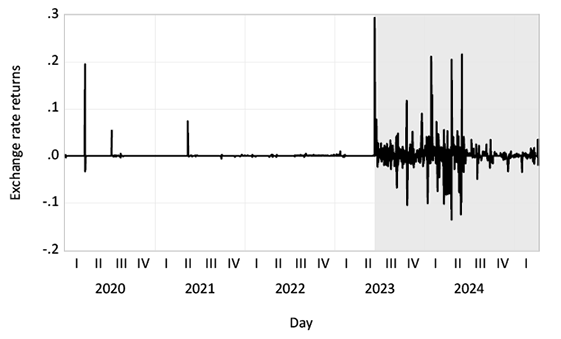

However, nearly two years after the policy was introduced, important questions remain regarding its effectiveness. A central concern is whether the intervention has had the desired impact on the returns and volatility of the exchange rate, and what the future trajectory of exchange rate behaviour may be under prevailing conditions. As shown in Figure 1, the exchange rate exhibited relative stability from the second quarter of 2021 until the implementation of the unification policy (shaded area), after which a noticeable spike in volatility occurred. Although the policy was intended to promote long-term stabilization, empirical validation of its effectiveness remains limited. To the best of our knowledge, no study has yet rigorously assessed whether the policy has achieved its longer-term stabilization objectives. This study is the first to explicitly investigate volatility dynamics, long-term stabilization, and short-term forecasts in the context of Nigeria’s 2023 exchange rate unification policy, examining both the returns and volatility of the exchange rate. It therefore offers insights into policy effectiveness and market behaviour in a context of economic fragility.

Figure 1

Daily Exchange Rate Returns (NGN/USD)

Note. The graph includes data from January 1, 2020 to April 8, 2025. Based on the author’s analysis.

This study seeks to answer three critical questions: First, what effect has the intervention had on the returns and volatility of exchange rates? Second, has the policy successfully reduced exchange rate fluctuations in the long run? Third, what do the model’s forecasts suggest about the future trajectory of exchange rate volatility? Addressing these questions is particularly important for countries with volatile economies like Nigeria, where exchange rate policies have significant implications.

Although several studies have investigated exchange rate unification in other countries—such as Ghana (Sanusi, 2010), Iran (Parvin & Banouei, 2020), and Cuba (De la Torre & Ize, 2013)—their focus has largely been on policy implementation, macroeconomic adjustment, or welfare outcomes rather than on volatility dynamics or long-term stabilization. Nigeria’s case is distinctive not only in focus but also in context: the unification occurred during a period of pronounced economic fragility, marked by high inflation, large fiscal and trade deficits, low foreign exchange reserves, and concurrent structural reforms such as fuel subsidy removal. These macroeconomic pressures likely heightened short-term exchange rate instability and complicated the transmission of the policy, making Nigeria a uniquely instructive case for examining the behaviour and persistence of volatility following unification.

Standard macroeconomic models suggest that efficient markets immediately incorporate all relevant information, making the effects of interventions both instant and permanent (Neely, 2005). Empirical studies using high-frequency GARCH models typically find that interventions have short-lived effects on exchange rate returns and volatility, lasting only a few days (Baillie & Osterberg, 1997; Dominguez, 2003). Similar conclusions have been drawn for the impact of major macroeconomic news (e.g., Andersen et al, 2003; Ehrmann & Fratzscher, 2005), highlighting the challenge of detecting persistent effects amid the constant flow of market-relevant information. However, microstructure-based models (e.g., Evans & Lyons, 2005) suggest that markets incorporate information more gradually, with macroeconomic news affecting exchange rates dynamically over several days.

Most prior studies in Nigeria have concentrated on the effects of exchange rate volatility on trade and investment flows, with limited focus on volatility shifts induced by specific policy interventions or the direct role of central bank actions. Olowe (2011) is a notable exception, applying GARCH-family models to examine the effects of banking reforms and the global financial crisis on Nigeria’s foreign exchange market. Nonetheless, policy-driven episodes, particularly those involving targeted interventions, remain underexplored. Ayodeji (2025) offers important initial insights by documenting short-term fluctuations in exchange rate volatility following the unification policy, highlighting immediate market reactions. This study extends Ayodeji’s work by moving beyond short-term dynamics to assess the long-term implications of the policy on exchange rate stability. Additionally, this study explores what the model’s forecasts suggest about the future trajectory of exchange rate behaviour. By examining a post-policy window of two years, this study provides a grounded assessment of whether such long-term stabilization effects have begun to materialize.

This study analyzes daily exchange rate data for the Nigerian Naira (NGN) against the US Dollar (USD) from January 1, 2020, to April 8, 2025, using the Exponential GARCH (EGARCH) model. The next section outlines the rationale for adopting this approach. By offering a comprehensive econometric assessment of exchange rate dynamics before and after the policy shift, the study highlights the persistence of volatility and its alignment with key market events. The findings hold practical value for policymakers, enabling more precise intervention strategies and improved forecasting of long-term outcomes of exchange rate reforms. For investors, the analysis provides insights into the shifting risk profile of the Nigerian currency, fostering more informed decision-making in an increasingly volatile environment. Researchers, in turn, will benefit from a deeper understanding of the effects of policy-induced shocks on exchange rate behaviour in emerging markets. Ultimately, the study offers lessons not only for Nigeria but also for other emerging economies navigating similar reform trajectories.

2. Method

The analysis uses daily exchange rate data for the Nigerian Naira (NGN) against the US Dollar (USD) from January 1, 2020, to April 8, 2025. This period captures exchange rate dynamics before, during, and after the policy announcement, providing a comprehensive view of volatility surrounding the intervention. The analysis focuses on the USD/NGN exchange rate because the US dollar is Nigeria’s primary trading and reserve currency, accounting for the majority of external transactions, and because it is the standard benchmark used in most empirical studies on exchange rate volatility in Nigeria (Olowe, 2011; Ayodeji, 2025; Sikiru & Salisu, 2025). The data were sourced from the Central Bank of Nigeria.

To model exchange rate volatility, this study employs the Exponential Generalized Autoregressive Conditional Heteroskedasticity (EGARCH) model. This approach facilitates the examination of both the returns and volatility of exchange rates over time, with a particular focus on asymmetries—such as the tendency for markets to respond more strongly to negative shocks than to positive ones. Such asymmetry is especially pertinent in evaluating the potential uneven effects of the exchange rate unification policy. Previous studies, including Bala and Asemota (2013) and Ayodeji (2015), have utilized EGARCH models to investigate the dynamics of exchange rate volatility in Nigeria and Kenya, respectively, yielding insights into the persistence and asymmetric nature of volatility in response to external shocks.

In line with Olowe (2011), a dummy variable D is introduced in Equation (1) to capture the impact of the policy intervention. This variable takes the value of 1 from June 14, 2023, the exact date of announcement, and in the post-policy period; and 0 otherwise:

(1)

(1)

The dummy is incorporated into both the mean and variance equations of the EGARCH model to assess shifts in exchange rate returns and volatility associated with the policy.

The model specifications are as follows:

1. Mean Equation is expressed as:

(2)

(2)

(3)

(3)

where

(4)

(4)

denotes the logarithmic change in exchange rates. x is the nominal exchange rates, c is the constant term, Dt is the policy intervention dummy variable, and θ measures its effect on exchange rate returns. εt represents the residuals, ht represents the conditional variance of the exchange rate returns at time t, and zt ~ N(0,1). φ measures the effect of the past exchange rate returns on the current exchange rate returns.

2. Variance Equation is represented as:

(5)

(5)

where ht represents the conditional variance of the exchange rate returns at time t, ω is a constant term, α measures the effect of past shocks on current volatility, γ measures the asymmetric effect of ε on the conditional variance ht , β captures the persistence of volatility, Dt is included to capture the effect of the policy on exchange rate volatility, and δ measures the effect of Dt .

Unlike the standard GARCH model, the EGARCH framework is less restrictive, requiring only that  for covariance stationarity of Equation (5) to be satisfied. A key advantage of the EGARCH model, as noted by Nelson (1991), is that it specifies the conditional variance in logarithmic form, thereby guaranteeing nonnegativity without imposing nonnegativity constraints on the parameters ω, α, β, γ. The system (2) - (5) is estimated using Maximum Likelihood Estimation. Diagnostic check is conducted to assess model adequacy, including tests for residual autocorrelation and heteroscedasticity.

for covariance stationarity of Equation (5) to be satisfied. A key advantage of the EGARCH model, as noted by Nelson (1991), is that it specifies the conditional variance in logarithmic form, thereby guaranteeing nonnegativity without imposing nonnegativity constraints on the parameters ω, α, β, γ. The system (2) - (5) is estimated using Maximum Likelihood Estimation. Diagnostic check is conducted to assess model adequacy, including tests for residual autocorrelation and heteroscedasticity.

2.1 Justification and Limitations

When studying the effects of interventions such as exchange rate unifications, two key methodological decisions are critical: the choice of data frequency and the modeling approach. Daily data are used in this study because they capture rapid market reactions to policy changes that monthly or quarterly data may miss. Daily observations allow for the analysis of both immediate shifts in exchange rate returns and volatility dynamics, including volatility clustering, which is essential for understanding the impact of the unification. Lower-frequency data tend to smooth over these short-term fluctuations, potentially obscuring critical information about market responses (Kim, 2003).

The choice of the EGARCH model complements the use of daily data. EGARCH is specifically designed to model volatility and can capture asymmetries in market responses to positive and negative shocks, as well as the persistence of volatility over time. Unlike event study methodologies, which focus on short, pre-defined windows around interventions, EGARCH allows for a continuous, dynamic assessment of both immediate and long-term effects, and provides forecasting capabilities. By incorporating the policy intervention directly into both the mean and variance equations, the model enables a detailed evaluation of whether the unification policy has reduced volatility and contributed to exchange rate stabilization.

3. Results

The preliminary descriptive statistics and diagnostic tests presented in Table 1 provide insights into the distributional and dynamic properties of the exchange rate return series (rt ). With 1,373 daily observations, the mean return is positive but very small (0.001182), suggesting marginal average daily appreciation over the sample period. The median return is zero, indicating a fairly symmetric distribution around the centre, but the range between the maximum (0.293655) and minimum (-0.135614) values reflects significant daily fluctuations, which is also captured by the relatively high standard deviation (0.019691). The Augmented Dickey-Fuller (ADF) test statistic of -24.94470, which is highly significant at the 5% level, confirms that the return series is stationary and suitable for further modeling in a volatility framework.

Tests of autocorrelation and heteroscedasticity further justify the use of an EGARCH model. The Ljung-Box Q statistics at lags 1, 5, and 10 are all statistically significant, indicating the presence of autocorrelation in the return series. More critically, the Ljung-Box Q² statistics for squared residuals at the same lags, along with the significant ARCH LM statistics, confirm the presence of conditional heteroscedasticity—a key characteristic of financial time series (Ayodeji, 2025). This implies that exchange rate volatility is not constant over time but forms clusters, with periods of high volatility followed by calm periods. These results validate the choice of a volatility model such as EGARCH, which can account for such time-varying volatility as well as asymmetries in market responses to shocks.

Table 1

Summary Statistics of Exchange Rate Returns (NGN/USD)

|

Statistics |

Value |

|---|---|

|

Observations |

1373 |

|

Mean |

0.001182 |

|

Median |

0.000000 |

|

Maximum |

0.293655 |

|

Minimum |

-0.135614 |

|

Std. Dev. |

0.019691 |

|

Unit Root Test |

|

|

Augmented Dickey-Fuller |

-24.94470* |

|

Tests of Autocorrelation |

|

|

Ljung-Box Q(1) |

13.412* |

|

Ljung-Box Q(5) |

38.947* |

|

Ljung-Box Q(10) |

48.141* |

|

Tests of Heteroscedasticity |

|

|

Ljung-Box Q2 (1) |

13.621* |

|

Ljung-Box Q2 (5) |

30.754* |

|

Ljung-Box Q2 (10) |

32.801* |

|

ARCH LM(1) |

13.69701* |

|

ARCH LM(5) |

5.350316* |

|

ARCH LM(10) |

2.744053* |

Note. *Significant at 0.05.

3.1 Main Analysis

The results from the EGARCH model presented in Table 2 provide insights into the dynamics of exchange rate returns and the impact of the CBN’s intervention, particularly in the context of the recent exchange rate unification policy. These findings directly address the two central research questions of this study: (1) What effect has the intervention had on the returns and volatility of exchange rates? and (2) Has the policy successfully achieved its intended goal of reducing volatility and stabilizing the exchange rate in the long run?

In the mean equation, none of the autoregressive terms are statistically significant except for the second lag, suggesting limited persistence in daily exchange rate returns. The policy intervention variable (θ) in the mean equation is positive (0.000959) but statistically insignificant, indicating that the intervention did not have effect on the average returns of exchange rate returns. This suggests that the policy did not cause a significant shift in the returns of the exchange rate itself.

In contrast, the variance equation reveals a different picture, with clear evidence that the unification policy significantly impacted exchange rate volatility. The large and statistically significant positive coefficient on the policy dummy in the variance equation (δ = 0.3757, p < 0.05) suggests that the 2023 unification policy led to a statistically significant increase in exchange rate volatility. Moreover, the persistence parameter (β = -0.6927, p < 0.05) shows that this increase in volatility moderately persisted over time, indicating that while the policy induced a notable volatility response, its effects on market uncertainty tend to decay over time rather than produce a prolonged destabilization of the exchange rate. In other words, CBN’s unification policy did not result in a permanent or overly persistent volatility spike. In addition, the negative and significant leverage term (γ = -0.1803, p < 0.05) highlights the asymmetric nature of the volatility, where negative shocks (such as exchange rate depreciation) tend to have a larger impact on volatility than positive shocks. This finding underscores the market’s heightened uncertainty following the policy shift, a response often observed during major economic policy changes.

Table 2

EGARCH Results

|

Parameter |

Coefficient |

|---|---|

|

Mean |

|

|

C |

0.000591 (0.000501) |

|

φ1 |

-0.015233 (0.024954) |

|

φ2 |

0.058609 (0.014379)* |

|

φ3 |

0.017753 (0.027434) |

|

φ4 |

-0.012597 (0.031697) |

|

φ |

0.000959 (0.001295) |

|

Variance |

|

|

ω |

-16.70408 (0.234051)* |

|

α |

0.222259 (0.019921)* |

|

γ |

-0.180256 (0.017854)* |

|

β |

-0.692706 (0.023547)* |

|

δ |

4.375693 (0.078986)* |

|

Diagnostics: Tests of Autocorrelation |

|

|

Ljung-Box Q(1) |

3.3514 |

|

Ljung-Box Q(5) |

5.2065 |

|

Ljung-Box Q(10) |

6.9655 |

|

Diagnostics: Tests of Heteroscedasticity |

|

|

Ljung-Box Q2 (1) |

0.0776 |

|

Ljung-Box Q2 (5) |

0.1206 |

|

Ljung-Box Q2 (10) |

0.1376 |

|

ARCH LM(1) |

0.077295 |

|

ARCH LM(5) |

0.023735 |

|

ARCH LM(10) |

0.013365 |

Note. Data for the period 1/01/2020 – 4/08/2025. Standard error in parentheses. *Significant at 5%.

The coefficient ω = -16.704 is negative, suggesting lower volatility when there are no shocks to the system. In addition, the positive and statistically significant parameter (α = 0.222) indicates that larger shocks increase volatility.

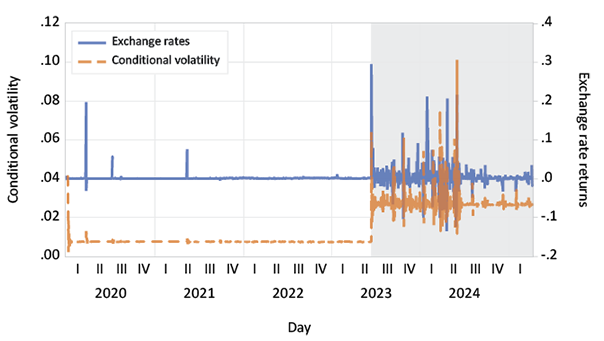

Figure 2 clearly shows that the period following the policy announcement (shaded in grey) saw significant heightened fluctuations with very high persistence within the period of announcement and the third quarter of 2024, followed by a period of relative stability.

Post-estimation diagnostics in Table 2 support the model’s adequacy, as the Ljung-Box Q and Q² statistics and ARCH LM tests show no remaining autocorrelation or ARCH effects, indicating that the model effectively captures the volatility dynamics in the data. These findings suggest that although the unification policy aimed at stabilizing the exchange rate, it may have initially triggered heightened market uncertainty and volatility.

Figure 2

Conditional Volatility Chart Superimposed with Exchange Rate Returns

Note. The chart covers the period January 1, 2020–April 8, 2025. Based on the author’s analysis.

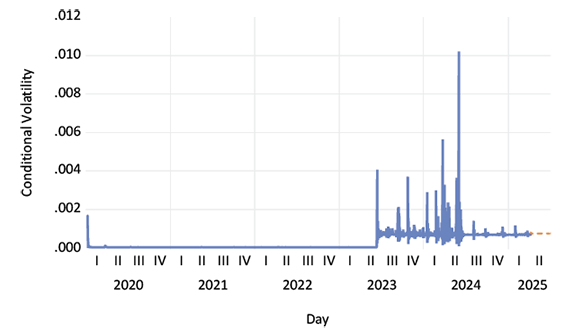

The conditional volatility forecast, indicated by dotted lines in Figure 3, shows a continuation of the declining or stabilized trend that began after the high-volatility spikes of 2023 and early 2024. This visual pattern suggests that the initial turbulence following the exchange rate unification policy is giving way to a more stable market environment. In particular, the absence of renewed volatility spikes in the forecast horizon, extending from April to June 2025, implies that the market is settling and that the policy may be on track toward achieving its long-term stabilization objectives.

Figure 3

Conditional Volatility Chart

Note. The chart includes the period January 1, 2020–June 14, 2025. Based on the author’s analysis.

4. Discussion

The EGARCH model yields several key insights into the effects of Nigeria’s 2023 exchange rate unification policy. In the mean equation, the policy intervention variable is positive but not statistically significant, suggesting that the unification policy did not induce a systematic change in the exchange rate returns, on the average. In essence, the policy did not trigger an immediate or sustained shift in the exchange rate returns. This finding is consistent with Olowe (2011), who similarly reported that major financial events, such as the 2004 increase in bank capital requirements, insurance sector reforms, and the global financial crisis, had no significant impact on the mean returns of the Nigerian exchange rate. The lack of effect on the mean may reflect market expectations already priced in prior to the announcement, as well as constraints imposed by Nigeria’s macroeconomic environment, including high inflation, fiscal and trade imbalances, and low foreign exchange reserves, all of which are well documented in recent studies (IMF, 2023; Ozili, 2024; Sikiru & Salisu, 2025).

The investigation of the effect of the announcement of Nigeria’s exchange rate unification policy on market volatility reveals interesting dynamics that challenge conventional expectations of immediate and permanent market adjustments. The EGARCH model shows that the announcement of the unification policy induced a temporary spike followed by a swift return to equilibrium. However, the results indicate a significant moderate persistence in volatility, with shocks continuing to affect market behaviour over a period longer than was observed in previous studies such as Baillie and Osterberg (1997) and Dominguez (2003).

The empirical findings from this study align more closely with microstructure-based models (Evans & Lyons, 2005), which suggest that markets process macroeconomic news gradually, absorbing its full implications over days or even weeks, depending on the complexity and significance of the policy intervention. This gradual adjustment suggests that the Nigerian foreign exchange market is not fully efficient, as policy-relevant information is absorbed over time rather than instantaneously. This finding is consistent with recent studies, such as Sikiru and Salisu (2025), which documents inefficiencies in the Nigerian FX market. However, it is in contrast with standard macroeconomic models, such as those discussed by Neely (2005), which assume efficient markets that immediately incorporate policy-relevant information, producing instant and permanent effects on exchange rates and volatility.

Notably, our finding here extends the result of Ayodeji (2025), which found β = 0.966 in Nigerian exchange rate data spanning January 1, 2020–August 4, 2024. Using data through April 8, 2025, we observe that fluctuations have begun to subside from the fourth quarter of 2024, suggesting the market may be finding equilibrium after the initial shock of the policy changes. This indicates that, although the policy triggered a significant volatility response, its effects on market uncertainty appear to diminish over time rather than cause prolonged destabilization. The forecast conditional volatility further supports this trend, showing a continued decline and the absence of renewed spikes through mid-2025, implying that the policy may be on track to achieving its long-term stabilization objectives. This pattern reflects a typical adjustment phase, where markets gradually return to a more stable state after major disruptions. Volatility may spike initially, but markets tend to stabilize over time as new policies are absorbed into expectations and strategies.

The literature on central bank interventions, particularly in developing economies, highlights the complex relationship between policy measures and exchange rate volatility. Studies such as Benita and Lauterbach (2007) have shown that central bank interventions, while aimed at stabilizing the currency, can sometimes exacerbate volatility. This is consistent with the findings in Nigeria, where the unification policy has resulted in significant volatility spikes, particularly in the wake of policy announcements and the broader economic uncertainty surrounding fuel subsidy removal and inflation. The negative coefficient γ in the EGARCH model further supports this, indicating that negative shocks have a disproportionately larger impact on volatility than positive shocks, a pattern commonly seen in other African markets (Bouoiyour & Selmi, 2002; Okyere et al., 2013; Ayodeji, 2015). This asymmetry suggests that Nigeria’s exchange rate market is highly sensitive to bad news, amplifying the market’s reaction to policy shifts.

The results also reinforce the idea that, in Nigeria, central bank interventions often lead to prolonged market reactions, reflecting the broader dynamics in developing economies. This sustained volatility could be due to a lack of sufficient stabilizing measures accompanying the exchange rate policy, which mirrors concerns raised by previous studies (Benita & Lauterbach, 2007). While the unification of exchange rates may be necessary for long-term economic stability, the findings suggest that the policy has inadvertently heightened market instability in the short run. This underscores the importance of complementary measures—such as effective fiscal policies, clear communication, and gradual implementation—to help ease the transition and reduce the negative consequences of such policy shifts on the exchange rate market. The persistent volatility observed here suggests that Nigeria may need to adopt a more comprehensive approach to managing market expectations, particularly in the wake of future policy interventions.

5. Conclusion

This study makes contribution to the existing literature by investigating the impact of the Central Bank of Nigeria’s exchange rate unification policy on exchange rate volatility, particularly in the aftermath of the policy announcement. Previous research has generally found that central bank interventions influence exchange rate volatility in the short term, with market reactions typically subsiding quickly. However, while the unification policy induced a significant volatility response, its effects on market uncertainty appear to diminish over time rather than causing a prolonged destabilization of the exchange rate. In addition, the result shows that the policy had no significant effect on the returns of the exchange rate. The findings suggest that the policy is beginning to achieve its intended long-term stabilization objectives, as evidenced by the market’s gradual return to equilibrium from the fourth quarter of 2024. Furthermore, the forecast conditional volatility reinforces this trend, showing a continued decline and the absence of renewed volatility spikes through mid-2025.

Policy Implications

The findings of this study have several actionable implications for policy design. First, the Central Bank of Nigeria (CBN) should consider monitoring exchange rate volatility more closely post-policy intervention, particularly in the initial quarters following such reforms. Given that the policy-induced volatility appears to subside over time, the CBN may explore additional targeted interventions to maintain market confidence and ensure that the stabilization process continues smoothly. For example, providing market guidance or implementing gradual adjustments could help manage market expectations and prevent potential shocks.

Second, as the market shows signs of finding equilibrium, the CBN should consider formalizing a post-policy evaluation framework to assess the long-term effectiveness of the exchange rate unification in stabilizing the Nigerian currency. This would provide both the central bank and market participants with a clear understanding of the policy’s trajectory and foster a more predictable economic environment.

Lastly, for emerging markets with similar exchange rate reform plans, this study suggests that while immediate effects may be volatile, long-term stabilization can be achieved through gradual market adjustments and careful monitoring of policy outcomes over time.

Study Limitations

While this study provides insights into the impact of Nigeria’s exchange rate unification policy, there are several limitations. The analysis focuses solely on the effects of the Central Bank of Nigeria’s exchange rate unification policy, without considering other key macroeconomic variables, such as interest rate differentials, which may have interacted with the policy and influenced exchange rate volatility. These variables are available only on a monthly, quarterly, or annual basis, limiting the ability to capture short-term fluctuations. This limitation may constrain the study’s ability to fully isolate and understand the policy’s impact in a broader economic context. However, the methodological decision to make use of high-frequency data was made to balance the trade-off that key macroeconomic factors are typically low-frequency data, potentially missing finer, rapid market reactions critical for examining immediate policy impacts. Thus, while high-frequency data may omit some key macroeconomic factors, it is essential for understanding quick shifts in exchange rate behaviour following policy changes. The results of the study should be interpreted with this in mind. Additionally, the analysis covers a post-policy period of two years, which serves as a solid starting point for evaluating the long-term effects of the policy. Future research could build on this foundation to observe whether the observed stabilization trends persist beyond this initial time frame.

Funding statement

Interested readers are referred to Central Bank of Nigeria (2023), Olaniwun Ajayi LP (2023) and Ozili (2024) for a more detailed discussion of the policy’s design, objectives, and implementation.

References

Andersen, T. G., Bollerslev, T., Diebold, F. X., & Vega, C. (2003). Micro Effects of Macro Announcements: Real-Time Price Discovery in Foreign Exchange, The American Economic Review, 39(1), 38–62.

Ayodeji, S. (2015). Modeling Asymmetric Effect in African Currency Markets: Evidence from Kenya. Journal of Statistical and Econometric Methods, 4(3), 17–46.

Ayodeji, I. O. (2025). Evaluating the Effect of Exchange Rate Unification on Exchange Rate Volatility in Emerging Markets: A Case Study of Nigeria. Sri Lankan Journal of Applied Statistics, 26 (1). https://doi.org/10.4038/sljas.v26i1.8150

Bala, D. A., & Asemota, J. O. (2013). Exchange-rates volatility in Nigeria: Application of GARCH models with exogenous break. CBN Journal of Applied Statistics, 4(1), 89–116. The Central Bank of Nigeria. https://hdl.handle.net/10419/142075

Baillie, R. T., & Osterberg, W. P. (1997). Why do Central Banks Intervene?, Journal of International Money and Finance, 16, 909–919.

Beine, M., Lahaye, J., Laurent, S., Neely, C. J., & Palm, F. C. (2007). Central bank intervention and exchange rate volatility: Its continuous and jump components. International Journal of Finance and Economics, 12(2), 201–223.

Benita, G., & Lauterbach, B. (2007). Policy Factors and Exchange rate Volatility: Panel Data versus a Specific Country Analysis. International Research Journal of Finance and Economics, 7(7), 7–23.

Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31(3), 307–327.

Bouoiyour, J., & Selmi, R. (2002). Modeling exchange volatility in Egypt using GARCH models, http://mpra.ub.uni-muenchen.de/49131/.

Central Bank of Nigeria. (2023, June 14). Operational changes to the foreign exchange market. https://perchstoneandgraeys.com/wp-content/uploads/2024/03/Review-of-the-Central-Bank-of-Nigeria.pdf

De la Torre, A., & Ize, A. (2013). Exchange rate unification: The Cuban case. Cuban Economic Change in Comparative Perspective Paper Series-Brookings.

Dominguez, K. (2003). The Market Microstructure of Central Bank Intervention. Journal of International Economics, 59(1), 25–45.

Ehrmann, M., & Fratzscher, M. (2005) Exchange Rates and Fundamentals: New Evidence from Real-Time Data, forthcoming in Journal of International Money and Finance, 24(2), 317–341.

Engle, R. F. (1982). Autoregressive conditional heteroscedasticity with estimates of U.K. inflation. Econometrica, 50(4), 987–1007.

Evans, M. D., & Lyons, R. K. (2005) Do Currency Markets Absorb News Quickly? Journal of International Money and Finance, 24(2), 197–219.

Fatum, R., & Hutchison, M. (2003) Is Sterilised Foreign Exchange Intervention Effective After All? An Event Study Approach. Economic Journal, 113(487), 390–411.

International Monetary Fund, African Department. (2023). Nigeria: Selected issues (IMF Country Report No. 23/094). Washington, DC: International Monetary Fund.

Kim, S. (2003). Monetary Policy, Foreign Exchange Intervention, and the Exchange Rate in a Unifying Framework. Journal of International Economics, 60(2), 355–86.

Neely, C. J. (2005). An Analysis of Recent Studies of the Effect of Foreign Exchange Intervention. Federal Reserve Bank of St. Louis Review, 87(6), 685–717.

Nelson, D. B. (1991). Conditional heteroskedasticity in asset returns: A new approach. Econometrica, 59(2), 347–370.

Okyere, E., Mensah, A., Antwi, O., & Kumi, P. (2013). Modeling the Volatility of GHC_USD Exchange Rate Using GARCH Model, European Journal of Business and Management, 5(32), 140–147.

Olaniwun Ajayi LP. (2023). Foreign exchange rate convergence in Nigeria. https://www.olaniwunajayi.net

Olowe, R. (2011). Exchange Rate Volatility, Global Financial Crisis and the Day-of-the-Week Effect, KCA Journal of Business Management, 3(3), 138–149.

Ozili, P. K. (2024). Exchange rate unification in Nigeria: Benefits and implications. Munich Personal RePEc Archive (MPRA Paper No. 120441). https://mpra.ub.uni-muenchen.de/120441/

Parvin, S., & Banouei, A. A. (2020). The Effect of Unification of Exchange Rate on Poverty in Iran Using the Computable General Equilibrium Model (CGE). The Economic Research, 20(1), 184–153.

Sanusi, A. R. (2010). Successful Exchange Rate Unification in a High Inflation Environment: Lessons from the Ghanaian Economic Reforms of 1983-2006. Abuja Journal of Administration and Management, 7(2).

Sikiru, A. A., & Salisu, A. A. (2025, January 31). Exchange rate variability in Nigeria: Drivers and remedial monetary policy (MPRA Paper No. 123526). University Library of Munich.