Organizations and Markets in Emerging Economies ISSN 2029-4581 eISSN 2345-0037

2026, vol. 17, no. 1(34), pp. 117–139 DOI: https://doi.org/10.15388/omee.2026.17.6

Why Do South African Companies Adopt the UN Sustainable Development Goals?

Alan Bandeira Pinheiro

NEOMA Business School, France

alanbpinheiro@hotmail.com

Ana Lidia de Oliveira Silva Ramalho

Federal University of Ceará, Brazil (UFC)

analidiaramalho@alu.ufc.br

Eduardo Becher de Lima Bernardo

Federal University of Paraná, Brazil (UFPR)

eduardobecher321@gmail.com

Nágela Bianca do Prado (corresponding author)

State University of Campinas (UNICAMP), Brazil

nagelabianca.prado@gmail.com

Abstract. Several previous studies have highlighted that the adoption of sustainable development goals in South Africa has contributed to poverty reduction, increased literacy rates, and progress in the fight against HIV. The purpose of this study is to understand the motivations underlying South African companies’ adoption of the UN Sustainable Development Goals and to assess the implications of this decision. To this end, the adoption of SDGs by 116 South African companies, focusing on board composition—specifically board size, diversity, skills, tenure, and independence—as antecedents, and corporate reputation as an outcome were analyzed. To analyze the data, we employed a mixed-methods approach, utilizing both multivariate analysis and fuzzy-set Qualitative Comparative Analysis (fsQCA). Both symmetric (multivariate analysis) and asymmetric (fsQCA) analyses provide strong evidence that three key board characteristics (gender diversity, board skills, and board independence) significantly influence the adoption of the SDGs. Additionally, the findings demonstrate that SDG adoption contributes to enhanced corporate social reputation. The findings have implications for both Agency Theory and Stakeholder Theory.

Keywords: Sustainable Development Goals, board composition, corporate reputation, agency theory, stakeholder theory, mixed-methods approach, emerging economies

Received: 5/6/2025. Accepted: 22/1/2026

Copyright © 2026 Alan Bandeira Pinheiro, Ana Lidia de Oliveira Silva Ramalho, Nágela Bianca do Prado. Published by Vilnius University Press. This is an Open Access article distributed under the terms of the Creative Commons Attribution Licence, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

1. Introduction

Over the past few years, sustainable development has become a strategic priority for both the business community and governments (Ferrero-Ferrero et al., 2023). In this context, the 2030 Agenda for Sustainable Development and its Sustainable Development Goals (SDGs) were launched in 2015 by 193 countries at the United Nations (UN) General Assembly (UN General Assembly, 2015). The initiative established a new framework to address the world’s most pressing challenges and ensure sustainable progress, based on five pillars: planet, people, prosperity, peace, and partnership, which help assess the 17 SDGs (UN General Assembly, 2015).

However, this poses significant challenges for developing countries, necessitating substantial financial, technical, and academic support. Many developing countries on the African continent face serious financial and economic constraints, making implementing the SDGs very challenging (Akanle et al., 2022). The latest report published by the Sustainable Development Goals Center for Africa, titled “The 2020 Africa SDG Index and Dashboards Report”, provides an assessment of where African countries stand with respect to the SDGs and their progress toward the goals, with the additional lens of “leave no one behind” (SDG Center for Africa, 2020).

According to the report, serious challenges remain, and most countries have demonstrated poor performance. Overall, stagnation and moderate improvement are the most common SDG trends, with African countries still struggling with various forms of inequality (Isaacs & Kaltenbrunner, 2018). Thus, there is an urgent call to action for business scholars to gather comprehensive insights into the factors driving progress toward the SDGs in Africa (SDG Center for Africa, 2020).

South Africa is experiencing extreme inequality, as reflected in one of the highest Gini coefficients globally (0.63), with approximately 13.2 million people (about 22% of the population) living in extreme poverty (Adetoro et al., 2023). In this context, the SDGs are crucial for countries like South Africa, offering long-term benefits if fully embraced by decision-makers. These benefits include reducing inequality and poverty, promoting workforce diversity, increasing literacy levels, combating HIV, addressing climate change, protecting the environment, achieving social acceptance, and increasing stakeholder satisfaction (Bose et al., 2024; Bose & Khan, 2022).

As the adoption of SDGs originates within the company, the board of directors sits at the top of the organizational hierarchy and is responsible for guiding the company’s strategic direction. Since boards of directors are involved in designing corporate strategies and setting organizational agendas, their policies and practices can significantly influence corporate behavior (Taglialatela et al., 2023), including whether they adopt SDGs initiatives.

Many studies have highlighted the determinants of corporate SDG adoption, such as industry sector (Emma & Jennifer, 2021; Pizzi et al., 2021), financial performance (Al-Qudah & Houcine, 2024; Emma & Jennifer, 2021), firm size (Al-Qudah & Houcine, 2024; Pizzi et al., 2021; Subramaniam et al., 2023), and separate sustainability committee (Subramaniam et al., 2023). However, it is less common to find studies in the literature that examine the board of directors as a determinant for adopting the SDGs (Subramaniam et al., 2023; Taglialatela et al., 2023).

Furthermore, the literature is still unaware of how the characteristics of board composition influence the adoption of the SDGs in emerging economies like South Africa, highlighting a research gap that this study aims to address. Although many studies suggest that socially responsible behaviors can positively impact corporate reputation, the specific effects of adopting the UN Sustainable Development Goals on corporate reputation remain underexplored in the literature. This is particularly relevant in emerging economies, where high inequality, significant poverty, and dual economic structures create complex environments in which corporate engagement with the SDGs may be shaped by both societal pressures and opportunities for contributing to sustainable development.

Therefore, the research question is: Why do South African companies adopt the UN Sustainable Development Goals? The purpose of this study is to understand the motivations underlying South African companies’ adoption of the UN Sustainable Development Goals and to assess the implications of this decision. To achieve the objective, we examined the adoption of SDGs by 116 South African companies, focusing on board composition – specifically board size, diversity, skills, tenure, and independence – as antecedents, and corporate reputation as an outcome.

Our findings have important theoretical and practical implications. Theoretically, we confirm agency theory by demonstrating that SDG adoption is influenced by board characteristics. We also support the Stakeholder Theory, demonstrating that companies that align their practices with the SDGs are better positioned to meet or surpass stakeholders’ expectations, thereby enhancing their reputation. Moreover, this paper is the first to examine the antecedents and outcomes of SDG adoption in South Africa, focusing on variables that are less explored in the literature. Practically, our findings can help managers and stakeholders assess and enhance corporate governance to foster greater organizational engagement with the SDGs.

2. Literature Review and Hypotheses Development

2.1 Agency Theory

According to agency theory (Fama & Jensen, 1983; Jensen & Meckling, 1976), one of the board’s main functions is to monitor managers in order to align their interests with those of shareholders and reduce agency costs. The board of directors is the most important internal corporate governance mechanism to oversee the CEO’s decisions (Ji et al., 2021).

The literature defends that effective boards provide companies with advice, knowledge, and resources to achieve strong sustainability performance (de Villiers et al., 2011), improve their ability to make necessary changes (Haniffa & Cooke, 2002), and enhance their legitimacy (Michelon & Parbonetti, 2012). García Martín and Herrero (2020) affirm that certain board characteristics can determine the implementation of sustainable strategies, such as the adoption of SDGs. Considering prior literature, this article considers the following board of directors’ variables that may influence SDG adoption in companies: size, diversity, skills, tenure, and independence.

Board size is a component of corporate governance that influences companies’ implementation and disclosure of sustainable initiatives (Cuadrado‐Ballesteros et al., 2017). In addition, larger boards are more likely to include directors with environmental expertise, prompting them to adopt global standards from a socio-environmental perspective, thereby supporting the SDGs (Taglialatela et al., 2023).

Buniamin et al. (2022) showed that companies with larger boards are more committed to achieving the SDGs in Malaysia. According to the authors, a larger number of board members indicates that the board has specific knowledge of sustainable strategies and integrates this understanding into the company’s operations. Other studies have found that board size positively influences the adoption of environmental SDGs globally (Taglialatela et al., 2023) and the adoption of the 2030 Agenda by companies in Latin America (Pinheiro, Ribeiro et al., 2024). On the other hand, Pinheiro, Lopes, et al. (2024) found that board size has a negative effect on SDGs in energy sector firms from emerging markets.

There is a lack of research on the relationship between board size and the adoption of SDGs in South Africa. However, a positive association between board size and sustainability performance has been observed in the Sub-Saharan Africa (SSA) region (Kwarteng et al., 2023).Therefore:

H1: Boards with a greater number of directors positively impact SDG adoption.

Gender diversity on boards adds a new dimension to corporate governance, as women bring fresh perspectives and drive policies on energy efficiency, green building, and climate change, thereby enhancing shareholder value and corporate citizenship (Jizi, 2017). According to Taglialatela et al. (2023), women tend to have greater influence in communities and leverage their networks to build alliances around sustainability issues. In this context, the authors argue that boards with a higher share of women are more likely to support SDG-related measures when setting strategic objectives for their firm.

The general opinion in the literature is that women demand higher levels of sustainability. The results by Rosati and Faria (2019) suggest a positive relationship between SDG reporting and the percentage of women on the directors’ board, with a sample of 408 organizations worldwide. The study by Taglialatela et al. (2023) showed that gender diversity on a board is a significant determinant of a firm’s support for the environmental SDGs among 4,417 globally listed firms. However, corporate SDG involvement was not influenced by the presence of female board members in Latin American (Pinheiro, Ribeiro, et al., 2024), Southeast Asian (Sekarlangit & Wardhani, 2021), or Malaysian (Buniamin et al., 2022) firms. Despite these mixed results, we hypothesize that in the South African context:

H2: Boards with a greater number of women positively impact SDG adoption.

According to Al Lawati and Hussainey (2022), boards with financial expertise are better prepared to oversee and mitigate agency conflicts within companies. In Nigeria, financial expertise equips board members with the financial competence necessary to perform their duties more effectively, which, in turn, enhances the firm’s performance (Arumona et al., 2019). Additionally, directors with a finance background are better equipped to understand the importance of social and environmental issues due to their training in social accounting (Ahmad et al., 2018).

In this context, directors with financial backgrounds tend to value society and the environment, which enhances their sense of responsibility and makes them more likely to encourage the company to engage in sustainable practices (Githaiga & Kosgei, 2023). Naheed et al. (2021) argue that directors with financial expertise understand the financial impact of non-financial sustainability disclosures and believe these disclosures enhance long-term corporate performance.

Furthermore, it is uncommon in the literature to use the financial background of board directors as a variable to analyze their influence on corporate sustainability strategies, such as SDG adoption. Githaiga and Kosgei (2023) discovered a positive association between board financial expertise and sustainability reporting in listed firms in East Africa. Al Lawati and Alshabibi (2023) found that SDG disclosures were positively associated with the presence of financial expertise among board directors. Therefore:

H3: Directors with a financial expertise positively impact SDG adoption.

Board members’ tenure can significantly influence their focus on sustainability issues. Directors with longer tenure are more familiar with the company’s operations, allowing them to better assess risks and seize opportunities related to environmental challenges (Katmon et al., 2019). Long-tenured directors possess deeper knowledge of corporate finance, making them more aware of strategic repercussions, which leads to a positive consideration of sustainability issues (Gallego-Álvarez & Rodriguez-Dominguez, 2023).

According to Padungsaksawasdi and Treepongkaruna (2024), among the board characteristics proposed to affect sustainability and Corporate Social Responsibility (CSR) initiatives, board tenure is one of the least discussed in the literature. The authors found a positive relationship between board tenure and CSR initiatives in companies in Thailand. While CSR and SDG adoption are related concepts, the specific relationship between board tenure and the adoption of the SDGs has not yet been analyzed in any known studies. Therefore:

H4: Directors with longer board tenure positively impact SDG adoption.

The independent board is associated with diversity in skills, knowledge, and stakeholders, helping to balance divergent interests and align financial and non-financial objectives of companies (Kwarteng et al., 2023). Taglialatela et al. (2023) argue that independent directors provide an outside perspective that insiders do not. According to the authors, these external perspectives can highlight the strategic and reputational value of participating in global efforts like supporting the SDGs.

The literature showed that board independence promotes better disclosure of the SDGs in Oman (Al Lawati & Alshabibi, 2023) and had a positive impact on companies’ contributions to the 2030 Agenda in European companies (Martínez-Ferrero & García-Meca, 2020) and Latin American companies (Pinheiro, Ribeiro, et al., 2024). Jiang et al. (2023) found that board independence favors firms addressing SDGs in their sustainability reporting in China. Other studies found that board independence was not a determinant for firms’ engagement with the SDGs in emerging economies (Pinheiro, Lopes, et al., 2024) and in Malaysia (Buniamin et al., 2022). Despite these mixed results, we hypothesize that in the South African context:

H5: A greater number of independent directors on the board positively impacts SDG adoption.

2.2 Stakeholder Theory

Corporate reputation is an organizational attribute that reflects how external parties perceive the company, evaluated based on its ability to meet the demands and expectations of individuals (Lin et al., 2016). According to Freeman (1984), firms exist within a network of relationships involving multiple stakeholders, each of whom holds legitimate interests in the firm. Organizational success is therefore contingent not only on shareholder value maximization but also on the firm’s capacity to recognize, balance, and satisfy diverse stakeholder expectations. In this sense, stakeholder theory allows understanding reasons to implement CSR practices, such as adopting the SDGs, and corporate reputation.

The core proposition of stakeholder theory is that firms have a diverse set of stakeholders, such as customers, suppliers, and employees, who make essential contributions to organizational success (Hossain et al., 2020). Accordingly, this theory is effective in providing both normative and instrumental foundations for the inclusion of stakeholders in managerial decision-making processes (Crane & Ruebottom, 2011). Thus, the descriptive dimension of stakeholder theory explains how organizations actually take stakeholder interests into account, as the literature assumes that there are three primary reasons why incorporating stakeholder interests through standards facilitates corporate performance objectives: (1) increased trust, (2) enhanced productivity, and (3) reduced exposure to government penalties (Gilbert & Rasche, 2008).

In contrast to an exclusive focus on shareholders, stakeholder theory positions the pursuit of the interests of groups and individuals identified as “stakeholders” as a central organizational objective (Gilbert & Rasche, 2008). In contemporary contexts, profit can no longer be the sole objective of corporations; hence, the management of relationships with stakeholders, including social and environmental concerns, has become an imperative (Russo & Perrini, 2010). Within this perspective, corporate strategies are increasingly evaluated according to their capacity to generate value that extends beyond financial performance, encompassing ethical conduct, social responsibility, and environmental stewardship (CSR) (Singla & Singh, 2024).

The adoption of the SDGs represents a concrete institutionalized framework through which firms can articulate and signal their commitment to addressing salient stakeholder demands (Kayikci et al., 2022). By aligning organizational practices with the SDGs, companies translate abstract stakeholder expectations into measurable objectives related to social inclusion, environmental protection, and responsible governance (Singhal, 2023). Corporate social reputation emerges in this context as a stakeholder-based evaluative outcome of SDG-oriented practices (Awa et al., 2024). As external stakeholders observe and interpret a firm’s engagement with the SDGs, they form collective judgments regarding the organization’s credibility, trustworthiness, and social responsibility (Pajuelo-Moreno, 2024).

In such a scenario, as stated by Lin-Hi and Blumberg (2018), CSR practices, in the sense of “doing good” (voluntary corporate engagement for the well-being of stakeholders and society), allow companies to positively exceed stakeholder expectations, which, according to the stakeholder theory, enhances corporate reputation. Analyzing the Brazilian context, Pinheiro et al. (2024) found that social responsibility practices improve corporate reputation. Therefore:

H6: SDG adoption positively impacts corporate social reputation.

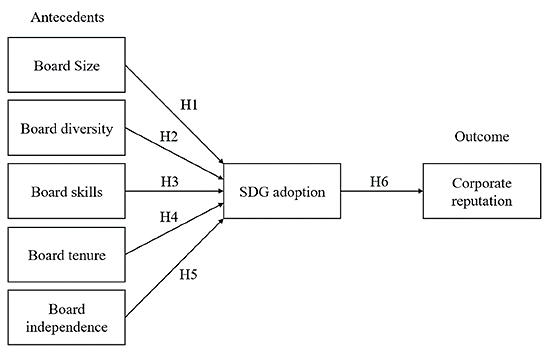

Figure 1 illustrates the theoretical model tested.

Figure 1

Conceptual Model

3. Research Design

This study investigates the antecedents and outcomes associated with the adoption of Sustainable Development Goals (SDGs) by 116 South African companies. To create this sample, we collected both financial and non-financial data from all 208 companies listed in the Refinitiv Eikon database. However, 92 companies were excluded due to incomplete data, leaving a final sample of 116 companies covering a five-year period from 2019 to 2023, the most recent years for which data was available at the time of collection. Additionally, a minimum of five years of data provides a strong foundation for econometric modeling, allowing for effective control of unobserved heterogeneity and endogeneity (García-Sánchez et al., 2025). Besides that, South Africa only established institutional mechanisms to implement the SDGs in 2019 (Mthembu & Nhamo, 2021). The sample selection process is detailed in Table I.

Table 1

Sample Selection

|

Sampling procedure |

Number of firms (n) |

Observations |

|---|---|---|

|

Companies listed in the Refinitiv Eikon database (Country: South Africa) |

208 |

1025 |

|

Companies with no information available covered by the Refinitiv Eikon database from 2019 to 2023 |

(92) |

(455) |

|

Final samples with complete financial and non-financial data |

116 |

572 |

The 116 companies analyzed are all listed on the Johannesburg Stock Exchange (JSE), which is currently ranked as the 19th largest stock exchange in the world by market capitalization and the largest in Africa. As part of the listing requirements, all JSE-listed companies are obligated to produce integrated reports in accordance with South Africa’s corporate governance codes (Haywood & Boihang, 2021).

Table 2 presents the variables used in the study. The adoption of SDGs is assessed based on the extent of SDG disclosure in the company’s public reports. This variable is quantified by summing the 17 SDGs, with a score ranging from 0 to 17. A score of 0 indicates that the company has not disclosed any SDGs, while a score of 17 signifies complete disclosure of all 17 SDGs.

Corporate social reputation is evaluated using the company’s social pillar score from the Refinitiv Eikon database, which is derived from a total of 63 indicators related to workforce management, human rights, community engagement, and product responsibility (Quintana-García et al., 2021).

Table 2

Description of Variables

|

Variable |

Description |

Authors |

|---|---|---|

|

Sustainable Development Goals (SDG) |

This variable is the sum of the 17 SDGs, ranging from 0 (if the company has not disclosed any SDGs) to 17 (if the company has disclosed all SDGs). |

Emma & Jennifer (2021) |

|

Social Reputation (REPUT) |

It is measured through the company’s social pillar score in the Refinitiv Eikon database. This score is based on a total of 63 indicators related to workforce, human rights, community and product responsibility and reflects the company’s reputation and the health of its license to operate. This ranges from 0 (lowest reputation) to 100 (highest reputation). |

Quintana-García et al. (2021) |

|

Board Size (BSIZE) |

Number of members on the board of directors |

Githaiga & Kosgei (2023) |

|

Board diversity (BDIVER) |

Percentage of women present on the board |

Gavana, Gottardo, & Moisello (2024) |

|

Board Skills (BSKILL) |

Percentage of board members who have a strong financial background |

García Martín & Herrero (2020) |

|

Board Tenure (BTENU) |

Average number of years each board member has been on the board |

Cahyono, Harymawan & Kamarudin (2023) |

|

Board independence (BINDEP) |

The percentage of independence of the board of directors |

Gallego-Álvarez & Rodriguez-Dominguez (2023) |

|

Company size (FSIZE) |

Natural log of the total assets |

Al Lawati & Hussainey (2022) |

|

Return on assets (ROA) |

It is measured using the ratio between net income and total assets. |

Al Lawati & Hussainey (2022) |

|

Market capitalization (MCAP) |

It is calculated by dividing the company’s net operating income by the current market value. |

Al Lawati & Hussainey (2022) |

|

Financial leverage (LEVER) |

It is measured using the ratio between total debt and total assets. |

Al Lawati & Hussainey (2022) |

|

Industry impact (INDUS) |

1 = if the company operates in a sector with a strong and direct environmental impact and 0 otherwise. |

Jizi (2017) |

|

Sustainability report (CSREP) |

1 = if the company has a sustainability report and |

Jizi (2017) |

To define the board characteristics, we selected five key governance variables: board size, board diversity, board skills, board tenure, and board independence. Board size refers to the total number of members on the company’s board of directors. Board diversity measures the level of gender diversity on the board, specifically by the proportion of female directors. Board skills refers to the percentage of board members who possess a strong financial background. Board tenure represents the average duration of service of the board of directors, and board independence indicates the proportion of independent directors, reflecting the board’s ability to provide unbiased oversight.

We include six control variables, selected based on findings from previous studies (Al Lawati & Hussainey 2022; García Martín & Herrero, 2020; Jizi, 2017; Quintana-García et al., 2021), which suggest that these factors may influence the adoption of SDGs. Company size is measured by the total assets of the company; return on assets is a measure of the company’s profitability, calculated as net income divided by total assets; and market capitalization refers to the total market value of the company’s outstanding shares.

Financial leverage is the ratio of the company’s total debt to equity, representing the financial risk undertaken by the company. In turn, industry impact is a variable that captures the company’s industry sector, given that different industries may have varying levels of SDG adoption. 1 is assigned to companies operating in the energy, industrial, materials, and utilities sectors (these industries typically have more significant environmental impact and therefore higher expectations regarding sustainability practices), and 0 is assigned to companies in all other sectors (Jizi, 2017). Finally, the sustainability report represents a binary variable indicating whether the company publishes a sustainability report.

The data analysis is conducted using two complementary methods: panel data regression with fixed effects and fuzzy set Qualitative Comparative Analysis (fsQCA). The equations below illustrate the econometric models.

To test hypotheses 1 through 5:

To test hypothesis 6:

After conducting the Hausman test, fixed effects were chosen. Fixed effects regression controls were used for unobserved heterogeneity across companies that could affect SDG disclosure and reputation, ensuring that the results account for differences that are constant over time but vary across companies. This method provides insights into the average effect of the independent variables on SDG disclosure and reputation while controlling for time-invariant company characteristics.

In addition to the main models, we conducted additional tests to enhance the validity of the findings. To assess multicollinearity, we examined the correlation matrix and calculated the Variance Inflation Factor (VIF). Moreover, the results of the Breusch-Pagan test confirmed that the errors exhibit constant variance (i.e., no heteroscedasticity). Furthermore, we performed Generalized Method of Moments (GMM) regressions to ensure the absence of endogeneity in the models (Hair Jr. et al., 2019).

Fuzzy Set Qualitative Comparative Analysis (fsQCA) is employed to explore the complex interactions between independent variables and other factors (control variables) that contribute to the disclosure of SDGs and reputation. fsQCA allows for the identification of different combinations of conditions that lead to high or low levels of SDG disclosure and reputation. This method is particularly useful in cases where there may be multiple paths to achieving the outcome of interest (Ragin, 1987).

Kumar et al. (2022) conducted a systematic review highlighting that fsQCA is a relatively new method in the management field, complementing traditional multivariate regressions. The review also revealed that the United States and the United Kingdom are the most studied contexts for this type of non-linear analysis, with a recommendation to apply this method in emerging countries.

4. Results

4.1 Descriptive Analysis

Table 3 displays the descriptive analysis of the variables. On average, companies adopted 6 of the 17 Sustainable Development Goals (SDGs), representing 35.29% of the total SDGs. The sample includes companies that did not adopt any SDGs between 2019 and 2023, as well as those that adopted all 17 SDGs during this period. The average social reputation score is 55 out of 100, with a minimum value of 1.75 and a maximum value of 96.02.

Table 3

Descriptive Analysis

|

Variable |

Observations |

25% |

Mean |

75% |

Standard |

Minimum |

Maximum |

|---|---|---|---|---|---|---|---|

|

SDG |

572 |

0.00 |

6.00 |

11.00 |

5.64 |

0.00 |

17.00 |

|

REPUT |

572 |

43.76 |

55.50 |

70.92 |

21.41 |

1.75 |

96.02 |

|

BSIZE |

572 |

9.00 |

11.26 |

13.00 |

2.70 |

4.00 |

20.00 |

|

BDIVER |

572 |

23.08 |

30.64 |

37.17 |

12.36 |

0.00 |

75.00 |

|

BSKILL |

572 |

1.00 |

0.99 |

1.00 |

0.09 |

0.00 |

1.00 |

|

BTENU |

572 |

5.24 |

7.23 |

9.25 |

2.85 |

0.25 |

17.63 |

|

BINDEP |

572 |

55.56 |

63.74 |

75.0 |

13.44 |

16.67 |

100.00 |

|

FSIZE |

572 |

8.81 |

9.29 |

9.69 |

0.70 |

7.70 |

11.24 |

|

ROA |

572 |

0.01 |

0.05 |

0.08 |

0.08 |

-0.62 |

0.42 |

|

MCAP |

572 |

8.47 |

8.90 |

9.47 |

0.76 |

6.94 |

10.58 |

|

LEVER |

572 |

0.43 |

0.57 |

0.75 |

0.22 |

0.00 |

1.19 |

|

INDUS |

572 |

0.00 |

0.30 |

1.00 |

0.46 |

0.00 |

1.00 |

|

CSREP |

572 |

1.00 |

0.90 |

1.00 |

0.29 |

0.00 |

1.00 |

Note. Based on statistical software outputs.

Regarding board composition, the average board size is 11.26 members, with the smallest board comprising 4 members and the largest consisting of 20 members. Women make up 30% of board members, with the highest representation reaching 75%. Additionally, 99% of board members possess expertise in finance. The average tenure of individual board members is 7.23 years. Furthermore, 63.74% of board members are considered independent, meaning they are not affiliated with the company’s management.

Regarding the control variables, the average company size is 9.29, with an average Return on Assets (ROA) of 0.05, an average market capitalization of 8.90, and an average financial leverage of 0.57. The minimum and maximum values for these variables show limited variation, suggesting that the companies in the sample are relatively similar in terms of size and financial performance. Additionally, 30% of the sample operates in environmentally sensitive sectors, and 90% of the companies publish an annual environmental report.

Table 4 presents the correlation matrix. The correlation coefficients between the variables are generally moderate to weak. While these coefficients do not suggest multicollinearity among the variables, a VIF analysis was conducted to further confirm the absence of this issue.

Table 4

Correlation Matrix

|

Variable |

(1) |

(2) |

(3) |

(4) |

(5) |

(6) |

(7) |

(8) |

(9) |

(10) |

(11) |

(12) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

(1) SDG |

1.00 |

|||||||||||

|

(2) REPUT |

0.38*** |

1.00 |

||||||||||

|

(3) BSIZE |

0.20*** |

0.35*** |

1.00 |

|||||||||

|

(4) BDIVER |

0.20*** |

0.30*** |

0.09** |

1.00 |

||||||||

|

(5) BSKILL |

0.09** |

-0.00 |

0.00 |

0.11*** |

1.00 |

|||||||

|

(6) BTENU |

-0.21*** |

-0.21*** |

-0.08** |

-0.27*** |

0.01 |

1.00 |

||||||

|

(7) BINDEP |

0.26*** |

0.29*** |

0.05 |

0.25*** |

0.10** |

-0.12*** |

1.00 |

|||||

|

(8) FSIZE |

0.27*** |

0.46*** |

0.64*** |

0.06 |

-0.01 |

-0.14*** |

0.15*** |

1.00 |

||||

|

(9) ROA |

0.00 |

0.16*** |

0.02 |

0.11*** |

-0.00 |

0.13*** |

-0.07** |

-0.08** |

1.00 |

|||

|

(10) MCAP |

0.30*** |

0.50*** |

0.52*** |

0.10** |

-0.01 |

-0.01 |

0.13*** |

0.74*** |

0.26*** |

1.00 |

||

|

(11) LEVER |

-0.01 |

0.24*** |

0.15*** |

0.10** |

0.00 |

-0.20*** |

0.09*** |

0.37*** |

-0.32*** |

0.06 |

1.00 |

|

|

(12) INDUS |

0.11*** |

0.06* |

-0.13*** |

-0.00 |

0.02 |

-0.12*** |

0.03 |

-0.16*** |

0.03 |

-0.19*** |

-0.17*** |

1.00 |

|

(13) CSREP |

0.29*** |

0.52*** |

0.18*** |

0.24*** |

-0.03 |

-0.19*** |

0.15** |

0.25*** |

0.02 |

0.29*** |

0.32*** |

0.05 |

Note. ***p<0.01. **p<0.05. *p<0.10. Based on statistical software outputs.

4.2 Symmetric Analysis: Panel Data

Table 5 presents the results of the estimation for the research models. Models 1 through 5 illustrate the impact of board composition on SDG adoption, while Model 6 examines the effect of SDG adoption on social reputation. T-statistics are reported in brackets.

Table5

Multivariate Analysis

|

Variable |

Model 1 |

Model 2 |

Model 3 |

Model 4 |

Model 5 |

Model 6 |

|---|---|---|---|---|---|---|

|

BSIZE |

0.08 [0.88] |

|||||

|

BDIVER |

0.03** [2.15] |

|||||

|

BSKILL |

4.26** [2.04] |

|||||

|

BTENU |

-0.31*** [-4.52] |

|||||

|

BINDEP |

0.06*** [4.33] |

|||||

|

SDG |

0.77*** [5.49] |

|||||

|

FSIZE |

1.18** [2.12] |

1.41*** [2.82] |

1.41*** [2.82] |

1.16*** [2.35] |

1.33*** [2.69] |

4.95*** [2.92] |

|

ROA |

-1.99 [-0.75] |

-2.69 [-1.00] |

-1.93 [-0.73] |

-1.27 [-0.49] |

-1.04*** [-0.40] |

38.37*** [4.30] |

|

MCAP |

1.22*** [2.62] |

1.21*** [2.61] |

1.21*** [2.60] |

1.38*** [2.99] |

1.11*** [2.42] |

5.52*** [3.50] |

|

LEVER |

-2.92*** [-2.66] |

-3.23*** [-2.95] |

-3.10*** [-2.84] |

-3.44*** [-3.18] |

-3.14*** [-2.92] |

12.86*** [3.49] |

|

INDUS |

1.79*** [4.02] |

1.77*** [4.01] |

1.74*** [3.92] |

1.49*** [3.38] |

1.65*** [3.76] |

4.98*** [3.30] |

|

CSREP |

3.52*** [4.61] |

3.28*** [4.25] |

3.63*** [4.77] |

3.10*** [4.10] |

3.31*** [4.39] |

23.00*** [8.83] |

|

Observations |

572 |

572 |

572 |

572 |

572 |

572 |

|

F (prob > F) |

19.55*** |

20.23*** |

20.15*** |

23.03*** |

22.74*** |

74.82*** |

|

R² |

0.1967 |

0.2022 |

0.2015 |

0.2239 |

0.2217 |

0.4837 |

|

VIF |

2.09 |

1.90 |

1.88 |

1.91 |

1.89 |

1.94 |

|

Breusch-Pagan test |

6.36 |

3.77 |

7.48 |

7.89 |

6.45 |

0.67 |

|

Endogenous regressors |

No |

No |

No |

No |

No |

No |

Note. ***p<0.01. **p<0.05. *p<0.10. Based on statistical software outputs.

The results reveal that board size does not significantly influence SDG adoption among South African companies. However, board diversity has a positive impact on SDG adoption, suggesting that a higher representation of women on the board contributes to greater commitment to the SDGs. Additionally, directors’ skills also have a positive effect on SDG adoption. On the other hand, board tenure shows a negative effect on SDG adoption, indicating that companies with shorter director tenure tend to adopt SDGs more readily. Furthermore, independent directors have a positive influence on SDG adoption. Finally, the findings demonstrate that SDG adoption positively affects corporate social reputation.

Regarding control variables, firm size and market capitalization positively influence both SDG adoption and corporate reputation. Financial leverage, however, negatively impacts SDG adoption but has a positive effect on corporate reputation. The data also indicate that companies in environmentally sensitive industries are more likely to adopt the SDGs and achieve a higher social reputation. Furthermore, companies that publish an environmental report tend to demonstrate greater SDG adoption and a stronger reputation.

Table 6 presents Models 7 to 12, which exclude financial companies due to their adherence to a different regulatory framework.

Table 6

Results Excluding Financial Companies

|

Variable |

Model 7 |

Model 8 |

Model 9 |

Model 10 |

Model 11 |

Model 12 |

|---|---|---|---|---|---|---|

|

BSIZE |

0.13 [1.26] |

|||||

|

BDIVER |

0.05** [2.72] |

|||||

|

BSKILL |

4.17*** [1.75] |

|||||

|

BTENU |

-0.33*** [-4.24] |

|||||

|

BINDEP |

0.06*** [3.95] |

|||||

|

SDG |

0.67*** [4.37] |

|||||

|

FSIZE |

1.53** [2.14] |

1.85*** [2.74] |

1.83*** [2.69] |

1.59*** [2.37] |

1.82*** [2.72] |

4.06* [1.76] |

|

ROA |

-1.07 [-0.37] |

-1.93 [-0.67] |

-1.06 [-0.37] |

-0.09 [-0.03] |

0.31*** [0.11] |

35.05*** [3.61] |

|

MCAP |

1.12*** [2.07] |

1.06** [1.96] |

1.12** [2.07] |

1.24** [2.32] |

0.85* [1.58] |

7.83*** [4.26] |

|

LEVER |

-1.82*** [-1.38] |

-2.18* [-1.69] |

-2.13* [-1.65] |

-2.44** [-1.91] |

-2.27* [-1.77] |

15.18*** [3.46] |

|

INDUS |

1.59*** [3.42] |

1.57*** [3.39] |

1.53*** [3.30] |

1.31*** [2.84] |

1.45*** [3.15] |

4.63*** [2.92] |

|

CSREP |

2.76*** [3.07] |

2.38*** [2.63] |

2.79*** [3.10] |

2.27*** [2.55] |

2.59*** [2.91] |

20.57*** [6.72] |

|

Observations |

479 |

479 |

479 |

479 |

479 |

479 |

|

F (prob > F) |

13.41*** |

14.39*** |

13.66*** |

16.20*** |

15.80*** |

43.62*** |

|

R² |

0.1673 |

0.1775 |

0.1699 |

0.1954 |

0.1915 |

0.3954 |

|

VIF |

1.82 |

1.73 |

1.71 |

1.73 |

1.74 |

1.76 |

|

Breusch-Pagan test |

3.60 |

1.52 |

4.95 |

5.73 |

4.27 |

0.03 |

|

Endogenous regressors |

No |

No |

No |

No |

No |

No |

Note. ***p<0.01. **p<0.05. *p<0.10. Based on statistical software outputs.

Even after adjusting the sample size, the results remained consistent. Among the five variables related to board composition, four were found to be significant. Gender diversity, board skills, and independence all had a positive impact on the adoption of the SDGs. In contrast, the tenure variable continued to exert a negative influence on SDG adoption. Additionally, the adoption of the SDGs by South African companies has enhanced their social reputation.

4.3 Asymmetric Analysis: fsQCA

Table 7

Configurational Analysis

|

Condition |

Path 1 |

Path 2 |

Path 3 |

Path 4 |

Path 5 |

Path 6 |

Path 7 |

|---|---|---|---|---|---|---|---|

|

Outcome |

SDG |

SDG |

SDG |

SDG |

REPUT |

REPUT |

REPUT |

|

BSIZE |

△ |

△ |

|||||

|

BDIVER |

△ |

△ |

● |

||||

|

BSKILL |

● |

△ |

● |

△ |

|||

|

BTENU |

△ |

△ |

△ |

△ |

|||

|

BINDEP |

△ |

|

△ |

△ |

|||

|

SDG |

● |

|

|||||

|

FSIZE |

△ |

△ |

△ |

△ |

△ |

△ |

|

|

ROA |

● |

● |

● |

● |

● |

● |

|

|

MCAP |

△ |

△ |

△ |

△ |

△ |

△ |

△ |

|

LEVER |

● |

△ |

△ |

△ |

|||

|

INDUS |

● |

△ |

△ |

● |

|||

|

CSREP |

△ |

● |

△ |

△ |

|||

|

Raw coverage |

0.72 |

0.44 |

0.04 |

0.35 |

0.66 |

0.35 |

0.85 |

|

Unique coverage |

0.00 |

0.06 |

0.00 |

0.00 |

0.01 |

0.01 |

0.18 |

|

Consistency |

0.90 |

0.80 |

0.95 |

1.00 |

1.00 |

1.00 |

1.00 |

|

Solution coverage |

0.92 |

0.94 |

|||||

|

Solution consistency |

0.72 |

1.00 |

Note. ● = core causal condition (present); △ = core causal condition (absent). Based on statistical software outputs.

The analysis identifies four pathways to enhance SDG adoption and three distinct pathways to improve corporate reputation. The data reveal that gender diversity, board skills, and board independence are core causal factors for SDG adoption. In contrast, board size and tenure are absent conditions, suggesting they do not play a direct role in driving SDG adoption. Additionally, ROA is a core causal factor in all pathways, while leverage, industry, and CSR reporting serve as core conditions in specific pathways for enhanced SDG adoption.

To enhance corporate social reputation, companies should adopt the SDGs, as this variable is a core causal factor. Additionally, the findings indicate that ROA and industry are other key drivers of social reputation.

Therefore, after symmetric analysis (multivariate analysis) and asymmetric analysis (fsQCA), the results allow us to confirm that three board characteristics affect the adoption of the SDGs: gender diversity, board skills, and board independence. Furthermore, the findings allow us to understand that the adoption of the SDGs increases corporate social reputation. Therefore, we confirm Hypotheses 2, 3, 5, and 6.

5. Discussion

The study shows that board size does not significantly affect SDG adoption, so hypothesis H1 was not supported. This contradicts previous literature that found a positive relationship (Buniamin et al., 2022; Kwarteng et al., 2023; Pinheiro, Ribeiro, et al., 2024; Taglialatela et al., 2023). Gutiérrez-Ponce and Wibowo (2023) also found no link between board size and SDG disclosure in Indonesian companies, suggesting that the board’s role is limited to policy-making rather than implementation.

Concerning the impact of board gender diversity, our results confirm H2 and are in line with previous studies (Rosati & Faria, 2019; Taglialatela et al., 2023). This implies that boards with greater female representation are more likely to adopt the SDGs. In South African companies, it was found that, on average, 30% of board members are women. This equates to approximately three women on each board, as most of the companies included in this study have around eleven board members. This suggests that women are underrepresented in positions of power in companies in this country, leading to low diversity on boards. There is significant potential for improvement, as increasing gender diversity on boards would positively impact the 2030 Agenda, particularly SDG 5.5 (ensure women’s full and effective participation and equal opportunities for leadership at all levels of decision-making in political, economic, and public life), by reducing gender inequality in the region.

Regarding H3, the findings show that the association between a board’s financial background and SDG adoption is positive and significant in South Africa. The results are in line with Al Lawati and Alshabibi (2023) and Githaiga and Kosgei (2023). Given the limited research linking board financial qualifications to SDG adoption, this study contributes to the literature by highlighting a positive association between these variables. Further research is needed to confirm the importance of board financial expertise in different contexts.

Regarding H4, the findings show a significant negative association between directors serving on the board for more than five years and SDG adoption, leading to the rejection of H4. Gavana et al. (2024) suggest that, from an agency theory perspective, low director turnover may lead to entrenchment and reduced monitoring, as long-tenured directors are more likely to form close relationships with the CEO (Ji et al., 2021). Furthermore, directors with long tenures may lead to conformity and a tendency to avoid conflicts, which can compromise effective decision-making (Gallego-Álvarez & Rodriguez-Dominguez, 2023) and may prioritize short-term reputation over long-term value (Cahyono et al., 2023).

Regarding H5, the results confirm it, meaning that a greater number of independent directors on the board positively impacts SDG adoption in South Africa. This finding supports theoretical claims that, from an agency theory perspective, independent directors influence CSR investment choices (Jizi, 2017). Independent directors, being responsible to a broader range of stakeholders, can exert more pressure on firms’ sustainability performance (Kwarteng et al., 2023). They have been successful in promoting the 2030 Agenda in South African companies, which aligns with prior studies (Al Lawati & Alshabibi, 2023; Pinheiro, Lopes, et al., 2024).

Finally, our results confirm H6, meaning that companies adopting the SDGs tend to improve their image and reputation with stakeholders, such as consumers, investors, and other interested groups, in the South African context. In this sense, if a company unexpectedly takes extra steps in providing living wages, supporting marginalized communities, or adopting innovative sustainability measures that far exceed what stakeholders expected, this can positively impact its reputation and build stronger loyalty (Lin-Hi & Blumberg, 2018; Singla & Singh, 2024). Therefore, through a solid theoretical foundation based on the stakeholder theory, it was possible to confirm the link between SDG adoption and corporate reputation. In other words, from a stakeholder theory perspective, SDG adoption functions not only as a sustainability governance mechanism but also as a reputational signal that reflects the firm’s ability to meet evolving stakeholder expectations.

5.1 Contribution to Literature and Practice

Our results contribute to agency theory by highlighting how board characteristics, such as gender diversity, board skills, and board independence, influence the adoption of the SDGs. Agency theory focuses on the relationship between principals (shareholders) and agents (managers), with the goal of aligning the interests of both parties to reduce agency costs.

By demonstrating that diverse and skilled boards (along with independent directors) play a key role in adopting SDGs, the findings highlight the governance conditions that support corporate sustainability initiatives. However, the alignment of these sustainability initiatives with shareholder interests may depend on the composition and preferences of investors, as short-term-oriented shareholders might prioritize financial returns over sustainability outcomes. The presence of diverse perspectives on the board can reduce conflicts and enhance decision-making, which in turn strengthens governance and contributes to better alignment between managerial actions and stakeholder expectations.

The finding that the adoption of the SDGs increases corporate social reputation contributes to and confirms the stakeholder theory by demonstrating that companies that align their practices with the SDGs can meet or exceed stakeholders’ expectations. According to stakeholder theory, when an organization’s actions either meet or surpass the expectations of its stakeholders, it leads to positive outcomes, such as enhanced reputation or trust.

In this context, the adoption of the SDGs serves as a way for companies to signal their commitment to sustainability, ethical practices, and social responsibility – key expectations that stakeholders have. When companies align with these expectations and deliver on their sustainability promises, they fulfill stakeholder anticipations, leading to an increase in their social reputation.

On a practical level, managers can leverage these findings to optimize their board compositions and better align corporate strategies with sustainable development goals. Recognizing that gender diversity, board skills, and independence positively influence SDG adoption can lead to more informed decisions about recruitment and board development.

Since the findings show that adopting SDGs increases corporate social reputation, managers should recognize that meeting or exceeding stakeholder expectations, especially around sustainability, can lead to higher levels of trust and loyalty. This can be especially valuable in industries where reputation and public perception are crucial for success.

In South Africa, governments or regulatory bodies might promote best practices in corporate governance by advising or mandating the inclusion of diverse skill sets and independent perspectives on boards, thereby improving corporate responsibility and sustainability efforts. Given the importance of adopting the SDGs in South Africa, governments can offer tax incentives, deductions, or subsidies to companies that implement sustainable practices or meet specific SDG-related targets (e.g., reducing carbon emissions, implementing renewable energy solutions, supporting local communities, or reducing poverty and illiteracy).

6. Conclusion

The purpose of this article was to understand the motivations underlying South African companies’ adoption of the UN Sustainable Development Goals and to assess the implications of this decision. In conclusion, both symmetric (multivariate analysis) and asymmetric (fsQCA) analyses provide strong evidence that three key board characteristics (gender diversity, board skills, and board independence) significantly influence the adoption of the SDGs. Additionally, the findings demonstrate that SDG adoption contributes to enhanced corporate social reputation. These findings have significant implications for agency theory and stakeholder theory, as well as for both managers and governments.

As with all research, this study has limitations that should be considered when interpreting the findings. For instance, the focus on South African companies may not fully reflect the dynamics in other regions with different regulatory, cultural, or economic environments. The data used in the study may not account for all possible variables that influence SDG adoption and corporate reputation. Another limitation is that our study measures the adoption of the SDGs rather than the quality or effectiveness of the actions implemented by the firms.

Future research could explore additional board characteristics, such as directors’ nationality and ethnicity, CEO duality, and CEO narcissism, to further understand their impact on SDG adoption. Adopting a mixed-methods approach, incorporating alternative measures, and applying psychological theory could further advance research in this field. Multinational studies could also be conducted, incorporating institutional variables to offer a broader perspective on SDG adoption and corporate social reputation.

References

Adetoro, A. A., Ngidi, M. S. C., & Danso-Abbeam, G. (2023). Towards the global zero poverty agenda: Examining the multidimensional poverty situation in South Africa. SN Social Sciences, 3(9), 148. https://doi.org/10.1007/s43545-023-00735-2

Ahmad, N. B. J., Rashid, A., & Gow, J. (2018). Corporate board gender diversity and corporate social responsibility reporting in Malaysia. Gender, Technology and Development, 22(2), 87–108. https://doi.org/10.1080/09718524.2018.1496671

Akanle, O., Kayode, D., & Abolade, I. (2022). Sustainable development goals (SDGs) and remittances in Africa. Cogent Social Sciences, 8(1). https://doi.org/10.1080/23311886.2022.2037811

Al Lawati, H., & Alshabibi, B. (2023). Does board structure drive Sustainable Development Goals disclosure? Evidence from an emerging market. Journal of Governance and Regulation, 12(2), 166–175. https://doi.org/10.22495/jgrv12i2art15

Al Lawati, H., & Hussainey, K. (2022). Does Sustainable Development Goals Disclosure Affect Corporate Financial Performance? Sustainability, 14(13), 7815. https://doi.org/10.3390/su14137815

Al-Qudah, A. A., & Houcine, A. (2024). Firms’ characteristics, corporate governance, and the adoption of sustainability reporting: Evidence from Gulf Cooperation Council countries. Journal of Financial Reporting and Accounting, 22(2), 392–415. https://doi.org/10.1108/JFRA-02-2023-0066

Arumona, J., Erin, O., Onmonya, L., & Omotayo, V. (2019). Board financial education and firm performance: Evidence from the healthcare sector in Nigeria. Academy of Strategic Management Journal, 18(4), 1–14.

Awa, H.O., Etim, W. & Ogbonda, E. (2024). Stakeholders, stakeholder theory and Corporate Social Responsibility (CSR). International Journal of Corporate Social Responsibility, 9, 11. https://doi.org/10.1186/s40991-024-00094-y

Bose, S., & Khan, H. Z. (2022). Sustainable development goals (SDGs) reporting and the role of country-level institutional factors: An international evidence. Journal of Cleaner Production, 335, 130290. https://doi.org/10.1016/j.jclepro.2021.130290

Bose, S., Khan, H. Z., & Bakshi, S. (2024). Determinants and consequences of sustainable development goals disclosure: International evidence. Journal of Cleaner Production, 434, 140021. https://doi.org/10.1016/j.jclepro.2023.140021

Buniamin, S., Jaffar, R., Ahmad, N., & Johari, N. H. (2022). The Role of Corporate Governance in Achieving SDGs among Malaysian Companies. European Journal of Sustainable Development, 11(3), 326. https://doi.org/10.14207/ejsd.2022.v11n3p326

Cahyono, S., Harymawan, I., & Kamarudin, K. A. (2023). The impacts of tenure diversity on boardroom and corporate carbon emission performance: Exploring from the moderating role of corporate innovation. Corporate Social Responsibility and Environmental Management, 30(5), 2507–2535. https://doi.org/10.1002/csr.2500

Crane, A., & Ruebottom, T. (2011). Stakeholder Theory and Social Identity: Rethinking Stakeholder Identification. Journal of Business Ethics, 102, 77–87 (2011). https://doi.org/10.1007/s10551-011-1191-4

Cuadrado‐Ballesteros, B., Martínez‐Ferrero, J., & García‐Sánchez, I. M. (2017). Board Structure to Enhance Social Responsibility Development: A Qualitative Comparative Analysis of US Companies. Corporate Social Responsibility and Environmental Management, 24(6), 524–542. https://doi.org/10.1002/csr.1425

de Villiers, C., Naiker, V., & van Staden, C. J. (2011). The Effect of Board Characteristics on Firm Environmental Performance. Journal of Management, 37(6), 1636–1663. https://doi.org/10.1177/0149206311411506

Emma, G.-M., & Jennifer, M.-F. (2021). Is SDG reporting substantial or symbolic? An examination of controversial and environmentally sensitive industries. Journal of Cleaner Production, 298, 126781. https://doi.org/10.1016/j.jclepro.2021.126781

Fama, E. F., & Jensen, M. C. (1983). Separation of Ownership and Control. The Journal of Law and Economics, 26(2), 301–325. https://doi.org/10.1086/467037

Ferrero-Ferrero, I., Muñoz-Torres, M. J., Rivera-Lirio, J. M., Escrig-Olmedo, E., & Fernández-Izquierdo, M. Á. (2023). SDG reporting: An analysis of corporate sustainability leaders. Marketing Intelligence & Planning, 41(4), 457–472. https://doi.org/10.1108/MIP-07-2022-0332

Freeman, R. E. (1984). Strategic management: A stakeholder approach. Pittman, Boston.

Gallego-Álvarez, I., & Rodriguez-Dominguez, L. (2023). Board of directors and environmental practices: the effect of board experience, culture, and tenure. Environment, Development and Sustainability. https://doi.org/10.1007/s10668-023-03937-z

García Martín, C. J., & Herrero, B. (2020). Do board characteristics affect environmental performance? A study of EU firms. Corporate Social Responsibility and Environmental Management, 27(1), 74–94. https://doi.org/10.1002/csr.1775

García-Sánchez, I.-M., Raimo, N., Vitolla, F., & Aibar-Guzmán, B. (2025). Does human-oriented governance foster labor and human rights disclosure? Review of Managerial Science. https://doi.org/10.1007/s11846-025-00843-8

Gavana, G., Gottardo, P., & Moisello, A. M. (2024). The impact of board gender diversity on ESG disclosure. A contingency perspective. Meditari Accountancy Research, 33(7), 1–29. https://doi.org/10.1108/MEDAR-07-2024-2567

Gilbert, D. U., & Rasche, A. (2008). Opportunities and Problems of Standardized Ethics Initiatives – a Stakeholder Theory Perspective. Journal of Business Ethics, 82, 755–773. https://doi.org/10.1007/s10551-007-9591-1

Githaiga, P. N., & Kosgei, J. K. (2023). Board characteristics and sustainability reporting: a case of listed firms in East Africa. Corporate Governance: The International Journal of Business in Society, 23(1), 3–17. https://doi.org/10.1108/CG-12-2021-0449

Gutiérrez-Ponce, H., & Wibowo, S. A. (2023). Sustainability Reports and Disclosure of the Sustainable Development Goals (SDGs): Evidence from Indonesian Listed Companies. Sustainability, 15(24), 16919. https://doi.org/10.3390/su152416919

Hair Jr, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2019). Multivariate Data Analysis (8th ed.). Cengage Learning.

Haniffa, R. M., & Cooke, T. E. (2002). Culture, Corporate Governance and Disclosure in Malaysian Corporations. Abacus, 38(3), 317–349. https://doi.org/10.1111/1467-6281.00112

Haywood, L. K., & Boihang, M. (2021). Business and the SDGs: Examining the early disclosure of the SDGs in annual reports. Development Southern Africa, 38(2), 175–188. https://doi.org/10.1080/0376835X.2020.1818548

Hossain, M., Atif, M., Ahmed, A., & Mia, L. (2020). Do LGBT Workplace Diversity Policies Create Value for Firms?. Journal of Business Ethics, 167, 775–791 (2020). https://doi.org/10.1007/s10551-019-04158-z

Isaacs, G., & Kaltenbrunner, A. (2018). Financialization and liberalization: South Africa’s new forms of external vulnerability. Competition & Change, 22(4), 437–463. https://doi.org/10.1177/1024529418788375

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

Ji, J., Peng, H., Sun, H., & Xu, H. (2021). Board tenure diversity, culture and firm risk: Cross-country evidence. Journal of International Financial Markets, Institutions and Money, 70, 101276. https://doi.org/10.1016/j.intfin.2020.101276

Jiang, Y., García-Meca, E., & Martinez-Ferrero, J. (2023). Do board and ownership factors affect Chinese companies in reporting sustainability development goals? Management Decision, 61(12), 3806–3834. https://doi.org/10.1108/MD-01-2023-0113

Jizi, M. (2017). The Influence of Board Composition on Sustainable Development Disclosure. Business Strategy and the Environment, 26(5), 640–655. https://doi.org/10.1002/bse.1943

Katmon, N., Mohamad, Z. Z., Norwani, N. M., & Farooque, O. Al. (2019). Comprehensive Board Diversity and Quality of Corporate Social Responsibility Disclosure: Evidence from an Emerging Market. Journal of Business Ethics, 157(2), 447–481. https://doi.org/10.1007/s10551-017-3672-6

Kayikci, Y., Kazancoglu, Y., Gozacan-Chase, N., & Lafci, C. (2022). Analyzing the drivers of smart sustainable circular supply chain for sustainable development goals through stakeholder theory. Business Strategy and the Environment, 31(7), 3335–3353. https://doi.org/10.1002/bse.3087

Kumar, S., Sahoo, S., Lim, W. M., Kraus, S., & Bamel, U. (2022). Fuzzy-set qualitative comparative analysis (fsQCA) in business and management research: A contemporary overview. Technological Forecasting and Social Change, 178, 121599. https://doi.org/10.1016/j.techfore.2022.121599

Kwarteng, P., Appiah, K. O., & Addai, B. (2023). Influence of board mechanisms on sustainability performance for listed firms in Sub-Saharan Africa. Future Business Journal, 9(1), 85. https://doi.org/10.1186/s43093-023-00258-5

Lin, H., Zeng, S., Wang, L., Zou, H., & Ma, H. (2016). How Does Environmental Irresponsibility Impair Corporate Reputation? A Multi‐Method Investigation. Corporate Social Responsibility and Environmental Management, 23(6), 413–423. https://doi.org/10.1002/csr.1387

Lin-Hi, N., & Blumberg, I. (2018). The Link Between (Not) Practicing CSR and Corporate Reputation: Psychological Foundations and Managerial Implications. Journal of Business Ethics, 150(1), 185–198. https://doi.org/10.1007/s10551-016-3164-0

Martínez-Ferrero, J., & García-Meca, E. (2020). Internal corporate governance strength as a mechanism for achieving sustainable development goals. Sustainable Development, 28(5), 1189–1198. https://doi.org/10.1002/sd.2068

Michelon, G., & Parbonetti, A. (2012). The effect of corporate governance on sustainability disclosure. Journal of Management and Governance, 16(3), 477–509. https://doi.org/10.1007/s10997-010-9160-3

Mthembu, D. E., & Nhamo, G. (2021). Domestication of the UN Sustainable Development Goals in South Africa. South African Journal of International Affairs, 28(1), 1–28. https://doi.org/10.1080/10220461.2021.1894971

Naheed, R., AlHares, A., Shahab, Y., & Naheed, R. (2021). Board’s financial expertise and corporate social responsibility disclosure in China. Corporate Governance: The International Journal of Business in Society, 21(4), 716–736. https://doi.org/10.1108/CG-08-2020-0329

Padungsaksawasdi, C., & Treepongkaruna, S. (2024). Corporate social responsibility, board characteristics, and family business in Thailand. Corporate Social Responsibility and Environmental Management, 31(2), 1340–1353. https://doi.org/10.1002/csr.2636

Pajuelo-Moreno, M. L., Barroso-Méndez, M. J., & Gallardo-Vázquez, D. (2024). Relationship between sustainability disclosure and corporate reputation: Evidence from a meta-analysis. Business Strategy and the Environment, 33(8), 8593–8615. https://doi.org/10.1002/bse.3933

Pinheiro, A. B., do Prado, N. B., Moraes, G. H. S. M. D., & Carraro, W. B. W. H. (2024). Corporate reputation in Brazil: Do board characteristics matter?. RAUSP Management Journal, 59(4), 350-365.

Pinheiro, A. B., Lopes, C., Teles, N., Rocha, R., Galleli, B., & Cunha, S. (2024). Sustainable Development Goals and Board Structure: Connecting the Dots in The Energy Sector. Revista de Gestão Social e Ambiental, 18(1), e04855. https://doi.org/10.24857/rgsa.v18n1-087

Pinheiro, A. B., Ribeiro, C. de M. de A., & Bizerra, A. L. V. (2024). Board structure as a mechanism to achieve the UN 2030 Agenda in Latin America. Cadernos EBAPE.BR, 22(1). https://doi.org/10.1590/1679-395120220308x

Pizzi, S., Rosati, F., & Venturelli, A. (2021). The determinants of business contribution to the 2030 Agenda: Introducing the SDG Reporting Score. Business Strategy and the Environment, 30(1), 404–421. https://doi.org/10.1002/bse.2628

Quintana-García, C., Benavides-Chicón, C. G., & Marchante-Lara, M. (2021). Does a green supply chain improve corporate reputation? Empirical evidence from European manufacturing sectors. Industrial Marketing Management, 92, 344–353. https://doi.org/10.1016/j.indmarman.2019.12.011

Ragin, C. C. (1987). The Comparative Method: Moving beyond Qualitative and Quantitative Strategies. University of CA Press.

Rosati, F., & Faria, L. G. D. (2019). Business contribution to the Sustainable Development Agenda: Organizational factors related to early adoption of SDG reporting. Corporate Social Responsibility and Environmental Management, 26(3), 588–597. https://doi.org/10.1002/csr.1705

Russo, A., & Perrini, F. (2010). Investigating Stakeholder Theory and Social Capital: CSR in Large Firms and SMEs. Journal of Business Ethics, 91, 207–221. https://doi.org/10.1007/s10551-009-0079-z

SDG Center for Africa. (2020). Africa SDG Index and Dashboards Report 2020.

Sekarlangit, L., & Wardhani, R. (2021). The Effect of the Characteristics and Activities of the Board of Directors on Sustainable Development Goal (SDG) Disclosures: Empirical Evidence from Southeast Asia. Sustainability (Switzerland), 13, 8007. https://doi.org/10.1108/SRJ-09-2021-0373

Singhal, N. (2023). Stakeholders sustainable development goals (SDGs) prioritization. Business Strategy & Development, 6(4), 986–990. https://doi.org/10.1002/bsd2.292

Singla, H., & Singh, V. (2024). Voluntary Disclosures and their Drivers: A Study of MDA Reports in India. Organizations and Markets in Emerging Economies, 15(1-30), 127–145. https://doi.org/10.15388/omee.2024.15.7

Subramaniam, N., Akbar, S., Situ, H., Ji, S., & Parikh, N. (2023). Sustainable development goal reporting: Contrasting effects of institutional and organisational factors. Journal of Cleaner Production, 411, 137339. https://doi.org/10.1016/j.jclepro.2023.137339

Taglialatela, J., Pirazzi Maffiola, K., Barontini, R., & Testa, F. (2023). Board of Directors’ characteristics and environmental SDGs adoption: an international study. Corporate Social Responsibility and Environmental Management, 30(5), 2490–2506. https://doi.org/10.1002/csr.2499

UN General Assembly. (2015). Transforming Our world: The 2030 Agenda For Sustainable Development.