Organizations and Markets in Emerging Economies ISSN 2029-4581 eISSN 2345-0037

2026, vol. 17, no. 1(34), pp. 6–32 DOI: https://doi.org/10.15388/omee.2026.17.1

The Nexus of Economic Policy Uncertainty, Cash Holdings, and Investment: A Systematic Literature Review from an Agency Theory Perspective

Nungki Pradita (corresponding author)

Gadjah Mada University, Indonesia

nungkipradita@mail.ugm.ac.id

Eduardus Tandelilin

Gadjah Mada Unversity, Indonesia

e_tandelilin@ugm.ac.id

Bowo Setiyono

Gadjah Mada University, Indonesia

bowo@ugm.ac.id

Abstract. This systematic literature review (SLR), integrated with bibliometric analysis, provides a comprehensive investigation into the impact of economic policy uncertainty (EPU) on corporate strategic decisions. While previous studies often discuss EPU impacts broadly, this review specifically synthesizes the interplay between EPU, corporate cash holdings, and investment efficiency through the lens of agency theory. Using the PRISMA framework, a total of 105 high-quality articles published in Scopus-indexed journals (2018–2025) were analyzed. The bibliometric findings reveal that 66.7% of the literature is published in Q1 journals, with Elsevier as the dominant publisher. However, a significant research gap exists regarding the underrepresentation of emerging economies, particularly in developing markets where policy uncertainty effects remain understudied. The qualitative synthesis reveals that EPU significantly influences precautionary cash holdings and suppresses investment efficiency, with agency conflicts acting as a critical moderating mechanism. This study contributes by proposing an integrated conceptual framework that links policy uncertainty to managerial behavior, providing a foundation for future research to explore mitigation strategies in diverse institutional contexts, particularly in developing markets.

Keywords: economic policy uncertainty, agency theory, cash holding, corporate investment

Received: 31/5/2025. Accepted: 14/4/2026

Copyright © 2026 Nungki Pradita, Eduardus Tandelilin, Bowo Setiyono. Published by Vilnius University Press. This is an Open Access article distributed under the terms of the Creative Commons Attribution Licence, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

1. Introduction

Economic policy uncertainty (EPU) refers to the level of ambiguity and uncertainity surrounding government policies and regulations, specifically encompassing changes in monetary policy, fiscal policy, regulatory framewoorks, and trade agreements and those who manage them. More precisely, EPU focusses on the ambiguity of government actions (monetary, fiscal, regulatory) that directly create information asymmetries between principals (shareholders) and agents (managers). This distinction is critical because it highlights how policy uncertainty exacerbates principal agent conflicts by increasing information gaps between those who own companies and those who manage them. Economic policy uncertainty has become an interesting topic among researchers due to its significant and broad adverse effects on the economy. This uncertainty impacts financial markets at both micro and macro levels, affecting stock markets, corporate behavior, and risk management (Al-Thaqeb & Algharabali, 2019). Regarding corporate behavior, economic policy uncertainty significantly affects corporate cash holdings and investment decisions. Companies tend to hold more cash during high EPU periods due to precautionary motives and delayed investments (Trinh et al., 2022, Guizani et al., 2023; Phan et al., 2019). One aspect of this impact is its influence on corporate cash holdings in China (Legesse et al., 2023; Lin et al., 2023; Makosa et al., 2021; Zeng et al., 2020) and the United States (Cheng et al., 2018; Duong et al., 2020; Guizani et al., 2023; Hankins et al., 2020; Heeney et al., 2023; M. Nguyen & Nguyen, 2020; Seo & Mun, 2022; Vuong et al., 2023). For example, companies in China and the United States show that EPU increases financing constraints and encourages companies to delay investment projects, leading to the accumulation of cash for future investments (Ahsan & Qureshi, 2021).

Cash storage is an important corporate policy that helps companies ensure financial stability and flexibility in uncertain times (Javadi et al., 2021). On the one hand, economic policy uncertainty can lead companies to increase their cash holdings as a precautionary measure. It can also create a sense of urgency for companies to invest their excess cash to mitigate potential risks and seize emerging opportunities. Economic policy uncertainty can have a dual impact on corporate cash holdings and investment decisions (Suet al., 2020). When faced with economic policy uncertainty, companies tend to increase their cash holdings as a precautionary measure (Heeney et al., 2023; Javadi et al., 2021; Zeng et al., 2020). This is because cash holdings serve as a safety net during high uncertainty periods (Javadi et al., 2021). High cash holdings allow companies to face potential financial challenges or seize new opportunities that may arise (Chada, 2023a). Moreover, economic policy uncertainty can also affect investor sentiment and increase concerns about detrimental managerial actions. As a result, companies may increase their cash holdings to reassure investors and demonstrate financial stability (Legesse et al., 2023; Phan et al., 2019).

Some companies tend not to increase cash holdings during high economic policy uncertainty due to agency conflicts (Feng et al., 2022; Vuong et al., 2023). It is assumed that reducing cash holdings during high economic policy uncertainty can mitigate agency problems (Attig et al., 2021; Javadi et al., 2021). In other situations, companies may sanction management for holding excess cash (Benkraiem et al., 2023), believing that the risks during high economic policy uncertainty are lower than the opportunities if investments are made (Cui et al., 2022). Thus, it is perceived that holding high levels of cash during periods of high economic policy uncertainty can lead to agency problems and missed investment opportunities.

According to agency theory, there is a potential conflict of interest between shareholders and managers in decision-making regarding cash holdings and investments. For instance, during periods of high economic policy uncertainty, managers may increase the company’s cash holdings to mitigate potential risks and uncertainties (El Ghoul et al., 2023). However, high cash holdings can result in agency problems. Research by Javadi et al. (2021) indicates a negative relationship between economic policy uncertainty and corporate cash holdings, moderated by agency theory. Reducing cash holdings is seen as alleviating agency problems in conditions of high economic policy uncertainty.

In China and the United States, economic policy uncertainty can lead to delays in corporate investments (Duong et al., 2020). The relationship between cash holdings and investment decisions is also influenced by agency theory (Legesse et al., 2023). Managers tend to be more cautious and conservative in making investment decisions, prioritizing projects with higher chances of success and lower exposure to economic volatility (Su et al., 2020). In addition to affecting investment decisions, economic policy uncertainty can also impact cash holdings in relation to agency theory. Economic policy uncertainty can create additional challenges for companies in securing external funding for their investment projects. Lenders and investors may become more hesitant to provide funding during high uncertainty, leading to higher external financing costs and stricter loan terms (Phan et al., 2019). As a result, companies might rely more on internal cash resources, increasing cash holdings.

In times of high economic policy uncertainty, strategic financial planning becomes more critical as companies navigate uncertain periods. In such situations, companies need to adjust their cash holding behaviors and the sensitivity of cash holdings to cash flow variations (El Ghoul et al., 2023). Economic policy uncertainty can significantly impact corporate cash holding decisions (Su et al., 2020). Thus, managing risks and uncertainties in corporate finance is a crucial aspect of financial management (X. Li, 2019). This is because cash reserves act as a buffer for companies during economic instability (El Ghoul et al., 2023).

Despite the growing body of literature on economic policy uncertainty (EPU), a significant geographic and thematic imbalance remains. Current research is predominantly concentrated on developed economies, particularly the United States and China, leaving the dynamics of EPU in emerging markets largely underrepresented. Furthermore, existing studies often analyze the impacts on cash holdings and investment as isolated phenomena, failing to provide an integrated framework that incorporates the moderating role of agency conflicts. Our study addresses these gaps by synthesizing 105 Scopus-indexed articles to build a comprehensive conceptual map. By doing so, it not only highlights the unique challenges faced by firms in developing regions but also offers a more holistic understanding of how policy uncertainty shapes managerial behavior across diverse institutional contexts. Consequently, literature review is essential to identify these gaps and expand findings as a basis for future research. To achieve these research objectives, the following research questions (RQs) are formulated:

RQ1. How does the economic policy uncertainty (EPU) mechanism specifically impact corporate strategic decisions regarding cash holdings and investment efficiency?

RQ2. To what extent does agency theory explain the divergence in managerial responses to EPU across different institutional environments?

RQ3. What are the prevailing research gaps in current literature regarding the representation of emerging economies in EPU studies?

The remainder of this paper is structured as follows. Section 2 details the systematic literature review (SLR) methodology, including the PRISMA framework and bibliometric criteria used for article selection. Section 3 presents the findings of the bibliometric analysis, highlighting publication trends, dominant journals, and geographical distributions. Section 4 provides a deep qualitative synthesis of the nexus between EPU, cash holdings, and investment efficiency through the lens of agency theory while also identifying critical research gaps. Finally, Section 5 concludes the study by summarizing the key insights, discussing practical implications for policymakers and corporate managers, and offering specific recommendations for future research in emerging markets.

2. Methodology

A literature review is necessary in research for several reasons. First, it provides background information and context for the research, helping readers understand the topic (Richter et al. 2020). Second, it helps identify gaps or weaknesses in the existing knowledge base, which can justify the need for the research. Third, it allows researchers to relate their study to previous similar research, whether by filling gaps, expanding findings, or challenging prevailing ideas (Goodfellow, 2023). Additionally, a literature review helps researchers identify practical and theoretical issues related to the research and guides the formulation of research objectives, questions, or hypotheses. A well-conducted literature review serves as a guide to understanding the components and style of well-written reviews, thus identifying areas for future research.

To uncover the impact of economic policy uncertainty on companies, an adequate literature review is necessary. This involves a systematic literature review (SLR) carried out in four structured stages: identifying keywords, searching the literature, extracting relevant data, and conducting analysis. This method provides a summary and overview of the relationships among a series of related articles and helps synthesize these articles to provide a comprehensive view of the key areas. The literature review was conducted using the Scopus database, chosen for its popularity and comprehensive coverage, offering substantial and reliable publications for academics (Caviggioli & Ughetto, 2019). While the use of multiple databases (such as Scopus and Web of Science) is generally encouraged to enhance comprehensiveness, Scopus alone was selected in this study because: (1) it provides comprehensive indexing of peer-reviewed journals across economic, business, and finance disciplines; (2) it offers transparent and replicable search algorithms; (3) it has been established as adequate for similar systematic literature reviews in the economic policy uncertainty domain; and (4) the single database approach was applied consistently across a defined time frame to prevent bias from ongoing updates. The article search was performed within a single time frame (January 19, 2026) to prevent bias from ongoing database updates. The process involved three stages: searching for related articles, screening articles, selecting articles, and conducting analysis.

1. Searching for Articles

The keyword formula was systematically constructed based on established terminology in the EPU literature, particularly drawing from seminal works by Baker et al. (2016), who introduced the Economic Policy Uncertainty Index. The search strategy employed the Boolean operators as presented in Table 1, combining keywords such as “Global Economic Policy Uncertainty,” “Economic Policy Uncertainty,” “Corporate,” “Firm,” and “Company” to capture all relevant publications addressing the nexus between policy uncertainty and corporate financial decisions. Article searches were conducted on the Scopus website using the criteria detailed in Table 1.

Table 1

Article Search Criteria

|

Inclusion |

Exclusion |

|---|---|

|

Articles must contain the keywords (“Global Economic Policy Uncertainty” OR “Economic Policy Uncertainty”) AND (“Corporate” OR “Firm” OR “Company”). |

Articles that do not contain the keywords (“Global Economic Policy Uncertainty” OR “Economic Policy Uncertainty”) AND (“Corporate” OR “Firm” OR “Company”). |

|

Must be written in English. |

Articles not written in English are excluded. |

|

Must be published in peer-reviewed journals from academic sources. |

Articles from non-peer-reviewed publications such as books, book chapters, theses/dissertations, working papers, conference papers, and predatory journals are excluded. |

2. Identifying Articles

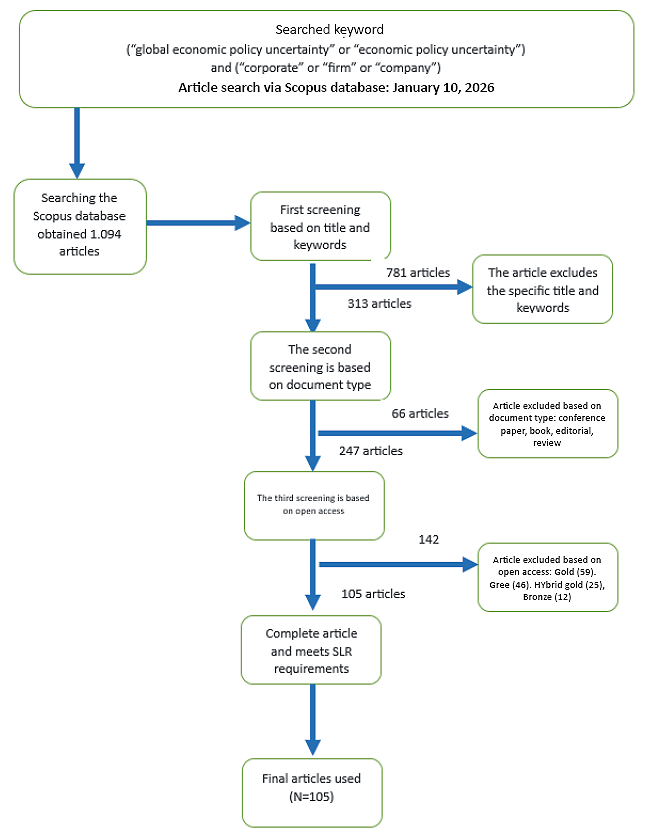

In the process of identifying articles, the PRISMA (Preferred Reporting Items for Systematic Review and Meta-Analyses) diagram (Figure 1) was used for easier identification. A search in the Scopus database with the specified criteria yielded 1.094 articles. The next step involved the first screening by examining the titles and keywords of each article. In this stage, 781 articles were excluded as they did not meet the keyword requirements of the first stage. The second screening was conducted on 313 articles by examining the document type, resulting in 66 articles that met the criteria. The third screening stage involved a detailed examination of the content completeness of 247 articles and open access, and eight articles were excluded due to incomplete content. After the final screening, 105 articles were deemed appropriate. Figure 1 shows the complete data extraction process using the PRISMA guidelines, which provide a framework for conducting and reporting systematic literature reviews (Moher et al., 2016).

Figure 1

Systematic Literature Review Information Flow Using PRISMA

The paper includes articles published in journals ranked from Q1 to Q4 in Scopus to capture the breadth of scholarship on this emerging topic. While higher-ranked journals typically indicate stronger methodological rigor, this inclusive approach was adopted because: (1) the field of economic policy uncertainty research is relatively recent (beginning substantially in 2016–2018), and significant contributions appear across journal quality tiers; (2) Q2–Q4 journals often feature empirical studies with robust datasets and novel country contexts, particularly from emerging markets; (3) restricting to Q1 journals alone would severely limit the representation of developing economy research, which is a key focus of this review. The bibliometric distribution (Q1: 70 articles, Q2: 25 articles, Q3: 8 articles, Q4: 2 articles) reflects this deliberate strategy to maintain geographic and thematic diversity. Alternative quality classifications such as the Academic Journal Guide (AJG) could be incorporated in future reviews to strengthen methodological rigor further.

The analytical steps were carried out by synthesizing influential research studies using a narrative synthesis approach. This approach is employed by researchers to summarize research findings from various studies. Initially, it provides a brief overview of prominent characteristics such as objectives, theoretical frameworks, and variables examined.

3. Findings

The findings are organized to directly address each of the three research questions formulated in the Introduction. Below, we present the results in a structured manner that maps explicitly RQ1, RQ2, and RQ3.

3.1 Profile of Reviewed Articles

A total of 105 articles were deemed suitable for further analysis. Based on their reputation, these articles were classified into Q1 to Q4 journals. The distribution was predominantly in Q1 with 70 articles, Q2 with 25 articles, Q3 with 8 articles, and Q4 with 2 articles. The distribution of journal rankings is shown in Figure 2.

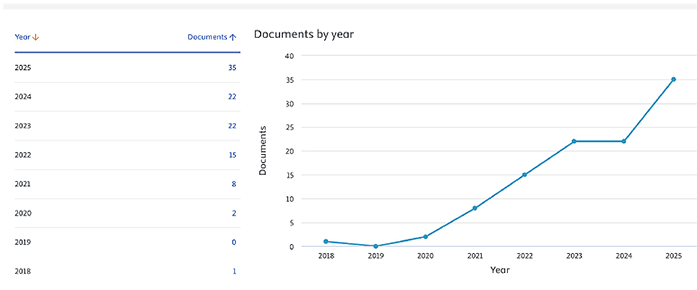

Journal Rankings: Research on economic policy uncertainty affecting companies began to be discussed in 2015. In 2016, researchers Scott R. Baker, Nicholas Bloom, and Steven J. Davis introduced the economic policy uncertainty (EPU) Index. Between 2015 and 2017, there were only two articles related to the EPU, the two mentioned above. Therefore, this article begins its analysis in 2018. This index is a key tool for measuring economic policy uncertainty (Al-Thaqeb & Algharabali, 2019). Research on economic policy uncertainty related to companies saw rapid growth starting in 2020, likely triggered by the COVID-19 pandemic. The pandemic increased the economic policy uncertainty index, prompting practitioners and academics to study it to better predict the future and minimize risks. This distribution is depicted in Figure 3.

Figure 2

Journal Ranking

Figure 3

Sample Distribution by Publication Year

The articles used were published by well-known publishers such as Elsevier, Routledge, Emerald, and many others, as shown in Figure 4. Over fifty percent of the articles were published by Elsevier, whether Elsevier Ltd, Inc, or B.V. The representation of countries was dominated by research from developed countries such as the United States and China, with only a few studies focusing on developing countries. The impact of economic policy uncertainty on developing countries is underrepresented, indicating a need for further encouragement in this area.

Table 2

Sample Distribution by Publisher

|

Publisher |

Quantity |

|---|---|

|

Academic Press Inc. |

1 |

|

Blackwell Publishing |

4 |

|

Cogent OA |

2 |

|

Elsevier (Ltd, Inc, B.V) |

59 |

|

Emerald (Publishing, Group Holdings Ltd.) |

8 |

|

Frontiers Media S.A. |

1 |

|

John Wiley and Sons (Ltd, Inc.) |

3 |

|

MDPI |

1 |

|

Routledge |

16 |

|

SAGE Publications (Inc., Ltd) |

2 |

|

Springer Science and Business Media Deutschland GmbH |

5 |

|

Sun Yat-sen (Zhongshan) University |

2 |

|

Wiley-Blackwell |

1 |

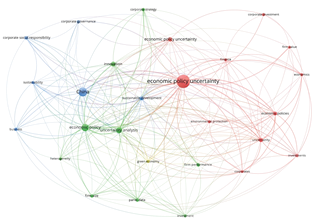

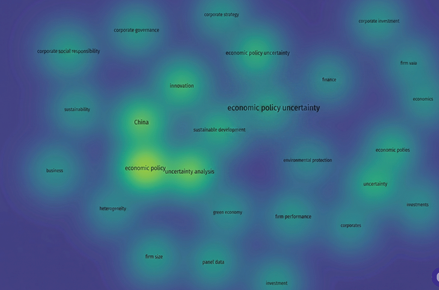

Before synthesizing, article analysis was conducted. To analyze the articles and identify research gaps, VOSviewer software was used. By utilizing VOSviewer, the data were analyzed by measuring the relationships between keywords based on their co-occurrence in documents. This co-occurrence analysis helps researchers identify and visualize the relationships between keywords, providing additional insights into the article analysis. Figure 4 shows that the discussion of the 105 articles is divided into four clusters. The first cluster, marked in red, includes eight keyword items: Cash Flow, Cash Holdings, Corporate Cash Holdings, Economic Policy Uncertainty, Financial Constraints, Financial Development, Investor Protection, Policy Uncertainty. The second cluster, marked in green, includes four items: Economic Policy Uncertainty, Cash Holding, Firm Value, Corporate Investment. The third cluster, marked in blue, includes three items: Investment, Corporate Governance, Corporate Social Responsibility, while the fourth cluster (marked in yellow) includes two items: China and Firm Performance. From the first and third clusters, researchers see opportunities for further research on economic policy uncertainty, for example, related to investment and cash holdings. This is due to the presence of smaller nodes indicating that discussions on investment and cash holdings are still limited.

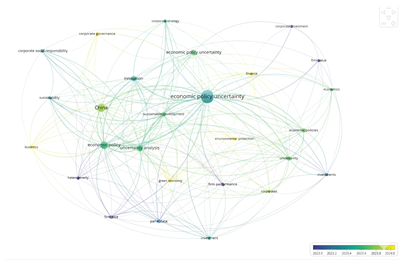

The discussion on economic policy uncertainty related to investment was widely covered in 2020 (see Figure 5). However, its connection to cash holdings only emerged in 2022, indicating further research opportunities. Additionally, Figure 6 shows that the area of cash holdings and investment remains underexplored, reinforcing the researchers’ belief in the potential to uncover more about economic policy uncertainty in relation to corporate investment and cash holdings. This is because the discussion on economic policy uncertainty is dynamic and significantly impacts corporate financial decisions (Al-Thaqeb & Algharabali, 2019).

Figure 4

Network Visualization

Note. List of clusters:

Cluster 1 (Red): economic policy uncertainty, finance, environmental protection, firm value, investment

Cluster 2 (Green): economic policy, innovation, firm size, corporate strategy

Cluster 3 (Blue): China, sustainability, corporate governance, corporate social responsibility

Cluster 4 (Yellow): green economy

Figure 5

Overlay Visualization

Figure 6

Density Visualization

Regarding Research Question 3 (emerging economy representation), the bibliometric analysis reveals a critical geographic imbalance in EPU research. Of the 105 articles analyzed, developed economies (United States and China) account for approximately 65% of the empirical studies, while emerging and developing economies represent less than 15% of the sample. This substantial underrepresentation indicates that current knowledge about EPU effects on corporate cash holdings and investment decisions are heavily skewed toward developed market contexts. Despite experiencing significant political volatility, countries such as Brazil, India, Indonesia, Mexico, and South Africa are largely absent from the scholarly discourse. This gap represents a major opportunity for future research to extend EPU frameworks to institutional contexts characterized by weaker governance structures, less mature capital markets, and higher policy volatility.

3.2 Impact of Economic Policy Uncertainty

Concerning Research Question 1 on EPU mechanisms, economic policy uncertainty operates through distinct pathways to influence corporate strategic decisions regarding cash holdings and investment efficiency. Economic policy uncertainty (EPU) is a complex phenomenon arising from the dynamic interaction between international political pressures and domestic legislative responses. While EPU refers to the unpredictability of government policies affecting the economic system, its complexity is further intensified by an intricate relationship with global geopolitical shifts, domestic regulatory changes, and systemic shocks such as the COVID-19 pandemic (Mamman et al., 2023; Shi & Wang, 2023). Geopolitical tensions—such as trade wars or regional conflicts—often serve as the primary trigger, creating uncertainty about global trade stability and forcing governments to abruptly adjust domestic regulations, including tax rates and investment rules, to protect national interests.

Furthermore, the emergence of global risks, exemplified by the COVID-19 pandemic, acts as a catalyst that amplifies this uncertainty across national borders. These global shocks often necessitate the adoption of unpredictable emergency policies, which can simultaneously exacerbate geopolitical tensions and fundamentally alter the regulatory landscape on a large scale. These three aspects—geopolitics, global risks, and domestic regulation—are interconnected through a domino effect (Shi & Wang, 2023), where global shocks trigger geopolitical shifts that manifest in regulatory changes. By distinguishing EPU from general economic volatility, this study highlights how this convergence creates a unique environment of information asymmetry, compelling firms to prioritize liquidity and defer strategic investments to navigate the heightened risk landscape.

The impact of economic policy uncertainty on companies and the global economy is substantial. It influences financial decisions and corporate behavior, often leading to conservative actions such as slowing down investments (Al-Thaqeb & Algharabali, 2019; Feng et al., 2021; Klayme et al., 2023; Vo et al., 2023) and holding larger cash reserves (Cheng et al., 2018; Duong et al., 2020b; Legesse et al., 2023; Lin et al., 2023). Previous literature reviews have revealed that high levels of economic policy uncertainty have detrimental effects on households, companies, and governments, impacting financial decision-making, reducing consumption, and lowering investment.

The impact of economic policy uncertainty on corporate investment is significant, affecting both foreign (W. L. Wu & Shao, 2023) and domestic investments (Feng et al., 2023; Im et al., 2021). High economic policy uncertainty can lead to a decline in corporate investment decisions (Klayme et al., 2023). This is because businesses hesitate to commit to financial and investment decisions when economic policies are uncertain (Dejuan-Bitria & Ghirelli, 2021). Additionally, companies tend to delay investments (Vo et al., 2022) due to the increased cost of external financing associated with high uncertainty, making it challenging for firms to secure the necessary funding for investments.

In times of high uncertainty, companies tend to be cautious by holding higher cash reserves (Demir & Ersan, 2017; Heeney et al., 2023; Seo & Mun, 2022). Cash holdings act as a safety net during periods of high uncertainty (Javadi et al., 2021), enabling companies to cope with potential financial challenges or seize new opportunities that may arise. Furthermore, economic policy uncertainty can affect investor sentiment, heightening concerns about adverse managerial actions. As a result, companies may increase their cash holdings to reassure investors and demonstrate financial stability (Legesse et al., 2023; Phan et al., 2019).

The EPU Index, developed by Baker et al.(2016), measures the level of economic policy uncertainty taking into consideration three main factors: economic news, government policy uncertainty, and business prospects. Economic news is evaluated based on the frequency of economic reports in the media, combined with assessments of government policy uncertainty affecting the economy and the perceived business outlook by business actors. This Baker index of policy uncertainty has been widely used in previous studies (Attig et al., 2021; Chiang, 2020; Heeney et al., 2023; Javadi et al., 2021; Makosa et al., 2021; C. P. Nguyen & Lee, 2021; Phan et al., 2019). Results indicate that economic policy uncertainty often has negative impacts on companies, such as financial aspects like cash holdings (Liu et al., 2021), cash flow (Z. Li et al., 2023), financial markets (Aydin et al., 2022), or investment decisions (J. Wu, Zhang, Zhang et al., 2020).

Economic policy uncertainty refers to the level of ambiguity and uncertainty surrounding government policies and regulations. This includes factors such as changes in monetary policy, fiscal policy, trade agreements, and regulatory frameworks that affect businesses and the economies of companies and countries. The impact of economic policy uncertainty is broad and has significant consequences for companies and nations (Al-Thaqeb & Algharabali, 2019). One of its effects is an increase in cash holdings (Feng et al., 2023; Javadi et al., 2021) and a decrease in investments (Im et al., 2021; Jing et al., 2023; Vo et al., 2023). However, the impact of economic policy uncertainty can vary depending on the country and region (Hou et al., 2021).

3.3 Corporate Cash Holdings

Economic policy uncertainty has significant implications for corporate cash holdings. Companies and management seek stable and predictable economic policies to make financial decisions, including decisions regarding cash holdings. Based on a review of articles, economic policy uncertainty has both positive and negative impacts on corporate cash holdings. Research in China (Legesse et al., 2023; Lin et al., 2023; Makosa et al., 2021; Zeng et al., 2020) indicates that companies tend to hold more cash as a precautionary motive by reducing inventories and lowering their investment value. Similar trends are observed in other developed countries like the United States (Cheng et al., 2018; Duong et al., 2020; Hankins et al., 2020; Heeney et al., 2023). Companies in the U.S. maintain high cash reserves during periods of high uncertainty due to precautionary motives (Phan et al., 2019). Strategies to increase cash holdings include reducing tax rates (M. Nguyen & Nguyen, 2020) and delaying investments (Trinh et al., 2022).

On the other hand, companies in Singapore respond differently to high economic policy uncertainty regarding cash holdings. Companies there tend to reduce cash holdings as EPU increases due to speculative incentives (Vuong et al., 2023) and the belief that the risks of holding cash outweigh the benefits (El Ghoul et al., 2023; Liu & Zhang, 2020). During periods of economic policy uncertainty, companies might see investment opportunities as greater than the risks of holding cash (Cui et al., 2022), leading them to invest rather than hold cash. High economic policy uncertainty also prompts companies to pay dividends to regain public trust (Attig et al., 2021). Economic policy uncertainty positively impacts cash holdings because companies increase their cash reserves as a precautionary measure to address investor concerns. However, high cash holdings can lead to new issues, such as conflicts of interest between shareholders and managers, as stated in agency theory. To avoid these agency problems, companies tend to reduce their cash holdings (Benkraiem et al., 2023; Feng et al., 2022), and agency problems tend to moderate the negative relationship between cash holdings and agency issues (Javadi et al., 2021).

Agency theory posits that the relationship between shareholders and managers can be influenced by economic policy uncertainty. In times of high economic policy uncertainty, managers may lean towards conservative strategies that prioritize cash savings and risk minimization. Conversely, shareholders seek to maximize the value of their investments. This conflict can be mitigated through effective corporate governance practices and aligning incentives between shareholders and managers (Benkraiem et al., 2023).

Agency theory is a framework that explores the relationship between principals (shareholders) and agents (managers) within an organization. It highlights that agents’ actions may not always align with the principals’ best interests, leading to agency costs (Rajan & Zingales, 1998). One focus area in agency theory is the decision-making process regarding corporate cash holdings. Several studies have examined the relationship between agency theory and cash holdings (Attig et al., 2021; Feng et al., 2022; Javadi et al., 2021). These studies found that managers, as agents, might prefer higher levels of cash to mitigate agency costs and reduce potential conflicts of interest with shareholders. The above studies indicate that agency theory plays a role in corporate decision-making processes concerning cash holdings.

Regarding agency theory’s explanatory power (Research Question 2), the relationship between EPU and corporate cash holdings is substantially moderated by agency conflicts across different institutional environments. In developed markets (United States, China), companies tend to increase cash holdings during high EPU periods due to precautionary motives. However, agency theory suggests that managers may exploit high cash positions to pursue personal interests, leading share-holders to demand stricter governance and potentially higher dividend payouts. Research indicates that effective agency conflict mitigation (through board independence, institutional monitoring, and executive compensation structures) moderates this relationship, with better-governed firms showing more optimal cash adjustment strategies. In emerging markets, the institutional environment differs substantially. Weaker legal protection for minority shareholders and less sophisticated governance mechanisms means that EPU-induced cash accumulation creates even greater agency problems. Additionally, in some emerging economies (such as Singapore, as noted in the literature), firms respond differently—reducing cash holdings despite high EPU due to speculative incentives or belief that investment opportunities outweigh holding risks. This divergence demonstrates that predictions of agency theory vary significantly across institutional environments. These patterns substantiate that agency theory partially explains managerial divergence across contexts, although the strength of the relationship depends critically on institutional quality, governance mechanisms, and capital market maturity.

The mentioned studies highlight various factors influencing a company’s decision to hold cash. These factors include internal company conditions, economic recessions, financing constraints, industry growth, and the macro environment (Zhou et al., 2021). The macro environment encompasses economic policy uncertainty, while internal company conditions involve agency conflicts, among other things. These findings suggest that agency theory provides valuable insights into the motivations behind corporate cash holding decisions and their relation to managers’ actions as agents and their potential conflicts with shareholders. Additionally, the research indicates that a company’s funding conditions, such as the availability of external funding and financial constraints, significantly affect cash flows and cash holding levels.

3.4 Corporate Investment

The impact of economic policy uncertainty (EPU) on investment has been a compelling and debated topic among policymakers, researchers, and the business community. For businesses, companies and investors rely on stable and predictable economic policies to make decisions regarding capital allocation, expansion plans, and long-term investments. When faced with high economic policy uncertainty, companies hesitate to invest due to concerns about potential changes in regulations, taxes (M. Nguyen & Nguyen, 2020), or even trade policies (Dejuan-Bitria & Ghirelli, 2021). This hesitation can lead to reduced corporate investment, subsequently negatively impacting economic growth and employment (Akron et al., 2020a). In other words, increased economic policy uncertainty significantly affects corporations, particularly in their investment decisions.

The impact of high economic policy uncertainty can be both positive and negative. Previous studies have shown that economic policy uncertainty positively correlates with investment, e.g., in companies in India (Perrin & Weill, 2023; J. Wu, Zhang, Wu et al., 2020; J. Wu, Zhang, Zhang et al., 2020) and in foreign direct investment in China (W. L. Wu & Shao, 2023). In India, investment values from the United States and China increased despite high economic policy uncertainty (Chada, 2023b). During times of high uncertainty, companies also tend to increase their investment in innovation (P. T. Nguyen & Nguyen, 2023) to navigate through periods of high economic policy uncertainty.

Previous studies have found a negative relationship between economic policy uncertainty and investment, with samples from countries in Asia (Farooq et al., 2022) and America (Caixe, 2022; Dejuan-Bitria & Ghirelli, 2021). For instance, companies in China (Feng et al., 2021; Huang et al., 2021, 2023a; Im et al., 2021; Jing et al., 2023; Liu & Zhang, 2020) and America (Akron et al., 2020; Huang et al., 2023; Jumah et al., 2023) experienced a decrease in investment levels due to high economic policy uncertainty. In Korea, both state-owned and non-state-owned enterprises reduced their investments during periods of high economic policy uncertainty (Vo et al., 2023). The relationship between economic policy uncertainty and investment appears to be nonlinear, with the marginal effect of uncertainty diminishing during periods of high economic policy uncertainty. This underscores the importance of stable economic policies in encouraging business investment and fostering economic growth. Economic policy uncertainty can hinder decision-making and investment in various sectors, including tourism and energy (Hou et al., 2021). This indicates that economic policy uncertainty negatively impacts investment decisions across various industries and countries (Akron et al., 2020). In short, economic policy uncertainty significantly affects corporate investment decisions.

The influence of economic policy uncertainty on investment is well-documented by the aforementioned research. The discussion above shows that when there is high economic policy uncertainty, companies tend to be more cautious and conservative in making investment decisions. Companies may delay or reduce their investments because uncertainty creates a higher level of risk and makes it more difficult to accurately assess the potential returns on investments (Hou et al., 2021). This cautious approach is especially evident during periods of significant policy changes, such as tax policies, regulatory frameworks, or trade agreements (Al-Thaqeb et al., 2022). During these periods, companies are cautious, preferring to wait and hold their cash rather than make investment decisions (Dejuan-Bitria & Ghirelli, 2021). Although previous studies have explored the relationship between economic policy uncertainty and investment, there is still a need for further exploration in specific contexts to clarify the direction of the relationship between economic policy uncertainty and corporate investment.

4. Discussion and Directions for Future Research

4.1. Discussion

Navigating cash holdings and investment decisions amidst economic policy uncertainty presents multifaceted challenges for companies and management. The evidence synthesized in this review demonstrates that EPU creates information asymmetries that amplify agency conflicts. Management must carefully evaluate potential risks and benefits of investment opportunities while considering prevailing economic policies and uncertainty levels. Importantly, businesses should diversify their interventions across industries and regions to minimize exposure to policy changes in specific sectors (Hou et al., 2021). Businesses also need to consider diversifying their interventions to minimize exposure to policy changes in specific industries and regions (Akron et al., 2020). Additionally, maintaining open lines of communication with the government and policymakers can provide additional insights into potential policy changes and help companies anticipate and adapt to dynamic economic policy uncertainty. Therefore, it is crucial for businesses to conduct due diligence and thorough analysis before making investment decisions, considering factors such as the potential impact of policy changes.

Understanding the concepts of cash holdings and investment is essential for making sound financial management decisions for companies. Theories on cash holdings and investment provide valuable insights into the relationship between a company’s cash reserves and its investment decisions. The review of various studies and research findings mentioned above shows that several factors influence a company’s level of cash holdings (Gao et al., 2017). These factors include both internal and external elements. Internal factors may stem from management experiencing agency problems, such as differing desires between investors and management. Investors seek high investments expecting high returns, while management, cautious due to high economic policy uncertainty, tends to increase cash holdings for precautionary reasons. Therefore, having a comprehensive understanding of cash holdings and investment theories (Duong et al., 2020) enables businesses to manage their financial resources effectively and make informed decisions regarding cash holdings and investments. This highlights that cash holdings and investment theories are crucial aspects of corporate finance as they help businesses make decisions based on the company’s financial resources (Denis & Sibilkov, 2009).

Understanding the relationship between government policy uncertainty and investment dynamics is crucial for investors and management (Phan et al., 2019). It allows them to adapt to policy changes, identify potential investment opportunities, and mitigate risks associated with economic policy uncertainty. Investors and management can implement several strategies to navigate an uncertain policy environment. Some possible strategies include:

1) Diversifying investments across various industries and regions: By spreading investments across different industries and regions, businesses can reduce the impact of economic policy changes (Jumah et al., 2023; Hou et al., 2021).

2) Analyzing economic policy developments: Monitoring and staying informed about policy changes, announcements, and their potential impacts will help investors and management anticipate and adapt to economic policy changes (Dejuan-Bitria & Ghirelli, 2021).

3) Maintaining cash reserves: Having sufficient cash reserves can provide flexibility for businesses during times of high economic policy uncertainty (Phan et al., 2019), although it may lead to agency conflicts. With these strategies, companies can mitigate the adverse effects of economic policy uncertainty.

Overall, economic policy uncertainty can significantly impact corporate cash holdings and investment decisions. The impact of economic policy uncertainty on cash holdings (Legesse et al., 2022) and investment decisions can be influenced by economic policy uncertainty and moderated by agency problems (Javadi et al., 2021). For instance, during periods of high economic policy uncertainty, businesses may choose to hold more cash as a precautionary measure to mitigate potential risks and ensure financial stability. Therefore, it is essential to further investigate how much cash holdings companies should maintain to effectively manage economic policy uncertainty while continuing to make profitable investments.

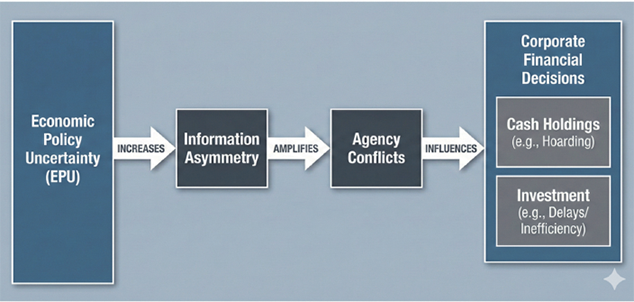

4.2 Conceptual Framework Formalization

Building on the synthesis of 105 articles, this review proposes a formal framework linking policy uncertainty to managerial behavior through agency theory mechanisms:

Figure 7

Conceptual Framework: Economic Policy Uncertainty, Information Asymmetry, Agency Conflicts and Corporate Financial Decisions

This framework illuminates that the relationship is not direct but mediated by the principal agent problem. High EPU increases information asymmetry, expanding the information gap between shareholders and managers. This widened asymmetry creates opportunities and incentives for opportunistic managerial behavior, leading to agency costs that moderate cash holding and investment decisions. The strength of this relationship varies significantly by institutional context, with stronger effects in weak-governance environments.

The practical implications of this research for corporate managers are based on the results above: Since EPU amplifies agency conflicts, it is important to maintain transparent communication with shareholders about strategic responses to uncertainty. Firms should implement robust governance mechanisms to mitigate agency costs during periods of high uncertainty. This framework illuminates that the relationship is not direct but mediated by the principal agent problem. High EPU increases information asymmetry, expanding the information gap between shareholders and managers. This widened asymmetry creates opportunities and incentives for opportunistic managerial behavior, leading to agency costs that moderate cash holding and investment decisions. The strength of this relationship varies significantly by institutional context, with stronger effects in weak-governance environments.

Policy makers should be aware that well-designed institutional frameworks and transparent regulatory environments can reduce the negative effects of EPU on corporate investment, thereby supporting economic growth. Investors should recognize that cash holdings and investment decisions vary by institutional context, which is essential for portfolio management and valuation in different market environments.

4.3 Directions for Future Research

The analyzed articles are sourced from high-quality journals. Most articles are published by renowned publishers such as Elsevier, Routledge, and Emerald, indicating that this topic garners attention from prominent publishers. The increase in research on this topic has been more prevalent in developed countries like the United States and China, while the lack of representation in developing countries highlights the need for further focus on the impact of economic policy uncertainty in these regions. Research on economic policy uncertainty began to develop around 2015 and saw a significant surge in 2020 during the COVID-19 pandemic, indicating high economic policy uncertainty. Researchers and practitioners have been attempting to make future forecasts to mitigate the associated risks. The COVID-19 pandemic heightened economic policy uncertainty, prompting the need for further analysis to minimize risks and to determine if there is a threshold level of economic policy uncertainty at which companies react to their cash holdings and investments.

Economic policy uncertainty has a significant impact on companies, particularly in their decisions regarding cash holdings (Avsar & Hudgins, 2022) and investments (Zheng, 2019). During periods of high economic policy uncertainty, management may prefer high cash holdings due to the desire to be cautious in the face of uncertainty (Duong et al., 2020; Guizani et al., 2023; Heeney et al., 2023) or, conversely, may choose to reduce cash holdings to minimize agency conflicts (Attig et al., 2021; Benkraiem et al., 2023; Javadi et al., 2021). High economic policy uncertainty significantly affects corporate investment decisions (Chada, 2023; Feng et al., 2023; Im et al., 2021; Klayme et al., 2023; Vo et al., 2023). This uncertainty can lead to reduced investment and conservative actions in capital allocation (Al-Thaqeb et al., 2022). However, the impact of economic policy uncertainty varies depending on the context of the country and region. Therefore, further analysis is needed in both developed and developing countries to better understand this phenomenon.

In analyzing the topic of economic policy uncertainty, most studies utilize the Barker Index (Barker et al., 2016). This index is available on the EPU Barker website but only covers a limited number of countries. Therefore, future researchers are encouraged to find alternative methods to obtain an economic policy uncertainty index, enabling the study of a wider range of countries regarding their economic policy uncertainty.

In the context of economic policy uncertainty, there is a lack of discussion regarding the relationship between shareholders and managers, necessitating further exploration. Economic policy uncertainty can lead to differing interests between shareholders and managers, potentially causing conflicts. One theory that can be used to further discuss this relationship is agency theory. Future research is recommended to explore the relationship between shareholders and managers under conditions of economic policy uncertainty by incorporating an agency theory framework.

The use of agency theory in the context of economic policy uncertainty is highly relevant because uncertain external conditions tend to widen the information asymmetry between shareholders (principals) and managers (agents). When government policies or geopolitical conditions become unpredictable, managers have better access to information regarding the actual impact on company operations than shareholders. This creates an opportunity for managers to engage in opportunistic actions or conceal performance inefficiencies by using economic uncertainty as an excuse. Consequently, shareholders must bear higher agency costs to monitor and ensure that every manager’s decision remains aligned with efforts to increase company value.

Furthermore, this theoretical framework is useful for exploring differences in risk preferences between the two parties during times of crisis. Shareholders generally expect optimal investment for long-term growth, but amid policy uncertainty, managers often exhibit risk aversion to safeguard their positions and professional reputations. This can trigger the phenomenon of underinvestment, where managers delay strategic projects that would otherwise be profitable. Through the perspective of agency theory, further research can identify how strong corporate governance mechanisms can mitigate these conflicts of interest so that companies remain competitive and resilient even in a turbulent policy environment.

The analysis reveals several critical directions for future research:

1. Geographic expansion: Future research should prioritize emerging markets (Brazil, India, Mexico, South Africa), where policy uncertainty is often acute but understudied. Comparative institutional analysis examining how EPU operates differently across different levels of governance quality would significantly advance the field.

2. EPU Index development: Most studies use the Baker Index, which covers a limited number of countries. Researchers are encouraged to develop alternative EPU indices or adapt existing indices for specific regional contexts thus allowing for broader geographic coverage.

3. Integration of agency theory: While this review identifies agency theory as central to understanding the impact of EPU, future research should explicitly formalize the moderating mechanisms through which agency costs influence cash holdings and investment. Longitudinal studies examining how governance mechanisms (board composition, institutional ownership, executive compensation structure) mitigate agency conflicts during periods of uncertainty would strengthen theoretical understanding.

4. Threshold effect analysis: Research should investigate whether there is a threshold level of EPU at which firm behavior shifts discontinuously—for example, at what level of uncertainty firms shift from precautionary cash accumulation to investment.

5. Visualization and mapping: As noted in the original research objective, explicit conceptual mapping through drawings, diagrams, and formal representations of constructs and relationships would enhance clarity and contribution.

5. Conclusion and Recommendations

This literature review has analyzed 105 articles related to economic policy uncertainty and its relationship with corporate financial decisions. Most articles were published by renowned publishers such as Elsevier, Routledge, and Emerald, dominated by Q1 journals, indicating the high quality of the analyzed articles. Research trends on economic policy uncertainty began to develop in 2015, spurred by the development of the EPU index by Baker, encouraging deeper exploration of this topic. In 2020, research on economic policy uncertainty increased significantly due to heightened uncertainty during the COVID-19 pandemic. The evidence demonstrates that EPU significantly impacts corporate cash holdings and investment decisions through information asymmetries that amplify principal–agent conflicts. High economic policy uncertainty leads to conservative corporate actions—slowing investment and increasing cash reserves—with these effects substantially moderated by agency conflicts and institutional context.

This review focuses exclusively on Scopus-indexed journals published between 2018 and 2025, potentially missing contributions in other databases or earlier foundational work. The predominance of developed economy studies limits the generalizability of findings to emerging markets. Additionally, the narrative synthesis approach, while comprehensive, differs from meta-analytic quantification of effects.

For future research, scholars should: (1) regularly expand analysis to emerging and developing economies using alternative EPU indices; (2) formalize and empirically test the proposed integrated conceptual framework linking policy uncertainty to managerial behavior through agency theory; (3) conduct comparative institutional analyses examining how government quality moderates EPU effects; and (4) investigate threshold effects and the nonlinearity of the relationship between EPU and corporate financial policies.

References

Ahmad, M. F., Aziz, S., El-Khatib, R., & Kowalewski, O. (2023). Firm-level political risk and dividend payout. International Review of Financial Analysis, 86(November 2022), 102546. https://doi.org/10.1016/j.irfa.2023.102546

Ahsan, T., & Qureshi, M. A. (2021). The nexus between policy uncertainty, sustainability disclosure and firm performance. Applied Economics, 53(4), 441–453. https://doi.org/10.1080/00036846.2020.1808178

Akron, S., Demir, E., Díez-Esteban, J. M., & García-Gómez, C. D. (2020). Economic policy uncertainty and corporate investment: Evidence from the U.S. hospitality industry. Tourism Management, 77(October 2019). https://doi.org/10.1016/j.tourman.2019.104019

Al-Thaqeb, S. A., & Algharabali, B. G. (2019). Economic policy uncertainty: A literature review. Journal of Economic Asymmetries, 20. https://doi.org/10.1016/j.jeca.2019.e00133

Attig, N., El Ghoul, S., Guedhami, O., & Zheng, X. (2021). Dividends and economic policy uncertainty: International evidence. Journal of Corporate Finance, 66. https://doi.org/10.1016/j.jcorpfin.2020.101785

Baker, S. R., Bloom, N., Davis, S. J. (2016). Measuring Economic Policy Uncertainty. The Quarterly Journal of Economics, 131(4), 1593–1636. https://doi.org/10.1093/qje/qjw024

Benkraiem, R., Gaaya, S., & Lakhal, F. (2022). Corporate tax avoidance, economic policy uncertainty, and the value of excess cash: International evidence. Economic Modelling, 108. https://doi.org/10.1016/j.econmod.2021.105738

Benkraiem, R., Gaaya, S., Lakhal, F., & Lakhal, N. (2023). Economic policy uncertainty, investor protection, and the value of excess cash: A cross-country comparison. Finance Research Letters, 52. https://doi.org/10.1016/j.frl.2022.103572

Borghesi, R., & Chang, K. (2020). Economic policy uncertainty and firm value: The mediating role of intangible assets and R&D. Applied Economics Letters, 27(13), 1087–1090. https://doi.org/10.1080/13504851.2019.1661951

Caixe, D. F. (2022). Corporate governance and investment sensitivity to policy uncertainty in Brazil. Emerging Markets Review, 51. https://doi.org/10.1016/j.ememar.2021.100883

Chada, S. (2023). Economic policy uncertainties and institutional ownership in India. Journal of Economic Asymmetries, 27. https://doi.org/10.1016/j.jeca.2023.e00293

Cheng, C. H. J., Chiu, C.-W. J., Hankins, W. B., & Stone, A.-L. (2018). Partisan conflict, policy uncertainty and aggregate corporate cash holdings. Journal of Macroeconomics, 58, 78–90. https://doi.org/10.1016/j.jmacro.2018.08.010

Cheng, C. H. J., Hankins, W. B., & Chiu, C. W. (2016). Does US partisan conflict matter for the Euro area? Economics Letters, 138, 64–67. https://doi.org/10.1016/j.econlet.2015.11.030

Cheng, Z., & Masron, T. A. (2023). Economic policy uncertainty and corporate digital transformation: Evidence from China. Applied Economics, 55(40), 4625–4641. https://doi.org/10.1080/00036846.2022.2130148

Clance, M., Gozgor, G., Gupta, R., & Lau, C. K. M. (2021). The relationship between economic policy uncertainty and corporate tax rates. Annals of Financial Economics, 16(1). https://doi.org/10.1142/S2010495221500020

Cui, D., Ding, M., Han, Y., & Suardi, S. (2022). Foreign shareholders, relative foreign policy uncertainty and corporate cash holdings. International Review of Financial Analysis, 84(July), 102399. https://doi.org/10.1016/j.irfa.2022.102399

Cui, X., Wang, C., Sensoy, A., Liao, J., & Xie, X. (2023). Economic policy uncertainty and green innovation: Evidence from China. Economic Modelling, 118. https://doi.org/10.1016/j.econmod.2022.106104

Dejuan-Bitria, D., & Ghirelli, C. (2021). Economic policy uncertainty and investment in Spain. SERIEs, 12(3), 351–388. https://doi.org/10.1007/s13209-021-00237-5

Demir, E., & Ersan, O. (2017). Economic policy uncertainty and cash holdings: Evidence from BRIC countries. Emerging Markets Review, 33, 189–200. https://doi.org/10.1016/j.ememar.2017.08.001

Dou, Z., Wei, L., & Wang, J. (2021). Institutional investor, economic policy uncertainty, and innovation investment: Evidence from China. E a M: Ekonomie a Management, 24(1), 4–20. https://doi.org/10.15240/TUL/001/2021-1-001

Duong, H. N., Nguyen, J. H., Nguyen, M., & Rhee, S. G. (2020). Navigating through economic policy uncertainty: The role of corporate cash holdings. Journal of Corporate Finance, 62. https://doi.org/10.1016/j.jcorpfin.2020.101607

El Ghoul, S., Guedhami, O., Mansi, S., & Wang, H. H. (2023). Economic policy uncertainty, institutional environments, and corporate cash holdings. Research in International Business and Finance, 65. https://doi.org/10.1016/j.ribaf.2023.101887

Farooq, U., Tabash, M. I., Anagreh, S., & Saleh Al-Faryan, M. A. (2022). Economic policy uncertainty and corporate investment: Does quality of governance matter? Cogent Economics and Finance, 10(1). https://doi.org/10.1080/23322039.2022.2157118

Feng, X., Lo, Y. L., & Chan, K. C. (2022). Impact of economic policy uncertainty on cash holdings: Firm-level evidence from an emerging market. Asia-Pacific Journal of Accounting and Economics, 29(2), 363–385. https://doi.org/10.1080/16081625.2019.1694954

Feng, X., Luo, W., & Wang, Y. (2021). Economic policy uncertainty and firm performance: Evidence from China. Journal of the Asia Pacific Economy. https://doi.org/10.1080/13547860.2021.1962643

Fujitani, R., Hattori, M., & Yasuda, Y. (2023). Domestic and international effects of economic policy uncertainty on corporate investment and strategic cash holdings: Evidence from Japan. Journal of the Japanese and International Economies, 69. https://doi.org/10.1016/j.jjie.2023.101272

García-Gómez, C. D., Demir, E., Chen, M.-H., & Díez-Esteban, J. M. (2022). Understanding the effects of economic policy uncertainty on US tourism firms’ performance. Tourism Economics, 28(5), 1174–1192. https://doi.org/10.1177/1354816620983148

Goodell, J. W., Goyal, A., & Urquhart, A. (2021). Uncertainty of uncertainty and firm cash holdings. Journal of Financial Stability, 56. https://doi.org/10.1016/j.jfs.2021.100922

Guan, J., Xu, H., Huo, D., Hua, Y., & Wang, Y. (2021). Economic policy uncertainty and corporate innovation: Evidence from China. Pacific Basin Finance Journal, 67. https://doi.org/10.1016/j.pacfin.2021.101542

Guizani, M., Talbi, D., & Abdalkrim, G. (2023). Economic policy uncertainty, geopolitical risk and cash holdings: Evidence from Saudi Arabia. Arab Gulf Journal of Scientific Research, 41(2), 183–201. https://doi.org/10.1108/AGJSR-07-2022-0109

Gupta, G. (2022). CEO’s educational background, economic policy uncertainty and investment-cash flow sensitivity: Evidence from India. Applied Economics, 54(5), 568–579. https://doi.org/10.1080/00036846.2021.1967279

Hankins, W. B., Stone, A.-L., Cheng, C. H. J., & Chiu, C.-W. (2020). Corporate decision making in the presence of political uncertainty: The case of corporate cash holdings. Financial Review, 55(2), 307–337. https://doi.org/10.1111/fire.12205

Hao, Z., Zhang, X., & Wei, J. (2022). Research on the effect of enterprise financial flexibility on sustainable innovation. Journal of Innovation and Knowledge, 7(2). https://doi.org/10.1016/j.jik.2022.100184

He, F., Ma, Y., & Zhang, X. (2020). How does economic policy uncertainty affect corporate Innovation?–Evidence from China listed companies. International Review of Economics and Finance, 67, 225–239. https://doi.org/10.1016/j.iref.2020.01.006

Heeney, L., Yang, S., Chowdhury, H., & Tan, K. J. K. (2023). Corporate cash holdings through economic policy uncertainty: An Australian study. Pacific Basin Finance Journal, 79. https://doi.org/10.1016/j.pacfin.2023.102008

Hoang, K., & Tran, T. T. (2022). Policy uncertainty and intellectual capital investment. Applied Economics Letters, 29(15), 1369–1377. https://doi.org/10.1080/13504851.2021.1934383

Hou, F., Tang, W., Wang, H., & Xiong, H. (2021). Economic policy uncertainty, marketization level and firm-level inefficient investment: Evidence from Chinese listed firms in energy and power industries. Energy Economics, 100(June), 105353. https://doi.org/10.1016/j.eneco.2021.105353

Huang, H., Liu, H., & Yang, B. (2021). Economic policy uncertainty and executive turnover. China Journal of Accounting Research, 14(1), 83–100. https://doi.org/10.1016/j.cjar.2020.11.003

Huang, J., Jin, Y., Duan, Y., & She, Y. (2023a). Do Chinese firms speculate during high economic policy uncertainty? Evidence from wealth management products. International Review of Financial Analysis, 87. https://doi.org/10.1016/j.irfa.2023.102639

Huang, J., Luo, Y., & Peng, Y. (2021). Corporate financial asset holdings under economic policy uncertainty: Precautionary saving or speculating? International Review of Economics and Finance, 76, 1359–1378. https://doi.org/10.1016/j.iref.2019.11.018

Ilyas, M., Khan, A., Nadeem, M., & Suleman, M. T. (2021). Economic policy uncertainty, oil price shocks and corporate investment: Evidence from the oil industry. Energy Economics, 97, 105193. https://doi.org/10.1016/j.eneco.2021.105193

Ilyas, M., Mian, R. U., & Suleman, M. T. (2022). Economic policy uncertainty and firm propensity to invest in corporate social responsibility. Management Decision, 60(12), 3232–3254. https://doi.org/10.1108/MD-06-2021-0746

Im, H. J., Liu, J., & Park, Y. J. (2021). Policy uncertainty and peer effects: Evidence from corporate investment in China. International Review of Financial Analysis, 77(June), 101834. https://doi.org/10.1016/j.irfa.2021.101834

Javadi, S., Mollagholamali, M., Nejadmalayeri, A., & Al-Thaqeb, S. (2021). Corporate cash holdings, agency problems, and economic policy uncertainty. International Review of Financial Analysis, 77. https://doi.org/10.1016/j.irfa.2021.101859

Jiang, H., & Liu, C. (2020). Economic policy uncertainty, CEO characteristics and firm R&D expenditure: A Bayesian analysis. Applied Economics, 52(34), 3709–3731. https://doi.org/10.1080/00036846.2020.1721422

Jing, Z., Lu, S., Zhao, Y., & Zhou, J. (2023). Economic policy uncertainty, corporate investment decisions and stock price crash risk: Evidence from China. Accounting and Finance, 63(S1), 1477–1502. https://doi.org/10.1111/acfi.13077

Jumah, Z., Younas, Z. I., & Al-Faryan, M. A. S. (2023). Economic policy uncertainty, corporate diversification, and corporate investment. Applied Economics Letters, 30(19), 2732–2742. https://doi.org/10.1080/13504851.2022.2106028

Jun, X., Huang, W., Guo, Y., Cao, Y., & Lu, M. (2023). Why does economic policy uncertainty increase firm-level pollutant emission? Economic Modelling, 129. https://doi.org/10.1016/j.econmod.2023.106537

Klayme, T., Gokmenoglu, K. K., & Rustamov, B. (2023). Economic policy uncertainty, COVID-19 and corporate investment: Evidence from the gold mining industry. Resources Policy, 85(PA), 103787. https://doi.org/10.1016/j.resourpol.2023.103787

Kong, Q., Li, R., Wang, Z., & Peng, D. (2022). Economic policy uncertainty and firm investment decisions: Dilemma or opportunity? International Review of Financial Analysis, 83. https://doi.org/10.1016/j.irfa.2022.102301

Legesse, T. S., Guo, H., Wang, Y., Tang, J., & Wu, Z. (2023). The impact of economic policy uncertainty and financial development on the sensitivity of corporate cash holding to cash flows. Applied Economics, 55(32), 3728–3746. https://doi.org/10.1080/00036846.2022.2117781

Lynda, T, Goodfellow. (2023). An Overview of How to Search and Write a Medical Literature Review. Respir Care, 68(11),1576-1584. doi: 10.4187/respcare.11198

Lin, H., He, S., Wang, M., & Yan, Y. (2023). The influence of peers’ MD&A tone on corporate cash holdings. International Review of Economics and Finance, 86, 865–881. https://doi.org/10.1016/j.iref.2023.04.006

Lin, Y., Fu, X., & Fu, X. (2021). Varieties in state capitalism and corporate innovation: Evidence from an emerging economy. Journal of Corporate Finance, 67. https://doi.org/10.1016/j.jcorpfin.2021.101919

Liu, G., & Zhang, C. (2020). Economic policy uncertainty and firms’ investment and financing decisions in China. China Economic Review, 63. https://doi.org/10.1016/j.chieco.2019.02.007

Liu, T., Chen, X., & Yang, S. (2022). Economic policy uncertainty and enterprise investment decision: Evidence from China. Pacific Basin Finance Journal, 75. https://doi.org/10.1016/j.pacfin.2022.101859

Lu, H., Gao, Q., & Yick, H. Y. (2023). Economic policy uncertainty and its mediating effect on leverage on the adjustment speed of corporate investment– evidence from China. Applied Economics Letters, 30(20), 2934–2946. https://doi.org/10.1080/13504851.2022.2115968

Ma, H., & Hao, D. (2022). Economic policy uncertainty, financial development, and financial constraints: Evidence from China. International Review of Economics and Finance, 79, 368–386. https://doi.org/10.1016/j.iref.2022.02.027

Makosa, L., Jie, S., Bonga, W. G., Jachi, M., & Sitsha, L. (2021). Does economic policy uncertainty aggravate financial constraints? South African Journal of Accounting Research, 35(2), 151–166. https://doi.org/10.1080/10291954.2021.1885233

Mirza, S. S., & Ahsan, T. (2020). Corporates’ strategic responses to economic policy uncertainty in China. Business Strategy and the Environment, 29(2), 375–389. https://doi.org/10.1002/bse.2370

Mun, S. G., & Jang, S. C. S. (2015). Working capital, cash holding, and profitability of restaurant firms. International Journal of Hospitality Management, 48, 1–11. https://doi.org/10.1016/j.ijhm.2015.04.003

Nguyen, M. H., & Trinh, V. Q. (2023). U.K. economic policy uncertainty and innovation activities: A firm-level analysis. Journal of Economics and Business, 123(July 2022), 106093. https://doi.org/10.1016/j.jeconbus.2022.106093

Nguyen, M., & Nguyen, J. H. (2020). Economic policy uncertainty and firm tax avoidance. Accounting and Finance, 60(4), 3935–3978. https://doi.org/10.1111/acfi.12538

Olalere, O. E., & Mukuddem-Petersen, J. (2023). Product Market Competition, Corporate Investment, and Firm Value: Scrutinizing the Role of Economic Policy Uncertainty. Economies, 11(6). https://doi.org/10.3390/economies11060167

Ongsakul, V., Jiraporn, P., & Treepongkaruna, S. (2021). Does managerial ownership influence corporate social responsibility (CSR)? The role of economic policy uncertainty. Accounting and Finance, 61(1), 763–779. https://doi.org/10.1111/acfi.12592

Ongsakul, V., Treepongkaruna, S., Jiraporn, P., & Uyar, A. (2021). Do firms adjust corporate governance in response to economic policy uncertainty? Evidence from board size. Finance Research Letters, 39. https://doi.org/10.1016/j.frl.2020.101613

Ozdemir, O., Erkmen, E., & Han, W. (2023). EPU and financial performance in the hospitality and tourism industry: Moderating effect of CSR, institutional ownership and cash holding. Tourism Management, 98. https://doi.org/10.1016/j.tourman.2023.104769

Perrin, C., & Weill, L. (2023). Girls will be girls? The gendered effect of economic policy uncertainty on corporate investment. Applied Economics, 00(00), 1–15. https://doi.org/10.1080/00036846.2023.2174935

Phan, H. V., Nguyen, N. H., Nguyen, H. T., & Hegde, S. (2019). Policy uncertainty and firm cash holdings. Journal of Business Research, 95, 71–82. https://doi.org/10.1016/j.jbusres.2018.10.001

Ren, X., Xia, X., & Taghizadeh-Hesary, F. (2023). Uncertainty of uncertainty and corporate green innovation—Evidence from China. Economic Analysis and Policy, 78, 634–647. https://doi.org/10.1016/j.eap.2023.03.027

Richter, O. Z., Kerres, M., Bedenlier, S., & Bond, M. (2020). Systematic reviews in educational research: Methodology, perspectives and application.

Rjiba, H., Jahmane, A., & Abid, I. (2020). Corporate social responsibility and firm value: Guiding through economic policy uncertainty. Finance Research Letters, 35. https://doi.org/10.1016/j.frl.2020.101553

Seo, D., & Mun, S. (2022). Economic policy uncertainty, social capital, and corporate cash holdings. Applied Economics Letters, 29(18), 1686–1689. https://doi.org/10.1080/13504851.2021.1958138

Sha, Y., Kang, C., & Wang, Z. (2020). Economic policy uncertainty and mergers and acquisitions: Evidence from China. Economic Modelling, 89, 590–600. https://doi.org/10.1016/j.econmod.2020.03.029

Shang, L., Lin, J.-C., & Saffar, W. (2021). Does economic policy uncertainty drive the initiation of corporate lobbying? Journal of Corporate Finance, 70. https://doi.org/10.1016/j.jcorpfin.2021.102053

Suh, H., & Yang, J. Y. (2021). Global uncertainty and Global Economic Policy Uncertainty: Different implications for firm investment. Economics Letters, 200. https://doi.org/10.1016/j.econlet.2021.109767

Su, X., Zhou, S., Xue, R., & Tian, J. (2020). Does economic policy uncertainty raise corporate precautionary cash holdings? Evidence from China. Accounting & Finance, 60(5), 4567-4592. https://doi.org/10.1111/acfi.12674

Trinh, N. T., Nguyen, T. P. T., & Nghiem, S. H. (2022). Economic policy uncertainty and other determinants of corporate cash holdings of Australian energy companies. International Journal of Energy Sector Management, 16(6), 1192–1213. https://doi.org/10.1108/IJESM-10-2020-0005

Vo, H., Nguyen, T., & Truong, H. (2023). Economic policy uncertainty and corporate investment: An empirical comparison of Korean chaebol and non-chaebol firms. Finance Research Letters, 54. https://doi.org/10.1016/j.frl.2023.103810

Vuong, T. H. G., Nguyen, H. M., & Wong, W.-K. (2023). Asian Academy of Management Journal of Accounting and Finance, 19(1), 1–27. https://doi.org/10.21315/aamjaf2023.19.1.1

Wang, M. (2021). Global evidence on macroeconomic variables and corporate money policy. Energy Systems, 0123456789. https://doi.org/10.1007/s12667-021-00494-0

Wang, Y., & Wang, X. (2023). Economic policy uncertainty and information intermediary: The case of short seller. Economic Modelling, 120. https://doi.org/10.1016/j.econmod.2022.106161

Wen, F., Li, C., Sha, H., & Shao, L. (2021). How does economic policy uncertainty affect corporate risk-taking? Evidence from China. Finance Research Letters, 41, 101840. https://doi.org/10.1016/j.frl.2020.101840

Wu, J., Zhang, J., Wu, Y., & Kong, D. (2020). When to go abroad: economic policy uncertainty and Chinese firms’ overseas investment. Accounting and Finance, 60(2), 1435–1470. https://doi.org/10.1111/acfi.12474

Wu, J., Zhang, J., Zhang, S., & Zou, L. (2020). The economic policy uncertainty and firm investment in Australia. Applied Economics, 52(31), 3354–3378. https://doi.org/10.1080/00036846.2019.1710454

Wu, W.-L., & Shao, C. (2023). How does home and host-country policy uncertainty affect outward FDI? Firm-level evidence from China. Economia Politica, 40(2), 495–515. https://doi.org/10.1007/s40888-023-00298-8

Yuan, T., Wu, J. G., Qin, N., & Xu, J. (2022). Being nice to stakeholders: The effect of economic policy uncertainty on corporate social responsibility. Economic Modelling, 108. https://doi.org/10.1016/j.econmod.2021.105737

Zeng, J., Zhong, T., & He, F. (2020). Economic policy uncertainty and corporate inventory holdings: Evidence from China. Accounting and Finance, 60(2), 1727–1757. https://doi.org/10.1111/acfi.12511

Zhao, T., & Chan, K. C. (2023). Corporate social network and corporate social responsibility: A perspective of interlocking directorates. International Review of Financial Analysis, 88. https://doi.org/10.1016/j.irfa.2023.102711

Zhao, T., Xiao, X., & Zhang, B. (2020). Economic policy uncertainty and corporate social responsibility performance: evidence from China. Sustainability Accounting, Management and Policy Journal, 12(5), 1003–1026. https://doi.org/10.1108/SAMPJ-05-2020-0158

Zhao, X., & Niu, T. (2023). Economic policy uncertainty and corporate cash holdings: the mechanism of capital expenditures. Asia-Pacific Journal of Accounting and Economics, 30(4), 930–950. https://doi.org/10.1080/16081625.2022.2054831

Zheng, S. (2019). Why do multinational firms hold so much cash? Further evidence on the precautionary motive. Journal of Multinational Financial Management, 50, 29–43. https://doi.org/10.1016/j.mulfin.2019.03.002

Zhou, H., Zhang, X., & Ruan, R. (2023). Firm’s perception of economic policy uncertainty and corporate innovation efficiency. Journal of Innovation and Knowledge, 8(3). https://doi.org/10.1016/j.jik.2023.100371

Zhu, H., Chen, W., Hau, L., & Chen, Q. (2021). Time-frequency connectedness of crude oil, economic policy uncertainty and Chinese commodity markets: Evidence from rolling window analysis. North American Journal of Economics and Finance, 57. https://doi.org/10.1016/j.najef.2021.101447