Organizations and Markets in Emerging Economies ISSN 2029-4581 eISSN 2345-0037

2026, vol. 17, no. 1(34), pp. 140–169 DOI: https://doi.org/10.15388/omee.2026.17.7

Corporate Venture Capital and Sport-Tech Enterprises: Innovation and Internationalization in an Emerging Economy Context

Dittachai Chankuna

Thailand National Sports University Chiang Mai Campus, Thailand

c.dittachai@tnsu.ac.th

Abstract. This study examines how different orientations of corporate venture capital (CVC) investment are associated with the strategic development of sport-tech firms in an emerging economy context. Using a longitudinal dataset of 48 Thai sport-tech firms and 73 CVC transactions between 2005 and 2025, the analysis focuses on two strategic outcomes: technology portfolio diversification and international market expansion. The results indicate that technology-oriented CVC is positively associated with broader technology portfolios, while foreign-oriented CVC is positively associated with wider geographic market presence. At the same time, the findings show that the strength of these relationships varies depending on the level of industry and cultural distance between investors and portfolio firms, suggesting that contextual compatibility influences the effectiveness of investment partnerships. The study adopts a mechanism-focused perspective that examines how strategic investment relationships may facilitate knowledge transfer and market access within CVC-backed firms. By applying the interorganizational learning framework to the sport-tech sector, the research extends existing corporate venture capital literature to an underexplored industry within an emerging economy context. The findings also provide practical insights for entrepreneurs, corporate investors, and policymakers seeking to leverage corporate venture capital as both a financial and strategic resource for innovation and international market participation.

Keywords: international investment, international business administration, corporate culture, sport-tech firms

Received: 20/9/2025. Accepted: 28/4/2026

Copyright © 2026 Dittachai Chankuna. Published by Vilnius University Press. This is an Open Access article distributed under the terms of the Creative Commons Attribution Licence, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Introduction

The sport-technology (sport-tech) industry has become a global driver of change in both professional and grassroots sport. It encompasses innovations such as wearable performance devices, immersive fan engagement platforms, analytics software, and esports infrastructure (Ratten, 2020). These innovations are reshaping how athletes prepare, how teams manage performance, and how fans interact with sport. For example, wearable sensors enhance athlete skill development and injury prevention through real-time biomechanical feedback, while video analytics improve team coordination and enrich fan experience (Adesida et al., 2019). Beyond advanced economies, sport-tech is increasingly salient in emerging markets, where it is viewed not only as a sector for economic growth but also as a source of cultural soft power and international visibility (Chankuna, 2024).

Yet, the development trajectories of sport-tech firms in emerging economies differ markedly from those in mature markets. Limited access to early-stage and growth capital, coupled with relatively low absorptive capacity, makes it difficult for many firms to adopt and scale advanced technologies (Lane & Lubatkin, 1998). In addition, international expansion is hindered by regulatory complexity, institutional voids, and weak international networks (Wadhwa & Basu, 2013). These challenges underscore the need for financing models that provide not only capital but also strategic assets to support innovation and market entry.

Corporate venture capital (CVC) represents one such mechanism. Defined as minority equity investments made by established firms in entrepreneurial ventures (Chemmanur et al., 2014), CVC goes beyond traditional venture capital by offering access to distribution networks, R&D facilities, and managerial expertise (Dushnitsky & Lenox, 2005). For firms in resource-constrained environments, these strategic benefits can be as critical as funding itself. From a theoretical perspective, CVC can also function as a platform for interorganizational learning, where collaboration between corporate investors and entrepreneurial firms facilitates the transfer of technological knowledge, managerial practices, and market insights (Schmidt et al., 2025). Recent studies further highlight that corporate venture capital investors can act as knowledge accelerators within global innovation ecosystems by facilitating the diffusion of entrepreneurial knowledge across organizational boundaries (Rossi et al., 2022).

Empirical evidence supports this dual role. Schmidt et al. (2025) found that technology-oriented CVC is associated with product portfolio diversification, while foreign-oriented CVC is associated with geographic expansion. However, both benefits are contingent and can be weakened by industry or cultural distance between investors and investees. This insight is especially relevant for sport-tech firms in emerging markets such as Thailand, where products and services are often culturally embedded (e.g., Muay Thai, esports, and regional sports leagues). Success in such niches requires not only financial capital but also cultural understanding and contextual alignment (Chankuna, 2024).

Despite its significance, the role of CVC in the sport-tech industry remains underexplored. While research has examined manufacturing, biotechnology, and information technology sectors (Dushnitsky & Lenox, 2005; Wadhwa & Basu, 2013), sport-tech in emerging economies has received little systematic analysis. This gap limits our understanding of how CVC contributes to innovation and internationalization in contexts characterized by institutional constraints and cultural distinctiveness. Thailand provides a useful empirical setting for examining these dynamics because it reflects many of the structural challenges faced by sport-tech ecosystems in emerging economies.

This study addresses these gaps by analyzing how CVC investments influence the strategic outcomes of Thai sport-tech firms. Specifically, it examines two pathways—technology portfolio diversification and international market expansion—and assesses how industry and cultural distance condition these relationships. Rather than comparing CVC-backed firms with a control group, the study focuses on examining the mechanisms through which post-investment relationships in CVC-backed firms are associated with strategic change. By doing so, it offers insights that are both context-specific and internationally relevant: highlighting how CVC functions in resource-constrained environments, and drawing lessons for other emerging markets seeking to leverage CVC for innovation-driven growth.

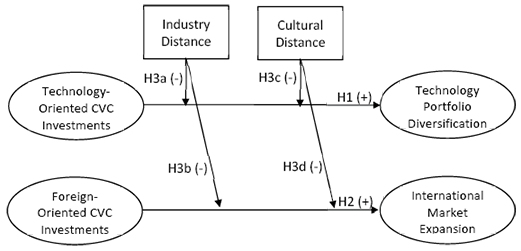

1. Conceptual Framework

This study adopts an interorganizational learning perspective to explain how corporate venture capital (CVC) influences strategic outcomes in Thai sport-tech enterprises. Interorganizational learning theory posits that firms can enhance their competitive advantage by acquiring, assimilating, and integrating external knowledge from their network partners (Lane & Lubatkin, 1998). In the context of CVC, this knowledge transfer occurs through strategic investment relationships, where established corporations provide not only financial resources but also technical expertise, market intelligence, and international networks (Chemmanur et al., 2014). Such investment relationships also facilitate knowledge management processes between corporate investors and entrepreneurial firms, enabling the exchange of both explicit and tacit knowledge that supports innovation and strategic development within venture ecosystems (Rossi et al., 2020). Recent research also emphasizes that corporate venture capital plays an important role within knowledge-based innovation ecosystems, where both independent venture capital (IVC) and corporate venture capital investors contribute to knowledge recombination and entrepreneurial learning across organizational boundaries (Kolte et al., 2025).

The conceptual model is grounded in the empirical findings of Schmidt and colleagues (Schmidt et al., 2025), who identified distinct pathways through which CVC investments contribute to strategic transformation. Specifically, their research demonstrated that technology-oriented CVC investments drive product portfolio diversification, while foreign-oriented CVC investments promote geographic expansion. However, the strength of these relationships depends on the level of industry distance and cultural distance between the investor and the investee, which can either facilitate or hinder effective knowledge transfer.

In adapting this framework to the Thai sport-tech context, the present study proposes that technology-oriented CVC investments will stimulate technology portfolio growth, foreign-oriented CVC investments will foster internationalization, and both industry distance and cultural distance will weaken these relationships.

1.1 Technology-Oriented CVC and Technology Portfolio Growth

Technology-oriented CVC investments are those in which the primary strategic objective is to access new technologies, research capabilities, or innovation pipelines. Such investments allow corporate investors to balance exploration of emerging technologies with exploitation of existing capabilities, creating ambidextrous innovation outcomes (Rossi et al., 2019). In prior corporate venture capital research, such investments are commonly characterized as strategically motivated partnerships through which incumbent firms seek to explore emerging technological domains and complement their existing innovation capabilities (Chemmanur et al., 2014; Dushnitsky & Lenox, 2005). For sport-tech enterprises, these investments can lead to the development of new products, enhancement of existing offerings, and adoption of advanced technologies such as wearable devices, performance analytics software, and fan engagement platforms (Adesida et al., 2019). For example, corporate investors in the digital sport ecosystem may support portfolio companies developing athlete monitoring systems, data-driven coaching platforms, or immersive fan engagement applications, thereby expanding the technological scope of the investee firm. Previous research has shown that such partnerships can improve innovation speed and breadth by providing access to specialized knowledge, technical infrastructure, and complementary technological assets (Dushnitsky & Lenox, 2005).

In Thailand’s sport-tech industry, where many firms have limited internal R&D capacity, technology-oriented CVC can act as a catalyst for innovation. Access to an investor’s technical resources can bridge capability gaps and support the integration of advanced digital tools into product offerings (Chankuna, 2024). From an interorganizational learning perspective, corporate investors can transfer technological knowledge, research expertise, and innovation practices to portfolio companies, enabling them to experiment with new technological domains beyond their original capabilities (Lane & Lubatkin, 1998). Such learning processes may expand the breadth of technologies embedded in the firm’s product offerings, resulting in a more diversified technology portfolio. In this study, technology portfolio diversification refers to the extent to which a firm develops or adopts multiple technological components across different product or service categories within the sport-tech ecosystem. Consistent with Schmidt et al. (2025), this study hypothesizes that technology-oriented CVC is positively related to technology portfolio diversification.

This study focuses on technology portfolio diversification rather than innovation intensity because diversification captures the breadth of technological domains in which a firm operates. In the sport-tech industry, firms often integrate multiple technological components—such as wearable sensing technologies, performance analytics, and digital fan engagement platforms—within their product ecosystems. Therefore, the ability of a firm to expand into multiple technological domains reflects strategic learning and capability expansion resulting from CVC partnerships. Innovation intensity, in contrast, typically measures the volume of innovation outputs within a single technological domain and may not fully capture the cross-domain technological development that characterizes sport-tech ventures.

H1: Technology-oriented CVC investments will be positively related to the diversification of a sport-tech firm’s technology portfolio.

1.2 Foreign-Oriented CVC and Internationalization

Foreign-oriented CVC investments are designed to facilitate entry into new geographic markets and to gain exposure to different customer bases, distribution channels, and regulatory environments (Song et al., 2023). In the corporate venture capital literature, foreign investors often provide portfolio companies with access to international networks, strategic alliances, and market knowledge that may otherwise be difficult for young firms to obtain independently. For sport-tech enterprises in Thailand, such investments can provide the resources and networks needed to expand into competitive international arenas, such as ASEAN markets, East Asia, and Europe. Recent studies examining corporate venture capital investments in Asia-Pacific innovation ecosystems further demonstrate how CVC partnerships can accelerate technological development and entrepreneurial growth across emerging industries (Kolte et al., 2023). Through cross-border investment partnerships and syndication with international venture investors, portfolio companies may gain legitimacy, market intelligence, and distribution channels that facilitate entry into foreign markets.

Internationalization not only increases revenue opportunities but also enhances brand recognition and the firm’s ability to attract additional investment. Research indicates that CVC can accelerate international expansion by reducing market entry risks and shortening the learning curve in unfamiliar environments (Wadhwa & Basu, 2013). In the corporate venture capital literature, foreign investors often provide portfolio companies with access to international networks, strategic alliances, and distribution channels that facilitate entry into foreign markets. Through cross-border venture investment partnerships and syndication with international investors, portfolio companies may gain legitimacy, market intelligence, and access to global commercialization platforms. In this study, international market expansion refers to the geographic diversification of a firm’s activities across multiple foreign markets rather than the intensity of foreign operations within a single market. This conceptualization emphasizes the diversity of international market presence, reflecting the firm’s ability to leverage corporate investment networks to enter different regional ecosystems. From an interorganizational learning perspective, foreign corporate investors can transfer knowledge about international market structures, regulatory environments, and commercialization strategies, enabling portfolio companies to overcome the liability of foreignness and expand their geographic market scope. In line with Schmidt et al. (2025), this study proposes that foreign-oriented CVC investments are positively related to a sport-tech firm’s international market expansion:

H2: Foreign-oriented CVC investments are positively related to the international market expansion of sport-tech firms.

1.3 Moderating Role of Industry Distance and Cultural Distance

Industry distance refers to the degree of difference in the technological base, competitive dynamics, and market logic between the investing firm and the investee (Schmidt et al., 2025). A smaller industry distance generally facilitates knowledge transfer because the two parties share a common technological language, product development processes, and market understanding (Lane & Lubatkin, 1998). From the perspective of absorptive capacity and interorganizational learning, knowledge transfer is more effective when firms operate within technologically related domains, as similarities in expertise and routines enable portfolio companies to recognize, assimilate, and apply external knowledge. Conversely, a large industry distance may hinder the integration of strategic resources, thereby reducing the potential benefits of CVC. When investors originate from industries with substantially different technological bases, portfolio companies may face difficulties translating external knowledge into their own innovation processes.

In Thailand’s sport-tech ecosystem, where investors may come from non-sport-related industries such as telecommunications or consumer electronics, industry distance could limit the effectiveness of collaboration. Although such investors may possess valuable technological assets, large differences in industry logic may create coordination challenges and reduce the efficiency of knowledge transfer between partners. This study therefore hypothesizes that industry distance will weaken the positive relationships between CVC investment orientation and strategic outcomes:

H3a: Industry distance will negatively moderate the relationship between technology-oriented CVC investments and technology portfolio diversification.

H3b: Industry distance will negatively moderate the relationship between foreign-oriented CVC investments and international market expansion.

Additionally, cultural distance describes the extent to which norms, values, and business practices differ between the home countries of the investor and the investee (Kogut & Singh, 1988). High cultural distance can create barriers to effective communication, trust-building, and knowledge sharing (Schmidt et al., 2025). In cross-border investment relationships, differences in managerial practices, communication styles, and institutional expectations may complicate coordination between investors and portfolio companies. In the Thai sport-tech context, where product adoption and marketing are often influenced by cultural preferences and national identity, cultural compatibility can be crucial for successful collaboration.

If the cultural distance is large, the positive impacts of CVC on strategic transformation may be reduced because misunderstandings, mismatched expectations, and adaptation challenges are more likely to arise. These barriers may weaken the ability of portfolio companies to fully utilize the strategic resources provided by corporate investors, thereby limiting the learning benefits of CVC partnerships. Therefore, this study posits the following:

H3c: Cultural distance will negatively moderate the relationship between technology-oriented CVC investments and technology portfolio diversification.

H3d: Cultural distance will negatively moderate the relationship between foreign-oriented CVC investments and international market expansion.

1.4 Conceptual Model

The proposed conceptual model positions CVC investment orientation (technology-oriented and foreign-oriented) as independent variables, strategic transformation outcomes (technology portfolio diversification and international market expansion) as dependent variables, and industry distance and cultural distance as moderators. This framework integrates the interorganizational learning perspective with empirical evidence from CVC research, applying it to the Thai sport-tech context for the first time. Figure 1 summarizes the conceptual model.

Figure 1

Conceptual Model

2. Methodology

This study adopts a quantitative, longitudinal design to assess the effects of corporate venture capital (CVC) on Thai sport-tech firms’ technology innovation and international expansion. The longitudinal approach enables more precise causal analysis by observing changes over time. Recent advances in econometrics affirm that fixed-effects panel regression with clustered standard errors offers superior robustness in this context, enabling valid inference despite heteroscedasticity and within-panel correlation (Eugenio-Martín & Patuelli, 2022). The methodology was approved with exemption by the Institutional Review Board of Chiang Mai Rajabhat University (Certificate No. IRBCMRU 2025/539.22.10) on October 24, 2025. This research was classified as a no human action. Researcher collected data from publicly available sources. Data were collected between October and December 2025.

2.1 Sampling and Data Sources

The sample includes 48 Thai sport-tech firms that received CVC funding between 2005 and 2025. “Sport-tech” refers to businesses whose core offerings involve technology applied to sports performance, management, or fan engagement (Ratten, 2020). Firms were identified through commercial VC databases such as Crunchbase and PitchBook, Thai government and industry records including the Department of Business Development and the National Innovation Agency, and public corporate disclosures such as annual reports and press releases. To be included, firms had to operate primarily in Thailand, be engaged in the sport-tech domain including areas such as wearables, analytics, and e-sports technology, and have received at least one CVC investment. The final dataset comprises 48 firms and 73 CVC transactions.

To ensure accuracy and completeness, data from commercial databases were cross-checked with official government sources and industry association publications. Duplicate entries across sources were consolidated using firm registration numbers, and transaction dates were verified against press release timelines. This triangulation process minimized the risk of including erroneous or unverifiable deals, thereby increasing the reliability of the sample for longitudinal analysis.

2.2 Variable Measurement

The study includes two independent variables, two dependent variables, two moderating variables, and four control variables. Operational definitions, measurement methods, and data sources are summarized in Table 1. All variables were coded using a structured data extraction protocol developed for this study. The coding process relied on publicly available information such as investment announcements, company reports, industry databases, and press releases. To ensure consistency, each observation was recorded following predefined coding criteria and cross-checked across multiple data sources.

Independent variables include Technology-Oriented CVC and Foreign-Oriented CVC. Technology-Oriented CVC is coded as 1 if the investment was aimed at acquiring new technology or innovation capability, and 0 otherwise, based on investment announcements, investor statements, and product descriptions. Coding decisions were based on explicit statements of strategic intent reported in investor communications or company disclosures, such as references to technological collaboration, product development partnerships, or access to innovation capabilities. Foreign-Oriented CVC is coded as 1 if the investment originated from a foreign corporate investor or explicitly targeted foreign market entry, and 0 otherwise, determined from investor nationality and stated strategic intent. Information on investor origin and investment objectives was verified through venture capital databases and corporate press releases.

Dependent variables comprise Technology Portfolio Diversification and International Market Expansion. Technology Portfolio Diversification is measured using the entropy index, calculated from the distribution of a firm’s products or technologies before and after the CVC investment, based on company reports, product catalogs, and patent filings. International Market Expansion refers to the geographic diversification of a firm’s activities across foreign markets following CVC investment. This measure captures changes in the number of foreign markets served by the firm and/or the proportion of foreign revenue within three years post-investment. The operationalization emphasizes the expansion of international market presence rather than the intensity of sales within a single foreign market. Data were obtained from annual reports, export records, and market announcements.

Industry Distance and Cultural Distance are moderating variables. Industry Distance is computed as a similarity index between the primary industry classification codes under the International Standard Industrial Classification (ISIC) of the investor and investee, where a higher score indicates greater dissimilarity, based on public registry and industry classification databases. Industry classifications were obtained from official company registries and industry databases, allowing the comparison of technological domains between corporate investors and portfolio firms. Cultural Distance is measured using the variance-based metric developed by Beugelsdijk and Welzel (2018), which combines Hofstede’s six cultural dimensions—Power Distance (PDI), Individualism versus Collectivism (IDV), Masculinity versus Femininity (MAS), Uncertainty Avoidance (UAI), Long-Term Orientation (LTO), and Indulgence versus Restraint (IVR)—with Inglehart–Welzel World Values Survey cultural clusters. This approach improves upon earlier measures by accounting for variability across dimensions and provides a more nuanced understanding of cultural differences between the investor’s home country and Thailand, particularly relevant for the Thai sport-tech sector where cultural context shapes interorganizational collaboration.

Control variables include firm age, firm size, prior internationalization experience, and prior CVC experience. Firm age is measured as the number of years since incorporation, obtained from company registration data. Firm size is measured as the number of employees at the time of investment, based on annual reports, company disclosures, and LinkedIn company pages. Prior internationalization experience captures the firm’s baseline exposure to foreign markets before receiving CVC investment. It is measured by the number of foreign markets served and/or the proportion of export revenue prior to the focal investment event. This variable is included as a control to distinguish pre-existing international market presence from the post-investment international expansion analyzed as the dependent variable. Prior CVC experience is measured as the number of previous CVC deals received by the firm, based on historical investment records and press releases.

Table 1

Variable and Measurement

|

Variable |

Variable |

Definition / |

Measurement / |

|---|---|---|---|

|

Independent Variables |

Technology-Oriented CVC |

Corporate venture capital investment with strategic intent to access new technologies, innovation capabilities, or R&D resources from the portfolio company |

Binary variable coded 1 when investment announcements or investor disclosures indicate technological collaboration or innovation objectives; 0 otherwise; Sources: investment announcements, company reports, venture capital databases |

|

Foreign-Oriented CVC |

CVC investment from foreign corporate investor or explicitly targeting foreign market entry |

Binary variable: 1 = foreign investor or foreign market expansion goal; 0 = otherwise Based on investor nationality and stated strategic intent |

|

|

Dependent Variables |

Technology Portfolio Diversification |

Breadth of technological domains embedded in the firm’s products or services |

Entropy index calculated from the distribution of technologies or product categories across the firm’s portfolio; Sources: company reports, product documentation, patent records |

|

International Market Expansion |

Geographic diversification of a firm’s activities across foreign markets following CVC investment |

Change in the number of foreign markets served and/or share of foreign revenue within three years after investment; Sources: annual reports, export records, market announcements |

|

|

Moderating Variables |

Industry Distance |

Difference between investor’s and investee’s primary industry classifications |

Similarity index based on ISIC codes; higher scores = lower similarity; Calculated using public registry and industry classification databases |

|

Cultural Distance |

Extent of cultural difference between investor’s home country and Thailand |

Variance-based cultural distance metric (Beugelsdijk & Welzel, 2018) combining Hofstede’s six cultural dimensions (PDI, IDV, MAS, UAI, LTO, IVR) with Inglehart–Welzel World Values Survey clusters |

|

|

Control Variables |

Firm Age |

Years since firm incorporation |

Company registration data |

|

Firm Size |

Number of employees at the time of investment |

Annual reports, company disclosures, and LinkedIn company pages |

|

|

Prior Internationalization Experience |

Firm’s baseline exposure to foreign markets prior to receiving CVC investment |

Number of foreign markets served and/or proportion of export revenue before the focal investment; Sources: company reports, export statistics |

|

|

Prior CVC Experience |

Number of prior CVC deals received by the firm |

Historical investment records from databases and company press releases |

2.3 Analytic Strategy

Panel data regression models with firm fixed effects were employed to control for unobserved time-invariant heterogeneity across firms. To ensure reliable inference in the presence of potential cross-sectional and serial correlations, cluster-robust standard errors were applied, a method widely recognized for enhancing inference reliability in panel data analysis (Cameron & Miller, 2015). Separate models were estimated for each dependent variable, and interaction terms were included to test the moderating effects of industry distance and cultural distance. This analytic approach is consistent with the empirical framework developed by Schmidt and colleagues (Schmidt et al., 2025) but adapted to the Thai sport-tech context, where unique market characteristics and institutional conditions necessitate context-sensitive modeling.

To empirically test the hypotheses, panel regression models with firm fixed effects were specified to control for unobserved, time-invariant heterogeneity across firms. Cluster-robust standard errors were applied at the firm level to account for cross-sectional dependence and serial correlation, consistent with best practice in panel data analysis (Cameron & Miller, 2015). The general regression model is specified as:

where:

Yit is a dependent variable (Technology Portfolio Diversification or International Market Expansion) for firm i at time t.

TechCVCit is Technology-Oriented CVC Investments.

ForeignCVCit is Foreign-Oriented CVC Investments.

IndDistit is Industry Distance between the investor and the investee.

CulDistit is Cultural Distance between investor’s home country and Thailand.

Controlsit is a vector of control variables (Firm Age, Firm Size, Prior Internationalization Experience, Prior CVC Experience).

αi is firm fixed effects.

εit is the error term.

Moreover, the hypotheses were also established. The dependent variables are Technology Portfolio Diversification (TPD) and International Market Expansion (IME). The key independent variables are Technology-Oriented CVC (TechCVC) and Foreign-Oriented CVC (ForeignCVC). Moderating variables include Industry Distance (IndDist) and Cultural Distance (CultDist), while the set of control variables includes firm age, firm size, prior internationalization experience, and prior CVC experience. The equations for each hypothesis are as follows:

H1: TPDit = β0 + β1 TechCVCit + γControlsit + αi + ϵit

Expected sign: β1>0.

H2: IMEit = δ0 + δ1 ForeignCVCit + ØControlsit + αi + uit

Expected sign: δ1>0.

H3a: TPDit = β0 + β1 TechCVCit + β2 IndDistit + β3 (TechCVCit × IndDistit) + γControlsit + αi + εit

Expected sign: β3 < 0.

H3b: TPDit = β0 + β1 TechCVCit + β4 IndDistit + β5 (TechCVCit × CulDistit) + γControlsit + αi + ϵit

Expected sign: β5 < 0.

H3c: IMEit = δ0 + δ1 ForeignCVCit + δ2 In dDistit + δ3 (ForeignCVCit × IndDistit)

+ ØControlsit + αi + uit

Expected sign: δ3 < 0.

H3d: IMEit = δ0 + δ1 ForeignCVCit + δ4 IndDistit + δ5 (ForeignCVCit × IndDistit) + ØControlsit + αi + uit

Expected sign: δ5 < 0.

To strengthen the robustness of results, several additional tests were conducted. First, random-effects specifications were estimated as a comparison to fixed-effects models to examine whether unobserved heterogeneity might bias results. Second, lagged dependent variables were included in alternative models to account for potential reverse causality, particularly in the relationship between CVC inflows and subsequent international expansion. Third, alternative measures of cultural distance were tested, including a Hofstede-based index, to confirm the consistency of findings with different operationalizations. Fourth, subsample analyses were performed by separating domestic and foreign CVC investors, providing insight into whether the source of investment influenced outcomes differently. Collectively, these robustness checks increase the validity of the results and reinforce the study’s contribution to understanding the role of CVC in shaping the trajectory of Thai sport-tech enterprises.

3. Results

3.1 Descriptive Statistics and Correlations

Table 2 presents descriptive statistics for all variables. The sample consists of 48 Thai sport-tech firms that received at least one CVC investment between 2005 and 2025, yielding 154 firm-year observations. The mean technology portfolio diversification score is 1.79 (SD = 0.61), while the mean international market expansion score is 2.26 (SD = 0.97). These values suggest moderate variation in both technological breadth and international market presence among the sampled firms. Approximately 42% of the investments are classified as technology-oriented, and 35% involve foreign-oriented CVC investors. This distribution indicates that a substantial proportion of CVC investments in the Thai sport-tech sector are strategically oriented toward either technological capability development or international market access.

Correlation analysis (Table 3) indicates that Technology-Oriented CVC is positively associated with Technology Portfolio Diversification (r = 0.23, p < .05), and Foreign-Oriented CVC is positively associated with International Market Expansion (r = 0.27, p < .01). These associations provide preliminary descriptive evidence consistent with the expected relationships proposed in the hypotheses. Industry Distance and Cultural Distance are negatively correlated with both dependent variables, suggesting that greater institutional or industry differences between investors and portfolio firms may be associated with weaker innovation and internationalization outcomes. Variance inflation factors (VIFs) are below 2.5, indicating that multicollinearity is not a concern.

Table 2

Descriptive Statistics

|

Variables |

mean |

SD |

min |

max |

|---|---|---|---|---|

|

1. Technology Portfolio Diversification (TPD) |

1.79 |

0.61 |

1.00 |

4.00 |

|

2. International Market Expansion (IME) |

2.26 |

0.97 |

1.00 |

5.00 |

|

3. Technology-Oriented CVC (TechCVC) |

0.42 |

0.49 |

0.00 |

1.00 |

|

4. Foreign-Oriented CVC (ForeignCVC) |

0.35 |

0.48 |

0.00 |

1.00 |

|

5. Industry Distance (IndDist) |

0.41 |

0.27 |

0.01 |

0.95 |

|

6. Cultural Distance (CultDist) |

0.48 |

0.25 |

0.05 |

0.92 |

|

7. Firm Age (years) |

7.20 |

4.60 |

1.00 |

20.0 |

|

8. Firm Size (employees) |

152 |

220 |

10 |

950 |

|

9. Prior Internationalization Experience |

0.33 |

0.47 |

0.00 |

1.00 |

|

10. Prior CVC Experience |

0.29 |

0.45 |

0.00 |

1.00 |

Note. n = 48 firms, 154 firm-year observations.

Table 3

Correlation Matrix

|

Variables |

1 |

2 |

3 |

4 |

5 |

6 |

|---|---|---|---|---|---|---|

|

1. TPD |

1.00 |

|||||

|

2. IME |

0.31** |

1.00 |

||||

|

3. TechCVC |

0.23* |

0.15 |

1.00 |

|||

|

4. ForeignCVC |

0.18 |

0.27** |

0.12 |

1.00 |

||

|

5. IndDist |

-0.19* |

-0.16 |

-0.11 |

-0.17 |

1.00 |

|

|

6. CultDist |

-0.21* |

-0.18* |

-0.10 |

-0.22* |

0.29** |

1.00 |

Note. * p < .05, ** p < .01.

3.2 Regression Results for Main Effects

Table 4 reports the fixed-effects regression results. The models examine the relationships between CVC investment orientation and the strategic outcomes of sport-tech firms while controlling for firm characteristics and prior internationalization experience. Model 1 tests the direct relationship between Technology-Oriented CVC and Technology Portfolio Diversification (H1). Results show that Technology-Oriented CVC is positively and significantly associated with diversification (β = 0.19, p < .05), supporting H1. This finding suggests that sport-tech firms receiving technology-oriented CVC investments tend to exhibit broader technological portfolios compared with periods in which such investments are absent.

Model 2 tests the relationship between Foreign-Oriented CVC and International Market Expansion (H2). Findings indicate that Foreign-Oriented CVC is positively and significantly associated with international market expansion (β = 0.28, p < .01), supporting H2. This result suggests that sport-tech firms receiving investment from foreign corporate partners tend to expand their presence across a broader set of international markets.

Control variables behave largely as expected. Firm size and prior internationalization experience are positively associated with international market expansion, indicating that larger firms and those with existing foreign market exposure tend to operate in a wider range of international markets. Firm age is negatively associated with technology portfolio diversification, suggesting that younger firms may demonstrate greater flexibility in expanding their technological scope.

Table 4

Fixed-Effects Regression Results

|

Variables |

Model 1 |

Model 2 |

Model 3 |

Model 4 |

Model 5 |

Model 6 |

|---|---|---|---|---|---|---|

|

Technology-Oriented CVC |

0.19* |

0.18** |

0.17** |

|||

|

Foreign-Oriented CVC |

0.28** |

0.26** |

0.25** |

|||

|

Industry Distance |

-0.07 |

-0.09 |

||||

|

Cultural Distance |

-0.08 |

-0.10 |

||||

|

TechCVC × IndDist |

-0.13* |

|||||

|

TechCVC × CultDist |

-0.16* |

|||||

|

ForeignCVC × IndDist |

-0.20** |

|||||

|

ForeignCVC × CultDist |

-0.17* |

|||||

|

Firm Age |

-0.08* |

-0.02 |

-0.09* |

-0.10* |

-0.03 |

-0.04 |

|

Firm Size |

0.05 |

0.11* |

0.06 |

0.07 |

0.12* |

0.13* |

|

Prior Internationalization |

0.18** |

0.17** |

0.19** |

|||

|

Prior CVC Experience |

0.04 |

0.07 |

0.05 |

0.06 |

0.08 |

0.09 |

|

R² (within) |

0.22 |

0.27 |

0.25 |

0.26 |

0.29 |

0.31 |

Note. Fixed-effects models with cluster-robust standard errors: n = 154 firm-year observations, 48 firms. TPD = Technology Portfolio Diversification; IME = International Market Expansion. *p < .05, **p < .01.

3.3 Moderating Effects of Industry and Cultural Distance

Models 3–6 incorporate interaction terms to test the moderating relationships proposed in H3a–H3d. Model 3 includes the interaction between Technology-Oriented CVC and Industry Distance. Results reveal a negative and significant interaction (β = –0.13, p < .05), indicating that greater industry distance is associated with a weaker relationship between technology-oriented CVC and technology portfolio diversification. This finding is consistent with H3a.

Model 4 examines the interaction between Technology-Oriented CVC and Cultural Distance. The interaction is negative and significant (β = –0.16, p < .05), suggesting that higher cultural distance is associated with a weaker relationship between technology-oriented CVC investments and technology diversification. This result provides support for H3b.

Model 5 tests the interaction between Foreign-Oriented CVC and Industry Distance. The coefficient is negative and significant (β = –0.20, p < .01), indicating that larger industry differences between investors and portfolio firms are associated with reduced international market expansion linked to foreign-oriented CVC investments. This result supports H3c.

Model 6 evaluates the interaction between Foreign-Oriented CVC and Cultural Distance. The coefficient is also negative and significant (β = –0.17, p < .05), suggesting that greater cultural distance is associated with weaker international market expansion among firms receiving foreign-oriented CVC investments. This finding confirms H3d.

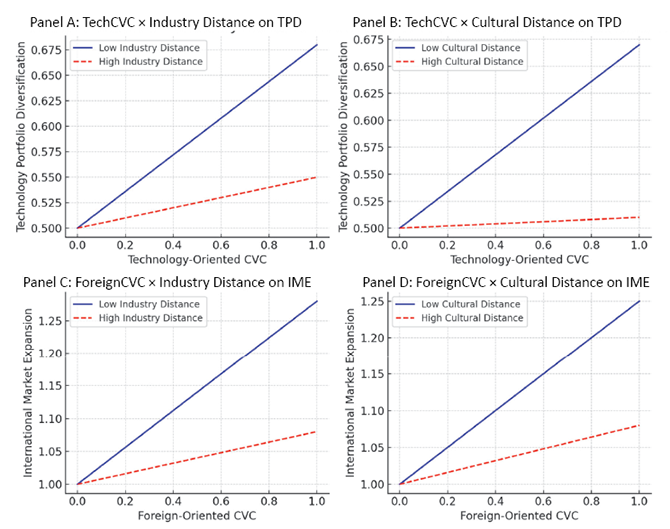

Figure 2

Moderating Effects of Industry Distance and Cultural Distance on the Relationships between CVC Investments and Firm Outcomes

Note. Panel A shows that the positive association between Technology-Oriented CVC and Technology Portfolio Diversification (TPD) is stronger under low industry distance than under high industry distance. Panel B indicates that Technology-Oriented CVC is more strongly associated with TPD when cultural distance is low. Panel C illustrates that Foreign-Oriented CVC has a stronger association with International Market Expansion (IME) —conceptualized as geographic market diversity— when industry distance is low, while Panel D shows that this association is also stronger when cultural distance is low. Predicted values are based on fixed-effects regression models with cluster-robust standard errors.

Figure 2 illustrates these moderating relationships using marginal effect plots. The plots indicate that the positive associations between CVC investment orientation and firm strategic outcomes become weaker as industry or cultural distance increases. This pattern highlights the importance of contextual alignment between investors and portfolio companies for effective interorganizational learning within the Thai sport-tech sector.

3.4 Robustness Assessment

Several robustness tests were conducted to assess the stability of the findings. These additional analyses were designed to examine whether the main results remain consistent under alternative model specifications and measurement approaches. First, random-effects specifications were estimated as a comparison to the fixed-effects models, and the results remained consistent with those reported in the primary models. The direction and statistical significance of the key relationships between CVC investment orientation and firm strategic outcomes were largely unchanged.

Second, lagged dependent variables were included to account for potential temporal dynamics and to reduce concerns about reverse causality. The estimated relationships between CVC investment orientation and the outcome variables remained statistically significant, indicating that the observed associations are not driven solely by contemporaneous correlations.

Third, alternative cultural distance measures based solely on Hofstede’s dimensions yielded similar results, suggesting that the moderating role of cultural distance is robust to alternative operationalizations.

Finally, subsample analyses revealed that domestic investors are more strongly associated with technology portfolio diversification, while foreign investors are more strongly associated with international market expansion. These patterns are consistent with the expectation that domestic investors may contribute more directly to technological collaboration within the local ecosystem, whereas foreign investors may provide stronger international network connections that facilitate geographic market expansion.

3.5 Summary of Findings

Overall, the results provide empirical support for the proposed relationships in the conceptual framework. Technology-Oriented CVC is positively associated with technology portfolio diversification, and Foreign-Oriented CVC is positively associated with international market expansion. These findings suggest that different orientations of corporate venture capital investment are linked to distinct strategic outcomes for sport-tech enterprises.

However, the strength of these relationships varies depending on the contextual distance between investors and investee firms. The results indicate that greater industry distance and cultural distance are associated with weaker relationships between CVC investments and firm strategic outcomes. In other words, when corporate investors and sport-tech firms operate in more distant industrial or cultural contexts, the potential benefits associated with CVC investment become less pronounced.

Taken together, these findings highlight the importance of relational and contextual alignment in corporate venture capital partnerships. CVC investment may function as a mechanism that facilitates access to technological resources and international networks, but its strategic value appears to depend on the extent to which investors and portfolio firms share compatible industry knowledge bases and cultural contexts.

4. Discussion

The purpose of this study was to examine how corporate venture capital (CVC) is associated with the strategic development of Thai sport-tech firms, particularly in relation to technology portfolio diversification and international market expansion. Building on the interorganizational learning perspective (Lane & Lubatkin, 1998; Schmidt et al., 2025), this research investigated whether different orientations of CVC investment are related to distinct strategic outcomes and how industry and cultural distance condition these relationships.

The empirical analysis of 48 firms across 154 firm-year observations provides evidence that technology-oriented CVC investments are positively associated with technology portfolio diversification, while foreign-oriented CVC investments are positively associated with international market expansion. These findings suggest that the strategic orientation of corporate investors may be linked to different dimensions of firm development, supporting the conceptual distinction proposed in the study.

At the same time, the results indicate that the strength of these relationships depends on the contextual alignment between the investor and the investee firm. Specifically, greater industry distance and cultural distance are associated with weaker relationships between CVC investment orientation and firm outcomes. These moderating patterns are consistent with the interorganizational learning perspective, which emphasizes the importance of knowledge compatibility and relational proximity for effective knowledge transfer (Rossi et al., 2020).

Overall, the findings provide empirical support for the proposed conceptual framework and offer insights into how CVC investment orientation and contextual distance jointly shape the strategic trajectories of sport-tech enterprises in an emerging economy. The following subsections discuss these results in relation to each hypothesis and the broader literature on corporate venture capital and innovation-driven firm growth.

4.1 Hypothesis 1: Technology-Oriented CVC and Technology Portfolio Diversification

The first hypothesis predicted that technology-oriented CVC investments would be positively related to technology portfolio diversification. The empirical results provide support for this hypothesis, indicating that technology-oriented CVC is positively associated with greater diversification of technology portfolios among Thai sport-tech firms. Firms that received investment from technologically aligned corporate investors tended to expand the range of technological applications within their product portfolios, including wearable performance devices, performance analytics platforms, and fan-engagement technologies. This pattern is consistent with prior research in other sectors showing that corporate venture capital relationships can enhance firms’ absorptive capacity by exposing them to complementary technologies and knowledge domains (Chemmanur et al., 2014; Schmidt et al., 2025).

Beyond documenting this relationship, the findings also suggest several mechanisms through which technology-oriented CVC may be associated with portfolio diversification. Firms that engaged with technology-focused corporate investors appear to benefit from knowledge exchange, collaborative development activities, and exposure to external technological standards and practices. These interactions may broaden the range of technological capabilities available to portfolio firms and facilitate the integration of new technological components into existing products and services. Such patterns are consistent with the interorganizational learning perspective, which emphasizes that alliances with technologically sophisticated partners can support the acquisition and recombination of external knowledge (Lane & Lubatkin, 1998). In the CVC context, this process has been described as a form of learning-by-investing, where investment relationships create opportunities for knowledge transfer and technological experimentation (Dushnitsky & Lenox, 2005; Rossi et al., 2020).

The Thai sport-tech context provides an additional perspective on this mechanism. Because the domestic innovation ecosystem for sport-technology remains relatively small, partnerships with corporate investors may provide access to technological expertise and development infrastructures that are otherwise difficult for young firms to obtain internally. Through such relationships, portfolio firms may gain exposure to broader technological networks and industry standards, which can facilitate experimentation with new technological applications.

Taken together, these findings suggest that technology-oriented CVC investment is associated with broader technology portfolios among sport-tech firms. Rather than functioning solely as a financial resource, CVC appears to operate as a channel through which external technological knowledge and capabilities can enter entrepreneurial firms. In line with earlier research on the Thai sports industry ecosystem (Chankuna, 2024), the results highlight the importance of strategic capital and knowledge partnerships for supporting the development of innovation-driven sport enterprises.

4.2 Hypothesis 2: Foreign-Oriented CVC and International Market Expansion

The second hypothesis proposed that foreign-oriented CVC would be positively related to international market expansion. The empirical findings provide support for this hypothesis, indicating that foreign-oriented CVC investment is positively associated with broader geographic market presence among Thai sport-tech firms. Firms that received investment from foreign corporate partners tended to expand their activities across a greater number of international markets, particularly within regional ecosystems such as Southeast Asia as well as selected global markets. Examples include esports platforms expanding into neighboring ASEAN markets and wearable technology firms collaborating with international distribution partners. These findings are consistent with prior research showing that corporate venture capital relationships can facilitate international market access by providing portfolio companies with access to foreign business networks, distribution channels, and reputational legitimacy (Song et al., 2023).

Beyond documenting this relationship, the results also suggest mechanisms through which foreign-oriented CVC may support geographic market expansion. From an international business perspective, emerging market firms often face the liability of foreignness, meaning that unfamiliar institutional environments and limited reputation abroad can create barriers to entry in foreign markets (Zaheer, 1995). Corporate investors with established international operations may help reduce these barriers by providing market knowledge, regulatory guidance, and credibility signals to external stakeholders. Through association with reputable international investors, sport-tech firms may gain legitimacy in foreign markets and benefit from the investor’s existing commercial networks.

In addition, foreign corporate investors can provide strategic knowledge about international commercialization processes, including distribution systems, partnership development, and product adaptation to local consumer preferences. Such knowledge transfer is consistent with research highlighting the importance of external learning channels in supporting firm internationalization (Bertoni et al., 2011; Gaba & Meyer, 2017). Within the sport-tech context, these forms of support may be particularly valuable because firms often need to navigate diverse sports cultures, regulatory frameworks, and digital market infrastructures when expanding internationally.

Taken together, these findings suggest that foreign-oriented CVC investment is associated with broader geographic market expansion among Thai sport-tech firms. Rather than operating solely as a financial resource, foreign corporate venture capital may function as a strategic gateway to international markets by connecting entrepreneurial firms to global networks and institutional knowledge. In this sense, the results indicate that international expansion in emerging sport-tech ecosystems may depend not only on entrepreneurial capabilities but also on access to internationally embedded investment partners.

4.3 Hypotheses 3a–3d: Moderating Effects of Industry and Cultural Distance

The third set of hypotheses proposed that industry distance and cultural distance would negatively moderate the relationships between CVC investment orientation and firm strategic outcomes. The regression models and marginal effect plots provide empirical support for these moderating relationships. Specifically, the results indicate that greater industry distance and greater cultural distance are associated with weaker relationships between CVC investment orientation and both technology portfolio diversification and international market expansion. These findings highlight the importance of contextual compatibility in CVC partnerships.

From an interorganizational learning perspective, effective knowledge transfer between organizations depends on the degree of similarity in their technological bases and knowledge structures (Lane & Lubatkin, 1998). When the industry distance between the investor and the portfolio firm is large, the two organizations may lack a shared technological language or compatible development routines. In such cases, the ability of the investee firm to absorb and recombine external knowledge may be reduced. Consistent with this reasoning, the results suggest that higher industry distance is associated with a weaker relationship between technology-oriented CVC and technology portfolio diversification. This pattern aligns with research on interindustry alliances, which indicates that excessive technological distance may limit absorptive capacity and reduce the effectiveness of knowledge exchange (Nooteboom et al., 2007).

A similar pattern emerges for cultural distance. Cultural distance refers to differences in norms, managerial practices, and communication styles between organizations originating from different national contexts. When such differences are large, collaboration may be constrained by misunderstandings, coordination difficulties, or divergent expectations regarding decision-making and knowledge sharing. The results of this study indicate that greater cultural distance is associated with weaker relationships between CVC investment orientation and firm strategic outcomes. In particular, cultural distance appears to reduce the strength of the association between both technology-oriented CVC and technology portfolio diversification, as well as between foreign-oriented CVC and international market expansion. This finding is consistent with research on cross-border alliances, which shows that cultural incompatibility can hinder the transfer of tacit knowledge and limit the effectiveness of collaborative learning processes (Park & Ungson, 2001).

These moderating patterns are also visible in the context of international expansion. Foreign-oriented CVC may provide portfolio firms with access to international networks and market knowledge, but the benefits of such relationships appear to depend on the degree of alignment between the investor and the investee. The results suggest that when industry or cultural distance between partners is large, the association between foreign-oriented CVC and international market expansion becomes weaker. Conversely, partnerships with investors from technologically related industries or culturally proximate regions may facilitate more effective collaboration and knowledge transfer. Similar patterns have been observed in prior studies of corporate venture capital and interorganizational learning (Schmidt et al., 2025).

Taken together, these findings support the view that the strategic value of CVC partnerships is contingent on relational and contextual compatibility. While corporate venture capital can connect entrepreneurial firms to external knowledge and global networks, its effectiveness appears to depend on the extent to which investors and portfolio companies share compatible technological backgrounds and cultural contexts. For sport-tech firms operating in emerging innovation ecosystems, these results underscore the importance of selecting corporate partners whose industry expertise and cultural proximity support meaningful knowledge exchange and collaborative development.

4.4 Integrating the Findings

Taken together, these findings provide an integrated perspective on how different orientations of corporate venture capital investment are associated with the strategic development of sport-tech enterprises in Thailand. The empirical results indicate that technology-oriented CVC is positively associated with technology portfolio diversification, while foreign-oriented CVC is positively associated with broader international market presence. At the same time, the analysis demonstrates that the strength of these relationships varies depending on the level of industry and cultural distance between the investing corporation and the portfolio firm. These patterns suggest that CVC relationships may function as channels for knowledge transfer and network access, but their effectiveness depends on the compatibility of the partners involved.

From a theoretical perspective, these findings reinforce the relevance of the interorganizational learning framework for understanding corporate venture capital relationships in emerging market contexts. Firms appear more capable of leveraging external investment partnerships when they share compatible knowledge bases and institutional contexts with their corporate investors. When industry or cultural distance becomes large, the potential learning and collaboration benefits associated with CVC relationships appear to weaken. In this sense, the results illustrate how structural and relational conditions shape the extent to which external investment partnerships translate into strategic outcomes.

In practical terms, the findings suggest that sport-tech enterprises and investors may benefit from prioritizing partnerships that combine financial investment with technological and contextual compatibility. For firms operating in emerging sport innovation ecosystems such as Thailand, corporate venture capital relationships may provide access to technological expertise and international networks that are otherwise difficult to obtain. However, the results also indicate that the strategic value of such partnerships may depend on the degree of alignment between the investor’s industry expertise and the firm’s technological focus, as well as the cultural proximity between the collaborating organizations.

Overall, this study contributes to the literature by extending research on corporate venture capital to the sport-tech sector within an emerging economy context. By examining how investment orientation and contextual distance jointly shape firm outcomes, the research provides new insights into how CVC partnerships operate in environments characterized by resource constraints and evolving innovation ecosystems. These insights offer implications for entrepreneurs, corporate investors, and policymakers seeking to leverage investment partnerships to support innovation-driven growth and international market participation.

5. Implications

5.1 Theoretical Implications

This study offers several theoretical contributions to the literature on corporate venture capital, innovation strategy, and emerging-market entrepreneurship.

First, the research extends the application of corporate venture capital (CVC) theory to the sport-tech sector, an industry that has received limited attention in prior CVC scholarship. Existing studies have primarily examined CVC in manufacturing, biotechnology, and information technology contexts. By focusing on sport-tech enterprises, this study demonstrates how CVC relationships operate in innovation ecosystems characterized by strong links between digital technologies, sports culture, and entrepreneurial experimentation. Situating the analysis in Thailand also contributes to the literature on emerging market innovation systems, where institutional constraints, limited domestic venture financing, and culturally embedded industries shape entrepreneurial development.

Second, the findings contribute to interorganizational learning theory by highlighting the contextual conditions under which knowledge transfer through CVC relationships is more or less effective. The results indicate that technology-oriented CVC investments are associated with broader technology portfolio diversification, while foreign-oriented CVC investments are associated with wider international market presence. At the same time, the moderating effects of industry distance and cultural distance suggest that the strategic value of CVC relationships depends on the compatibility between investors and portfolio firms. These findings reinforce the idea that effective knowledge transfer requires a degree of cognitive and contextual proximity between collaborating organizations (Lane & Lubatkin, 1998).

Third, the study contributes to the corporate venturing literature by shifting attention from the presence of CVC funding to the mechanisms through which CVC relationships are associated with firm-level strategic change. Much of the prior literature has focused on whether firms receive corporate venture capital. In contrast, this study emphasizes how different orientations of CVC investment are linked to distinct strategic outcomes, including technological diversification and geographic market expansion. This perspective advances a more nuanced understanding of how strategic investment partnerships may shape entrepreneurial firm trajectories beyond simple capital provision.

Finally, by integrating investment orientation, contextual distance, and firm strategic outcomes into a single empirical framework, the study provides a more comprehensive perspective on how CVC partnerships operate in emerging innovation ecosystems. These insights extend the theoretical conversation on corporate venture capital by illustrating how investment orientation and relational compatibility jointly influence the strategic development of entrepreneurial firms. Although the empirical setting is Thailand, the mechanisms identified in this research may also be relevant for other emerging economies in Asia, Africa, and Latin America where entrepreneurial firms rely on external partnerships to access technological resources and international markets.

5.2 Managerial Implications

From a managerial perspective, the findings provide several practical insights for entrepreneurs, corporate investors, and policymakers operating within emerging sport-tech ecosystems.

First, the results suggest that entrepreneurs should view corporate venture capital not only as a financial resource but also as a strategic partnership that may provide access to technological expertise and international market networks. The positive association between technology-oriented CVC and technology portfolio diversification indicates that collaborations with technologically aligned corporate investors may support the expansion of product and technology portfolios through exposure to new knowledge domains and development practices. For sport-tech entrepreneurs, selecting corporate investors with complementary technological capabilities may therefore be an important strategic decision when seeking external investment.

Second, the findings highlight the potential value of foreign-oriented CVC relationships for firms seeking to expand internationally. The observed association between foreign CVC and broader geographic market presence suggests that international corporate investors may provide portfolio firms with access to global networks, distribution channels, and market intelligence. Entrepreneurs aiming to enter foreign markets may benefit from forming partnerships with investors who possess experience in international commercialization and cross-border business development.

Third, the moderating effects of industry distance and cultural distance indicate that the success of CVC partnerships may depend on the degree of compatibility between the investor and the entrepreneurial firm. Corporate investors and portfolio companies may therefore benefit from carefully evaluating strategic fit before forming investment partnerships. Firms whose technological focus and organizational culture align with those of their corporate investors may be better positioned to translate investment relationships into meaningful collaborative outcomes.

Finally, the findings also offer implications for innovation policy and ecosystem development in emerging economies. The results suggest that corporate venture capital may function as a complementary mechanism for strengthening innovation ecosystems by connecting entrepreneurial firms with technological resources and international networks. Policymakers seeking to promote innovation-driven growth in sectors such as sport-tech may therefore consider policies that encourage collaboration between domestic start-ups and both domestic and international corporate investors. Such initiatives may help entrepreneurial firms overcome resource constraints while supporting the broader development of knowledge-intensive industries.

5.3 Policy Implications

From a policy perspective, the findings highlight the potential role of corporate venture capital as a complementary mechanism for strengthening innovation ecosystems in emerging sport-tech industries. The empirical results suggest that different orientations of CVC investment are associated with distinct strategic outcomes for entrepreneurial firms, including technology portfolio diversification and international market expansion. In this context, policymakers may consider initiatives that encourage stronger collaboration between corporate investors and sport-tech entrepreneurs.

One potential policy direction is the development of institutional incentives that encourage corporate participation in venture investment activities. Governments may support the growth of CVC ecosystems through tax incentives, co-investment programs, or risk-sharing mechanisms that reduce the perceived uncertainty of investing in emerging technology sectors. Such initiatives may encourage established corporations to engage more actively with entrepreneurial firms, thereby expanding the availability of strategic capital within the sport-tech sector.

The results also highlight the importance of industry and cultural compatibility in investment partnerships. Because the analysis indicates that greater industry and cultural distance may weaken the relationship between CVC investment orientation and firm outcomes, policymakers may consider supporting intermediary platforms that facilitate strategic matching between investors and start-ups. Government agencies such as national innovation authorities or industry development organizations could promote innovation forums, corporate–startup partnership programs, and cross-border investment networks that connect sport-tech entrepreneurs with investors from technologically related industries or culturally proximate regions.

In addition, policies that strengthen absorptive capacity within entrepreneurial firms may further enhance the benefits associated with CVC partnerships. Programs that promote entrepreneurial training, university–industry collaboration, and technology-focused innovation clusters may help firms develop the organizational capabilities required to effectively utilize external knowledge and investment resources. Such initiatives may increase the likelihood that investment partnerships translate into technological development and international market participation.

These policy considerations are also consistent with broader economic development strategies that emphasize innovation-driven growth and the global promotion of cultural industries. In Thailand, for example, the development of sport-related technologies is increasingly linked to national initiatives that position sport as a component of cultural soft power and digital economic development (Thawesaengskulthai et al., 2024). Strengthening the institutional conditions that support CVC partnerships may therefore contribute not only to entrepreneurial growth but also to the broader development of knowledge-intensive sport industries.

Although the empirical analysis focuses on Thailand, the insights generated by this study may also be relevant for other emerging economies facing similar structural constraints. Countries across Southeast Asia, Latin America, and Africa often encounter comparable challenges, including limited access to venture financing, fragmented innovation ecosystems, and institutional barriers to international market participation. By illustrating how CVC partnerships interact with these contextual conditions, the study offers comparative insights for policymakers seeking to leverage corporate investment partnerships to strengthen innovation ecosystems and support the global competitiveness of emerging technology sectors.

6. Limitations and Future Research

As with all empirical studies, this research has limitations that should be acknowledged. First, the dataset is relatively small, reflecting the limited number of sport-tech firms in Thailand that have received corporate venture capital (CVC) investment during the study period. The emerging nature of the sport-tech sector and the relatively recent adoption of CVC investment in this industry constrain the availability of large-scale datasets. The dataset therefore includes only Thai sport-tech firms that received CVC investment. The absence of a matched control group of non-CVC-backed firms limits the ability to draw strong causal inferences about the comparative effects of CVC. This reflects data constraints: many non-funded sport-tech firms in Thailand operate informally, lack transparent disclosures, or do not report systematic information on innovation outcomes and international activities. To partially address these limitations, this study employs a longitudinal panel design that increases the number of observations across time and enables the analysis of within-firm changes following CVC investment. As a result, the study focuses on the mechanisms of post-investment transformation within CVC-backed firms rather than direct counterfactual comparisons.

Future research can address this gap by constructing broader samples that include both CVC-backed and non-CVC-backed firms. Comparative datasets across multiple emerging economies could also increase the number of observations and improve statistical power. Quasi-experimental designs such as propensity score matching, difference-in-differences estimation, or instrumental variable approaches could help isolate causal effects more precisely. Such approaches would allow for stronger generalizations and provide additional insights into whether CVC-backed firms systematically outperform their peers.

Second, while this study concentrated on the Thai sport-tech sector, findings should be interpreted in the context of an emerging economy with unique institutional and cultural characteristics. Extending the analysis to other regional markets, such as Southeast Asia or Latin America, would provide comparative insights and test the generalizability of the mechanisms identified here.

Finally, the present research relied primarily on secondary data sources such as corporate disclosures, industry reports, and government records. Future studies could benefit from combining such data with primary qualitative evidence, including interviews with managers and investors, to capture the nuanced dynamics of knowledge transfer, strategic alignment, and cultural proximity in CVC partnerships.

By addressing these limitations, future scholarship can advance the understanding of how CVC contributes to innovation and internationalization across different sectors and institutional environments, and provide stronger guidance for corporate managers, entrepreneurs, and policymakers.

Conclusion

This study examined how different orientations of corporate venture capital (CVC) investment are associated with the strategic development of sport-tech firms in Thailand, with particular attention to technology portfolio diversification and international market expansion. Drawing on the interorganizational learning perspective, the empirical analysis indicates that technology-oriented CVC is positively associated with broader technology portfolios, while foreign-oriented CVC is positively associated with wider geographic market presence. At the same time, the findings show that the strength of these relationships varies depending on the level of industry and cultural distance between investors and portfolio firms. These results suggest that corporate venture capital partnerships may provide channels for technological learning and international network access, but their effectiveness appears to depend on the degree of contextual alignment between collaborating organizations.

The study makes several contributions to the literature on corporate venture capital and emerging-market entrepreneurship. First, it extends existing CVC research to the sport-tech sector, an industry that has received limited attention in prior studies despite its growing economic and technological significance. Second, the research advances understanding of how different orientations of CVC investment are associated with distinct strategic outcomes, including technological diversification and international market expansion. Third, by incorporating the moderating roles of industry distance and cultural distance, the study highlights how relational and contextual factors shape the potential benefits of investment partnerships within emerging innovation ecosystems.

The findings also provide insights for practice. Entrepreneurs may benefit from evaluating corporate investors not only in terms of financial capital but also in terms of technological compatibility and international network access. Corporate investors may improve collaboration outcomes by forming partnerships with firms whose technological focus and organizational context are compatible with their own capabilities. In addition, policymakers seeking to promote innovation-driven growth may consider initiatives that strengthen corporate–startup collaboration, international investment networks, and the absorptive capacity of entrepreneurial firms.

At the same time, several limitations should be acknowledged. The dataset includes only Thai sport-tech firms that received corporate venture capital investment, and the absence of a matched control group of non-CVC-backed firms limits the ability to make strong causal claims. This reflects the limited availability of reliable data on non-funded sport-tech enterprises in Thailand. Future research may address this limitation by employing quasi-experimental approaches, such as propensity score matching or difference-in-differences estimation, and by expanding the analysis to cross-country samples to examine whether similar patterns emerge across different institutional contexts.

Overall, the study suggests that corporate venture capital may function as an important mechanism connecting entrepreneurial firms to external technological knowledge and international business networks. In emerging innovation ecosystems such as Thailand’s sport-tech sector, the strategic value of CVC partnerships appears to depend not only on the availability of investment capital but also on the degree of industry compatibility, cultural proximity, and collaborative learning between investors and entrepreneurial firms.

Declaration of Generative AI Use

Generative AI tools (specifically, ChatGPT by OpenAI) were used only for grammatical correction and language polishing of the manuscript. No part of the conceptualization, analysis, interpretation, or substantive content was generated by AI. The authors have carefully reviewed all language edits and take full responsibility for the content of this manuscript.

References