Organizations and Markets in Emerging Economies ISSN 2029-4581 eISSN 2345-0037

2026, vol. 17, no. 1(34), pp. 95–116 DOI: https://doi.org/10.15388/omee.2026.17.5

Green Banking and Sustainability Disclosures in the Islamic Banking Sector: Evidence from Malaysia

Mohd Faizuddin Muhammad Zuki (corresponding author)

Islamic Business School, College of Business, Universiti Utara Malaysia, Malaysia

m.faizuddin@uum.edu.my

Muhammad Arif Fadilah Ishak

Faculty of Quranic Science, UCYP University, Malaysia

ariffadilah@ucyp.edu.my

Muhammad Hafiz Hassan

Faculty of Muamalat, Management and Technology,

Universiti Islam Antarabangsa Tuanku Syed Sirajuddin, Malaysia

muhammadhafiz@unisiraj.edu.my

Abstract. The heightened global focus on sustainability has intensified expectations for financial institutions, including Islamic banks, to embed green finance and sustainable practices within their operations. Although Malaysia remains a global leader in Islamic finance, questions persist regarding the depth of sustainability implementation beyond narrative disclosure. This study examines the extent to which full-fledged Islamic banks in Malaysia operationalize green finance and sustainability principles, and evaluates their alignment with national and global frameworks. A qualitative exploratory design was employed, incorporating systematic content analysis and thematic review of sustainability, annual, and integrated reports from six Islamic commercial and development banks. To enhance rigor, a triangulation strategy validated findings against academic literature, regulatory documents, and institutional policy sources. In addition, a quantitative content analysis was conducted through a structured 0–4 scoring rubric applied across fifteen indicators, generating a Green Banking and Sustainability Index (GBSI) scaled to 0–100. The results reveal four emerging themes–climate risk management, compliance with sustainability frameworks, environmental footprint reduction, and green financing activities, with banks demonstrating varying maturity across initiatives. GBSI scores ranged from 40.3 to 66.7, indicating moderate progress yet uneven adoption across institutions. Positive strides were noted in energy efficiency, digitalisation, and initial climate-disclosure efforts, while gaps remain in renewable energy deployment, green procurement, verified performance metrics, and standardised reporting. This study contributes empirical insight into ESG integration within Islamic banking, advances legitimacy theory and provides actionable recommendations to strengthen execution consistency, enhance reporting quality, and support Malaysia’s strategic ambition in Islamic green finance.

Keywords: green banking, sustainability, ESG, Islamic banks, disclosure

Received: 3/11/2025. Accepted: 27/4/2026

Copyright © 2026 Mohd Faizuddin Muhammad Zuki, Muhammad Arif Fadilah Ishak, Muhammad Hafiz Hassan. Published by Vilnius University Press. This is an Open Access article distributed under the terms of the Creative Commons Attribution Licence, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

1. Introduction

Environmental degradation and the depletion of natural resources represent critical challenges that demand global attention, catalysing the adoption of green banking and sustainability practices as a viable solution (Bukhari et al., 2020). Green banking represents a paradigm shift in the banking sector, integrating environmental considerations into operational and strategic decision-making processes (Fajriah et al., 2023). Stakeholder engagement emerges as a central issue for both conventional and Islamic banking institutions in the pursuit of green banking initiatives, highlighting the necessity for inclusive and collaborative strategies (Bukhari et al., 2020). The move towards sustainability necessitates the alignment of financial practices with environmental protection, resource conservation, and social responsibility, underscoring the crucial role of financial institutions in fostering a more sustainable future.

Banks are now transitioning their behaviour by implementing green banking concepts to minimize their environmental impact (Hermala et al., 2024). This transition involves a multifaceted approach, integrating environmentally conscious operational adjustments, such as the adoption of recycled paper products to mitigate deforestation and minimize waste generation, with the introduction of pioneering financial instruments, including green credit cards that offer targeted incentives and benefits to promote environmentally responsible actions. These efforts aim to cultivate a widespread ethos of environmental stewardship among both consumers and commercial entities (Chowdhury et al., 2025).

The urgency to address climate change, coupled with the increasing awareness of environmental degradation, has spurred the financial sector to adopt sustainable practices, with green banking at the forefront. Islamic banking, guided by the principles of Shariah, emphasizes social justice, ethical conduct, and environmental stewardship—values that align well with the goals of sustainable development. Islamic financial instruments, such as zakat, waqf, and microfinance, possess the capacity to enhance social well-being and reduce poverty. This highlights how Islamic finance not only offers economic advantages but also reinforces social and environmental responsibilities that align with ESG principles (Budiman et al., 2021). Integrating ESG principles into Islamic finance practices necessitates the issuance of fatwas that provide a legal framework for guiding the implementation of ethical investments. Islamic banks distinguish themselves through a profound commitment to sustainability, tangibly demonstrated through the proactive integration of environmental considerations into their operational frameworks and a steadfast adherence to ethical guidelines enshrined in Shariah law. This convergence underscores the intrinsic compatibility between Islamic finance and the global movement toward environmental preservation and responsible financial practices, positioning these institutions as key drivers in fostering a more sustainable and equitable financial ecosystem.

Despite this promising alignment between Islamic finance and sustainable development goals, several critical challenges remain. The first is the lack of systematic assessment of green finance initiatives. While Islamic banks, grounded in Shariah principles, have the potential to significantly contribute to climate finance solutions (Obaidullah, 2017), there remains a dearth of comprehensive studies evaluating their green efforts (Andatu & Hilabi, 2023). Islamic financial principles, which advocate justice, fairness, and the preservation of resources, naturally align with environmental protection and sustainable development (Al‐Roubaie & Sarea, 2019), yet empirical evaluations are scarce. Second, the fragmented nature of sustainability reporting and inconsistent practices among Islamic banks hinder efforts to benchmark performance or establish industry-wide standards. Existing reports often lack standardization, and application of sustainability principles varies, resulting in outcomes that are difficult to measure or compare. Third, there exists a gap between marketing claims and actual sustainability performance. Accusations of “greenwashing” have surfaced, where banks promote environmental initiatives in public relations materials without substantive changes in operations (Accenture, 2022). This discrepancy threatens public trust and undermines the credibility of Islamic finance in championing sustainability.

Although no banks fully meet green policy requirements, studies suggest Islamic banks show more seriousness than their conventional counterparts (Julia & Kassim, 2019). This may stem from their inherently ethical framework, which emphasizes environmental and social responsibility (Bukhari et al., 2019). Therefore, further research is imperative to dissect the methodologies Islamic banks are adopting, evaluate their efficacy, and identify areas for improvement, ultimately to inform best practices and support the industry’s transition towards a more ecologically conscious banking model. To provide a strong theoretical foundation, this study adopts legitimacy theory as its guiding lens. Legitimacy theory posits that organizations seek to maintain societal approval by aligning their activities and disclosures with stakeholder expectations (Deegan, 2002; Suchman, 1995). This perspective is particularly relevant to Islamic banks, where sustainability reporting often reflects a tension between symbolic compliance and substantive implementation.

Recent studies highlight that sustainability disclosures in the banking sector are frequently shaped by legitimacy concerns, with reporting practices sometimes serving more as symbolic gestures than substantive environmental commitments (Firmansyah & Kartiko, 2024; Sebastião et al., 2024). By applying legitimacy theory, the study interprets why banks adopt sustainability frameworks, why disclosure frequently outpaces actual practice, and why standardized indicators remain limited. The selection of legitimacy theory adheres to the IMPACT framework for theory selection, offering interpretive power in explaining disclosure practices, meaningful relevance to Islamic finance, predictive capacity regarding risks of greenwashing, broad applicability across institutional contexts, coherence with the study’s central argument, and transferability to other emerging economies.

Despite the growing body of literature on green banking and sustainability, there remains a notable research gap in systematically evaluating the extent to which Islamic banks move beyond disclosure to actual implementation of sustainability practices. Prior studies have often focused on disclosure quality or broad ESG adoption without critically examining the depth of integration into operational frameworks. This study addresses that gap by assessing both the nature and substance of sustainability initiatives within Malaysia’s full-fledged Islamic banks, thereby contributing new empirical evidence to the discourse on Islamic green finance. The novelty of this research lies in the emergence of four key themes, climate risk management, compliance with national and global frameworks, environmental footprint reduction, and green financing activities, further broken down into fifteen specific indicators. The findings are expected to enrich the literature on Islamic green finance while offering practical insights for regulators and practitioners to strengthen policy coherence, disclosure practices, and sustainability performance in the sector.

Malaysia offers a particularly significant context for this study. As one of the world’s leading Islamic finance hubs, Malaysia hosts a dual banking system where Islamic banks play a central role in advancing financial inclusion and sustainable development. The country has pioneered regulatory frameworks such as the Value-Based Intermediation (VBI) initiative and the Climate Change and Principle-Based Taxonomy (CCPT), which position Islamic banks at the forefront of sustainability integration. This context underscores Malaysia’s importance as both a testing ground and a benchmark for how Islamic banking can align with global sustainability agendas while remaining rooted in Shariah principles.

2. Literature Review

2.1 Conceptualizing Green Banking and Sustainability in Banking

The integration of Environmental, Social, and Governance (ESG) principles into the financial sector has become a critical strategy for fostering sustainable development. In particular, Islamic banking, with its emphasis on ethical and socially responsible investing, offers a strong foundation for aligning financial operations with sustainability goals (Bukhari et al., 2019; Salsabila et al., 2022). Financial institutions are increasingly seen as agents of change in addressing climate-related challenges by directing capital toward environmentally and socially impactful sectors (Rahman et al., 2022). This growing role is driven not only by regulatory pressures but also by stakeholder expectations and international climate accords that emphasize carbon reduction and responsible investment.

This paradigm shift necessitates a new orientation in banking practices where financial institutions are expected to generate both financial returns and positive environmental externalities. Green finance, in this regard, has emerged as a critical tool, aiming to embed sustainability into core banking functions such as lending, investment, and risk management (Muchiri et al., 2025). Notably, Islamic banking offers a unique advantage in operationalizing green finance through its Shariah principles. The prohibition of riba (interest) and gharar (excessive uncertainty), alongside the emphasis on social justice and stewardship (khalifah), position Islamic finance as a naturally aligned system with sustainability objectives.

Green banking, which refers to the integration of environmental considerations into financial decisions, goes beyond regulatory compliance. It entails the strategic reorientation of banking operations to actively support environmental preservation, resource efficiency, and sustainable development. This includes financing renewable energy projects, clean transportation, green technology, and sustainable agriculture, sectors that directly contribute to a low-carbon economy (Anggraini & Muhammad Iqbal, 2022; Zhixia et al., 2018). Banks engaging in such initiatives are increasingly contributing to both ecological resilience and long-term profitability, particularly as consumer and investor preferences shift toward ESG-conscious institutions.

However, the transition from traditional to sustainability-oriented banking is not without challenges. Issues such as greenwashing, fragmented regulatory guidelines, inconsistent disclosure practices, and a lack of standardized green finance taxonomy limit the full potential of green banking initiatives (Institute for Capital Market Research Malaysia, 2023; Muchiri et al., 2025; Sebastião et al., 2024). Moreover, for Islamic banks, operationalizing green finance in alignment with Maqasid al-Shariah still requires further clarity in terms of implementation, product innovation, and measurable impact. Therefore, while the conceptual foundation of green finance in banking is robust and evolving, its effective application necessitates continued strategic, regulatory, and institutional development to drive systemic change across the sector.

2.2 Islamic Finance and ESG Integration

Islamic finance is inherently aligned with ethical and responsible investing due to its foundational principles derived from Shariah law. These principles emphasize fairness, risk-sharing, and the prohibition of activities harmful to society and the environment, such as those involving riba (interest), gharar (excessive uncertainty), and maysir (gambling). This ethical orientation closely mirrors the values promoted under Environmental, Social, and Governance (ESG) frameworks, which seek to create sustainable and socially responsible economic systems (Bukhari et al., 2019; Qoyum et al., 2022). As such, Islamic finance presents a natural framework for supporting ESG integration, especially in predominantly Muslim regions where Shariah-compliant financial products are widely accepted. This intrinsic alignment allows Islamic financial institutions to seamlessly embed green and sustainability practices into their operational frameworks, thereby distinguishing their approach from that of conventional counterparts (Andatu & Hilabi, 2023).

The integration of ESG into Islamic finance is not just a theoretical proposition but is increasingly evident in practice. For instance, the emergence of green sukuk serves as a critical milestone in demonstrating the compatibility between Islamic finance and sustainability objectives. Green sukuk enable capital raising for projects that have clear environmental benefits while maintaining Shariah compliance. Malaysia and Indonesia have been pioneers in this space, launching sovereign and corporate green sukuk to fund renewable energy, energy efficiency, and low-carbon transport infrastructure. These instruments showcase how Islamic finance can contribute to the global sustainability agenda (Araminta et al., 2022), particularly in aligning financial flows with the Sustainable Development Goals (SDGs) and the Paris Climate Agreement. The rigorous screening processes inherent in Islamic finance, which prohibit investments in industries deemed unethical or harmful, naturally filter out many environmentally and socially detrimental activities, reinforcing their commitment to responsible finance (Liu & Lai, 2021).

Despite these promising developments, several challenges hinder the widespread integration of ESG within Islamic financial institutions. A key concern is the lack of standardized ESG metrics that are compatible with Shariah guidelines. While conventional ESG scoring systems exist, they often fail to account for the unique ethical filters and prohibitions in Islamic finance. This mismatch creates difficulties for Islamic banks in benchmarking their sustainability performance relative to global peers. Moreover, the risk of greenwashing, where financial institutions overstate or misrepresent the environmental impact of their activities, is a growing concern. Without proper oversight and disclosure standards, the credibility of ESG claims may be compromised, particularly in markets where regulatory frameworks are still evolving.

Another critical issue is the operationalization of Maqasid al-Shariah, the higher objectives of Islamic law, as a framework for assessing sustainability. While scholars have proposed that Maqasid align with the pillars of ESG (Qoyum et al., 2022), there remains limited empirical evidence on how Islamic banks incorporate these objectives into their governance, risk management, and product development processes. The absence of measurable benchmarks for Maqasid-driven ESG practices makes it difficult to evaluate their effectiveness in promoting sustainability. Furthermore, the adoption of ESG practices varies widely across Islamic financial institutions, depending on their size, regulatory context, and strategic priorities. While the ethical underpinnings of Islamic finance provide a strong basis for ESG integration, there is a pressing need to bridge conceptual ideals with institutional practices. This requires the development of Shariah-compatible ESG indicators, increased regulatory clarity, and a commitment to transparency and accountability.

2.3 Legitimacy Theory as a Guiding Framework

Legitimacy theory provides a critical lens for analyzing sustainability disclosures in the banking sector. It posits that organizations seek to maintain societal approval by aligning their activities, narratives, and reporting with stakeholder expectations (Deegan, 2002; Suchman, 1995). Within the context of Islamic banking, this perspective is particularly relevant given the sector’s dual responsibility to uphold Shariah principles and respond to global sustainability demands.

Recent past studies demonstrate that sustainability reporting often reflects legitimacy-seeking behaviour, where disclosures are used strategically to signal compliance with societal norms rather than to document substantive environmental performance. For instance, Sebastião et al. (2024) highlight that banking institutions frequently adopt sustainability frameworks to enhance legitimacy, even when implementation remains uneven. Similarly, Firmansyah and Kartiko (2024) and Islam and Kokubu (2018) show that green banking disclosures can serve symbolic functions, with firm size and age moderating the extent of substantive adoption. These findings resonate with concerns about “greenwashing,” where banks emphasize environmental narratives without embedding them into operational practices (Cho et al., 2015; Michelon et al., 2015).

Applying legitimacy theory to Islamic banking thus enables a deeper understanding of why disclosure often outpaces actual practice, why standardized indicators remain limited, and how banks balance symbolic compliance with substantive integration. The selection of legitimacy theory adheres to the IMPACT framework for theory selection (Hollebeek et al., 2025), as it offers interpretive power in explaining disclosure practices, meaningful relevance to Islamic finance, predictive capacity regarding risks of greenwashing, broad applicability across institutional contexts, coherence with the study’s central argument, and transferability to other emerging economies.

The first element of the IMPACT framework, Interestingness, arises from the tension between symbolic disclosure and substantive implementation in Islamic banking sustainability, a phenomenon that has not been systematically examined. Second, Matching is achieved as legitimacy theory directly explains why banks disclose sustainability practices to maintain societal approval, even when implementation remains partial. Third, Parsimony is reflected in the theory’s ability to provide a coherent explanation without requiring multiple overlapping frameworks. Fourth, Applicability is evident in its relevance across diverse institutional contexts, including Islamic finance in Malaysia. Fifth, Conceptual Rigor is ensured through established scholarly foundations (Deegan, 2002; Suchman, 1995), which provide interpretive depth for disclosure practices. Finally, Testability is supported by the operationalization of sustainability indicators within the Green Banking and Sustainability Index (GBSI), allowing empirical assessment of symbolic versus substantive practices.

3. Methodology

This study adopts an exploratory qualitative research design to examine the extent and maturity of green finance and sustainability implementation among Malaysian Islamic banks. Exploratory qualitative designs are appropriate for emerging domains where empirical structures are still forming and where rich contextual understanding is required (Creswell & Creswell, 2022). Consistent with sustainability reporting works, the study employs a systematic content analysis of narrative disclosures, an approach widely used in ESG and banking studies to analyse corporate sustainability practices (Hamidi & Worthington, 2021; Kurniawati, 2025; Vőneki & Lamanda, 2020). Document-based qualitative research is particularly suited to examining institutional behaviour and policy alignment in regulated financial sectors, where public narratives provide strategic and compliance signals (Hahn & Kühnen, 2013).

The sample consists of all six full-fledged Islamic banks in Malaysia, Bank Islam, Bank Muamalat, Bank Rakyat, BSN, MBSB, and Bank Agro. These banks were selected due to their complete Shariah-compliant mandate and relevance to Islamic sustainable finance and policy priorities in Malaysia. Data were extracted from annual reports, sustainability reports, and integrated reports, consistent with prior studies on sustainability disclosure practices in banking and Islamic finance (Hamidi & Worthington, 2021; Kurniawati, 2025; Vőneki & Lamanda, 2020). Only publicly available and verifiable reports were analysed to ensure transparency and replicability, in line with established qualitative research protocols for document analysis (Bowen, 2009).

A hybrid inductive–deductive thematic analysis was applied to identify and classify green finance and sustainability practices. Deductive coding was guided by established frameworks such as BNM’s Climate Change and Principle-based Taxonomy (CCPT), the Task Force on Climate-related Financial Disclosures (TCFD), the UN Sustainable Development Goals (SDGs), and the Value-Based Intermediation (VBI) initiative. Deductive approaches grounded in regulatory and theoretical frameworks are widely recommended in ESG scholarship to ensure conceptual alignment and analytical coherence (Braun & Clarke, 2006; Fereday & Muir-Cochrane, 2006). Complementing this, inductive coding allowed themes to emerge organically from the data, reflecting evolving industry practices, as recommended in qualitative sustainability research (Kyngäs, 2020; Pipere et al., 2010; Spetic et al., 2012).

To strengthen methodological rigor, enhance comparability across institutions and ensure the replicability, the qualitative coding was complemented with quantitative content analysis. Each indicator was scored using a structured 0–4 maturity scale, where 0 = no disclosure; 1 = minimal mention without detail; 2 = disclosure with qualitative description; 3 = disclosure with quantitative evidence; 4 = disclosure with measurable outcomes and external assurance. The scale was adapted from established content analysis frameworks in sustainability accounting and green finance research (Krippendorff, 2019). This scoring approach reflects common practice in ESG assessment studies, which increasingly combine qualitative insights with quantitative indices to evaluate implementation depth and maturity (Hamidi & Worthington, 2021; Kurniawati, 2025; Vőneki & Lamanda, 2020).

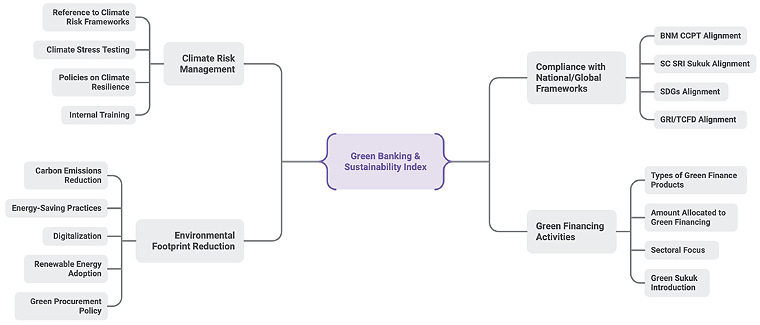

Each theme score was calculated as the average of its respective indicators. The overall Green Banking and Sustainability Index (GBSI) was then derived as the average of all fifteen indicators across the four themes, divided by 15 (the total number of indicators), and multiplied by 100 to normalize results to a 0–100 scale. This normalization ensures comparability across banks by placing results on a standardized benchmark. No weighting was applied, meaning each indicator contributes equally to the overall score. Figure 1 below summarizes the developed themes–indicators of the Green Banking and Sustainability Index.

Figure 1

The Themes–Indicators of the GBSI

4. Results and Analysis

4.1 Green Banking and Sustainability Index (GBSI)

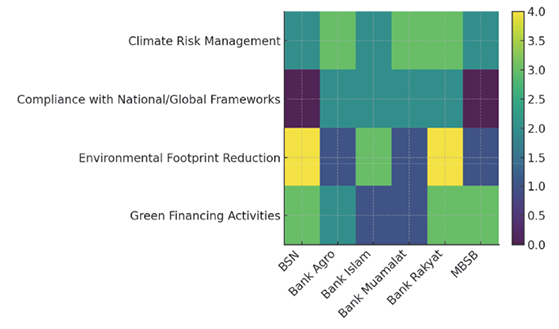

To complement the qualitative content analysis, a quantitative Green Banking and Sustainability Index (GBSI) was developed to assess the maturity of sustainability practices across the six Islamic banks. Using a structured 0–4 scoring rubric converted into a 0–100 scale, the GBSI results reveal a moderate and uneven level of sustainability integration across institutions. Scores range from 40.3 to 66.7, suggesting that while progress is evident, sustainability maturity remains in a developing phase. Table 1 and Figure 2 below present the scoring and the heatmap of the green banking and sustainability practices of the Islamic banking.

Table 1

Green Banking and Sustainability Index

|

Bank |

Main Theme |

Score |

Overall Score |

|---|---|---|---|

|

Bank Agro |

Climate Risk Management |

3.0 |

45.7 |

|

Compliance with National/Global Frameworks |

2.0 |

||

|

Environmental Footprint Reduction |

1.0 |

||

|

Green Financing Activities |

2.0 |

||

|

Bank Islam |

Climate Risk Management |

2.0 |

63.0 |

|

Compliance with National/Global Frameworks |

3.0 |

||

|

Environmental Footprint Reduction |

2.0 |

||

|

Green Financing Activities |

3.0 |

||

|

Bank |

Climate Risk Management |

2.0 |

44.3 |

|

Compliance with National/Global Frameworks |

2.0 |

||

|

Environmental Footprint Reduction |

1.0 |

||

|

Green Financing Activities |

2.0 |

||

|

Bank Rakyat |

Climate Risk Management |

3.0 |

66.7 |

|

Compliance with National/Global Frameworks |

2.0 |

||

|

Environmental Footprint Reduction |

3.0 |

||

|

Green Financing Activities |

2.0 |

||

|

BSN |

Climate Risk Management |

1.0 |

40.3 |

|

Compliance with National/Global Frameworks |

1.0 |

||

|

Environmental Footprint Reduction |

2.0 |

||

|

Green Financing Activities |

2.0 |

||

|

MBSB |

Climate Risk Management |

2.0 |

56.0 |

|

Compliance with National/Global Frameworks |

1.0 |

||

|

Environmental Footprint Reduction |

2.0 |

||

|

Green Financing Activities |

3.0 |

The analysis reveals notable variation in the maturity of green finance and sustainability practices among Malaysian full-fledged Islamic banks. The computed Green Banking and Sustainability Index scores range from 40.3 to 66.7 out of 100, suggesting that sector-wide progress is ongoing, yet still positioned at an evolving rather than fully institutionalized stage. Bank Rakyat records the highest score (66.7), followed closely by Bank Islam (63.0) and MBSB (56.0), indicating more established integration of sustainability policies and financing programs. In contrast, Bank Agro (45.7), Bank Muamalat (44.3), and BSN (40.3) reflect more nascent adoption, particularly in areas requiring verified outcomes and measurable climate impact.

Figure 2

Green Banking and Sustainability Index

Table 2

Theme-Level Performance

|

Theme |

Highest Score |

Lowest Score |

Trend Insight |

|---|---|---|---|

|

Climate Risk Management |

Bank Rakyat / |

BSN = 1 |

Governance efforts growing; execution uneven |

|

Compliance with National/Global Frameworks |

Bank Islam = 2 |

BSN & MBSB = 1 |

Framework commitment exists; gaps in assurance & reporting |

|

Environmental Footprint Reduction |

Bank Rakyat = 3 |

Bank Agro, & Bank Muamalat = 1 |

Strong efficiency programs; renewables adoption limited |

|

Green Financing Activities |

Bank Islam & MBSB = 3 |

Bank Muamalat / Bank Rakyat / Bank Agro / BSN = 2 |

Product variety growing; allocation disclosure inconsistent |

The theme-level analysis highlights uneven progress among Islamic banks in embedding sustainability practices. In Climate Risk Management, Bank Rakyat and Bank Agro lead with scores of 3, reflecting stronger governance structures and resilience policies, while BSN lags at 1, indicating limited execution despite growing sectoral attention. For Compliance with National and Global Frameworks, Bank Islam stands out with a score of 2, showing more consistent alignment with CCPT and TCFD, whereas BSN and MBSB remain at 1, suggesting that while framework commitments exist, assurance and reporting practices are still underdeveloped. In Environmental Footprint Reduction, Bank Rakyat again performs best (score 3) due to robust efficiency programs, but Bank Agro and Bank Muamalat trail at 1, underscoring that renewable energy adoption and broader footprint reduction remain limited. Finally, in Green Financing Activities, Bank Islam and MBSB achieve the highest scores (3), reflecting diversified product offerings and larger allocations, while the other banks score 2, pointing to growth in product variety but inconsistent disclosure of allocation details.

4.2 Thematic Results

Based on the content analysis and review of existing academic literature and publicly available documents, including annual reports, sustainability reports, and integrated reports of the selected Islamic banks, coupled with a thematic analysis approach, four main themes were identified. These themes are: (1) Climate Risk Management, (2) Compliance with Global and National Frameworks, (3) Environmental Footprint Reduction, and (4) Green Financing Activities. Furthermore, these main themes are supported by a total of 15 specific indicators that collectively represent the green and sustainability practices observed among the institutions.

4.2.1 Climate Risk Management

All six Islamic banks referenced at least one climate risk framework, most notably the Task Force on Climate-related Financial Disclosures (TCFD), Bank Negara Malaysia’s Climate Risk Management and Scenario Analysis (CRMSA), and Climate Change and Principle-based Taxonomy (CCPT). Bank Islam, Bank Rakyat, Bank Simpanan Nasional (BSN), MBSB Bank, and Agrobank explicitly refer to TCFD recommendations, indicating their efforts to align with globally recognized disclosure standards (Agrobank, 2023; Bank Islam, 2024; Bank Rakyat, 2023; BSN, 2023; MBSB, 2024). In contrast, Bank Muamalat emphasizes its compliance with BNM’s CCPT and CRMSA and incorporates an ESG scorecard in non-retail financing but does not explicitly mention TCFD (Bank Muamalat, 2023). Agrobank stands out for integrating climate frameworks into its Strategic Business Plan 2021–2025, showing a deeper strategic alignment (Agrobank, 2023). This suggests a clear distinction between banks that are primarily compliance-driven versus those with a more strategic orientation toward climate governance.

With regard to climate stress testing or scenario analysis, all six banks have initiated some form of assessment, although the scope and depth vary. MBSB Bank and BSN are more advanced, with MBSB conducting a 2.5°C scenario analysis for high-emitting sectors and establishing climate-related exposure limits. BSN, meanwhile, applied Representative Concentration Pathway (RCP) 8.5 scenarios to assess operational vulnerabilities across its branch network and factored climate risk into stress testing for home financing and microbusiness portfolios. Agrobank and Bank Muamalat have begun incorporating climate-linked scenarios, including flood risk, into stress testing exercises. Bank Islam and Bank Rakyat have completed gap analyses aligned with BNM’s climate risk stress testing guidance, which is a positive step toward full implementation but still preliminary compared to other banks.

For the third indicator, policies on climate resilience, all banks except BSN have developed relevant policies or frameworks. Bank Islam and Bank Muamalat have formalized climate risk management frameworks guided by BNM’s taxonomy. MBSB Bank has developed a Sustainable and Transition Finance Framework, adopted VBI Sectoral Guides, and is working on internal validation of its climate risk scenario models. These efforts demonstrate a commitment to integrating climate risk within governance and credit assessment structures. Agrobank and Bank Rakyat are also aligning their risk management policies with CRMSA, with Agrobank enhancing its Risk Appetite Statement (RAS) and Risk Acceptance Criteria (RAC) to address climate-related risks.

The fourth indicator, internal training and capacity building, is the area with the least reported progress. Except for Bank Rakyat and Agrobank, all other banks marked this indicator as “N/A,” indicating that either no internal ESG-related training programs have been reported or such initiatives are not yet in place. Bank Rakyat mentioned general staff upskilling, while Agrobank provides a more structured and comprehensive approach, including institution-wide sustainability awareness campaigns, the establishment of a Sustainability Discussion Group (SDG), and targeted employee learning modules covering topics such as VBI, CCPT, and responsible resource use. The limited focus on training across most banks signals a critical gap in internal capacity development, which is essential for implementing sustainability strategies effectively across all levels of an organization (Hahn & Kühnen, 2013).

The findings show that while all six banks are making efforts toward climate risk management, their progress is uneven across the four indicators. Agrobank, MBSB Bank, and Bank Islam are more advanced in terms of strategic integration, policy development, and stress testing, while BSN and Bank Muamalat demonstrate more fragmented or nascent practices. Internal capacity building remains a major weakness, suggesting a need for greater investment in training and awareness initiatives. This reinforces the importance of moving from compliance-based disclosure toward embedded, organization-wide climate risk governance, aligned with both national and international frameworks (Bank Negara Malaysia, 2021; Financial Stability Board, 2015).

4.2.2 Compliance with Global and National Frameworks

The second main theme, Compliance with National/Global Frameworks, involves two specific indicators: (1) alignment with Bank Negara Malaysia’s Climate Change and Principle-Based Taxonomy (CCPT) or the Securities Commission’s Sustainable and Responsible Investment (SRI) Sukuk Framework, and (2) alignment with global sustainability reporting standards, particularly the Sustainable Development Goals (SDGs), Global Reporting Initiative (GRI), and the Task Force on Climate-related Financial Disclosures (TCFD). The findings reflect varying degrees of regulatory compliance and strategic alignment across Islamic banks in Malaysia.

Under the first indicator, alignment with CCPT or SRI Sukuk frameworks, four out of six banks demonstrate some level of commitment to integrating BNM’s CCPT into their financing and sustainability assessments. Bank Muamalat stands out by integrating an ESG scorecard based on CCPT Guiding Principles (GP3 & GP4) and updating sectoral guidelines to include due diligence at both the transactional and entity levels. Bank Islam, Bank Rakyat, and Agrobank also report alignment with CCPT to varying degrees, primarily for classification of exposures and guiding their green finance initiatives. However, MBSB and BSN did not disclose any related activities, suggesting a potential compliance or strategic gap in implementing taxonomy-based climate risk evaluation. This inconsistency highlights the need for industry-wide guidance and standardized implementation of CCPT to ensure uniformity and accountability (Bank Negara Malaysia, 2021).

The second indicator, alignment with SDGs, GRI, or TCFD, shows broader compliance across all banks, with more comprehensive disclosures. Bank Islam and Bank Muamalat undertook materiality assessments and structured their sustainability reporting in accordance with GRI standards and other market benchmarks such as FTSE4Good and Bursa Malaysia guidelines. MBSB, BSN, and Agrobank also referenced TCFD and GRI frameworks in their sustainability reports. Notably, Bank Rakyat has committed to fully adopt TCFD disclosures by FY2024, signalling its effort to enhance transparency and climate risk governance. Several banks, such as Bank Muamalat and Bank Rakyat, are also active participants in the Joint Committee on Climate Change (JC3), a collaborative regulator-industry platform, showing their engagement in national-level climate finance policymaking.

Despite the promising adoption of international standards, the level of depth and strategic integration varies. Some banks mention frameworks superficially, while others embed them into performance reviews and policy documents. The lack of uniform materiality reporting or quantifiable sustainability targets indicates that banks are still in transition from voluntary alignment to structured implementation. This aligns with observations by Hahn and Kühnen (2013), who argued that sustainability disclosures are often driven by legitimacy concerns rather than internalized corporate responsibility unless guided by strong regulatory frameworks. While most Islamic banks have acknowledged or adopted global and national sustainability frameworks, there remains a disparity in implementation depth and reporting quality. The findings call for a more consistent, transparent, and performance-based reporting model to enable benchmarking and improve the accountability of Islamic financial institutions in supporting Malaysia’s sustainable finance agenda.

4.2.3 Environmental Footprint Reduction

Based on the content analysis of the third main theme, Environmental Footprint Reduction, five specific indicators were examined: (1) carbon emissions reduction initiatives, (2) energy-saving or efficiency practices, (3) digitalization or paperless banking, (4) adoption of renewable energy, and (5) green procurement policy. The analysis reveals diverse levels of commitment and implementation across Islamic banks in Malaysia, reflecting both commendable progress and critical gaps. In terms of carbon emissions reduction, all banks, except for Agrobank, which focused primarily on responsible waste disposal, demonstrated varying efforts. Bank Muamalat and Bank Rakyat initiated technical upgrades such as switching to LED lighting and transitioning from desktops to energy-efficient laptops, while MBSB took a more comprehensive approach by calculating Scope 3 financed emissions and outlining a Net Zero Roadmap. BSN notably became the first development financial institution (DFI) in Malaysia to establish a GHG inventory verified under ISO 14064-3:2019, indicating a commitment to measurable and standardized reporting. Bank Islam stood out with its introduction of environment-friendly branches powered by solar energy and rainwater harvesting systems, demonstrating an institutional-level integration of sustainability objectives.

Regarding energy-saving or efficiency practices, all banks except Agrobank reported structured programs. These included LED retrofitting, HVAC system upgrades, and workspace consolidation strategies. MBSB and Bank Islam also introduced electric vehicle (EV) support infrastructure and water conservation mechanisms. Bank Rakyat’s efforts in recycling paper, plastic, and metals further reinforce its holistic approach to resource efficiency. On digitalization and paperless banking, progress was seen across all banks. MBSB, BSN, and Bank Muamalat implemented digital onboarding, virtual branches, and end-to-end paperless account opening. Bank Rakyat and Bank Islam took smaller steps, focusing on responsible paper usage and backend automation. Agrobank’s strategic transformation plan and digital subsidy distribution system highlighted the inclusive role of digital tools in financial outreach.

In contrast, the adoption of renewable energy remains limited. Only Bank Islam has significantly scaled up solar installations, while Bank Rakyat plans to launch pilot projects in FY2024. The remaining banks have not disclosed similar efforts, reflecting a sector-wide lag in renewable energy adoption, despite its alignment with national sustainability goals and the broader global climate agenda. The final indicator, green procurement policies, was addressed by only one bank, MBSB, which developed a Sustainable Supply Chain Framework and administered supplier assessments to evaluate ESG compliance. The absence of such policies across the other banks suggests a significant blind spot in embedding sustainability into upstream procurement decisions, consistent with findings from Hahn and Kühnen (2013), who noted that many institutions overlook supply chain sustainability in favour of internal operations.

Islamic banks in Malaysia have demonstrated encouraging progress in reducing their environmental footprint, particularly through initiatives in carbon emissions reduction, energy efficiency, and digital transformation. However, notable gaps remain in the areas of renewable energy adoption and the implementation of green procurement practices. These shortcomings highlight the need for more robust policy direction, standardized sectoral benchmarks, and a broader institutional commitment to climate-responsive strategies in order to advance comprehensive environmental sustainability within the Islamic banking sector.

4.2.4 Green Financing Activities

Based on the content analysis of the fourth main theme, Green Financing Activities, four specific indicators were assessed: (1) types of green finance products offered, (2) amount or percentage allocated to green financing, (3) sectoral focus of green financing, and (4) introduction of green sukuk or sustainability-linked sukuk. The findings indicate a growing commitment among Malaysian Islamic banks to support sustainability-driven financing, although the scope, scale, and instruments vary significantly across institutions.

For the first indicator, types of green finance products offered, all six banks reported the introduction or continuation of green-oriented products and facilities. These include electric vehicle (EV) financing, solar photovoltaic (PV) financing, eco-friendly home financing, and SME sustainability-linked loans. Banks such as Bank Islam and MBSB demonstrated more comprehensive offerings, with structured programmes such as the Low Carbon Transition Facility (LCTF), SME SMART Eco Financing Programme, and Sustainable Green Business Financing. BSN introduced unique retail-focused products like EcoSave-i, a green savings account, and offered solar panel financing for staff and customers, showcasing a people-centric approach. Agrobank focused on sector-specific sustainability programmes such as Climate Smart Agriculture and Agrotechnology Financing, aligning well with its development mandate.

In terms of the amount or percentage allocated to green financing, only four banks disclosed quantifiable data. Bank Islam leads in both total green financing volume and long-term targets, having achieved RM2.9 billion in green financing by 2021 with a strategic goal under its LEAP25 agenda. MBSB reported RM4.7 billion in sustainable and transition financing and significant disbursements for SME-driven decarbonization. Agrobank’s green financing constituted 9.9% of its overall portfolio in 2023, while Bank Rakyat allocated 60% of its ESG financing approvals to environment-focused projects. The lack of disclosure from BSN and limited data from Bank Muamalat reflects inconsistencies in measurement and transparency across the sector. On the third indicator, sectoral focus of green financing, banks broadly targeted renewable energy, EV financing, waste and water management, green-certified buildings, and agriculture. The most diversified portfolios were seen in MBSB and Bank Islam, while BSN and Bank Rakyat maintained a strong focus on mobility and solar financing. Agrobank’s concentration on SMEs and agri-modernization initiatives underscores its alignment with national development priorities, but also highlights the potential to expand further into other green sectors.

The final indicator, introduction of green sukuk or sustainability-linked sukuk, revealed limited activity. Only two banks, Bank Islam and MBSB, reported involvement in such instruments. Bank Islam played a key role as Joint Lead Manager in the Telekosang Hydro One ASEAN Green SRI Sukuk, while MBSB issued a Sustainability Sukuk Wakalah worth over RM300 million. Other banks did not report any participation in green sukuk issuance, indicating that this remains a largely untapped opportunity within Islamic banking, despite Malaysia’s leadership in the global sukuk market. This gap suggests the need for greater innovation and regulatory incentives to promote the development of Shariah-compliant ESG investment instruments (Alam et al., 2016; Bank Negara Malaysia, 2023; Institute for Capital Market Research Malaysia, 2023). In conclusion, while Islamic banks in Malaysia have made meaningful strides in offering green finance products and increasing their environmental financing portfolios, the adoption of green sukuk and consistent allocation reporting remain underdeveloped. The findings underscore the need for a standardized green finance taxonomy, enhanced product innovation, and strategic alignment across institutions to support Malaysia’s transition toward a low-carbon economy.

5. Conclusion and Implications

Based on the comprehensive analysis of the four main themes, climate risk management, compliance with frameworks, environmental footprint reduction, and green financing activities, the study concludes that Malaysian Islamic banks are progressively aligning their operations with sustainability goals, yet several critical gaps persist across implementation depth, standardization, and strategic integration. The results show that while many banks have adopted global and national climate risk frameworks such as TCFD and BNM’s CCPT, the degree of actual strategic integration and scenario analysis varies widely. Banks like MBSB, Agrobank, and Bank Islam demonstrate stronger institutional readiness, whereas others show preliminary or fragmented approaches. This supports the view of authors like Khan et al. (2015), who emphasize that mere adoption of disclosure frameworks without operational integration limits the impact of climate risk governance (Khan et al., 2015).

The study also finds inconsistent alignment with international frameworks such as the SDGs, GRI, and TCFD, and a lack of uniform sustainability reporting standards among Islamic banks. This reinforces earlier concerns raised by Hahn and Kühnen (2013) and Khattak et al. (2020) that sustainability disclosures in emerging markets are often superficial unless embedded within regulatory mandates and internalized governance structures. In terms of environmental footprint reduction, banks have made commendable progress in carbon reduction and digitalization, but lag in renewable energy adoption and green procurement policies. These areas require greater policy pressure and sectoral coordination to overcome inertia and resource constraints, echoing calls by UNEP Finance Initiative (2025) for more robust institutional mechanisms in green transformation (UNEP Finance Initiative, 2025).

On the green financing front, the introduction of green-focused products and services has expanded, with banks offering financing for solar, EV, and energy-efficient housing. However, the issuance of green or sustainability-linked sukuk remains limited, despite Malaysia’s global leadership in sukuk markets. This gap reflects the need for greater innovation in Shariah-compliant ESG instruments, as discussed by Alam et al. (2016) and Institute for Capital Market Research Malaysia (2023), and stronger incentives for Islamic banks to lead in ethical impact investing. The study contributes to the growing body of literature advocating for standardized green finance taxonomies, institutional ESG integration, and policy-driven innovation in Islamic finance. While Islamic banks in Malaysia are advancing on several fronts, they must shift from compliance-oriented approaches to strategic, measurable, and holistic sustainability integration to effectively contribute to Malaysia’s climate commitments and sustainable development agenda.

The findings of this study offer several practical implications for advancing green and sustainable finance within Malaysian Islamic banks. First, there is a pressing need for regulatory authorities, particularly Bank Negara Malaysia (BNM) and the Securities Commission (SC), to introduce a standardized and Shariah-compliant green finance taxonomy. A consistent framework would help Islamic banks uniformly define, measure, and report green finance initiatives, thereby reducing ambiguity and improving comparability (Khan et al., 2015; Martini & Creed, 2025; Sebastião et al., 2024). This is particularly critical given the fragmented adoption of sustainability indicators observed across the banks in this study (Sebastião et al., 2024). Secondly, banks should institutionalize climate risk governance by embedding climate scenario analyses into enterprise risk management systems and offering continuous capacity-building programs focused on ESG literacy. As suggested by Weber (2017), strengthening internal knowledge and governance structures is essential for embedding sustainability into banking operations (Weber, 2017). Training board members, risk officers, and operational staff on ESG and climate risks will foster greater organizational alignment with sustainability goals.

Third, the transition from voluntary to mandatory sustainability disclosures is recommended (Donner et al., 2025). Aligning reporting practices with globally recognized standards such as the Global Reporting Initiative (GRI), the Task Force on Climate-related Financial Disclosures (TCFD), and BNM’s Climate Change and Principle-based Taxonomy (CCPT) would enhance transparency and enable effective regulatory oversight (d’Aspremont, 2023; Hahn & Kühnen, 2013). Fourth, incentivizing green product innovation, particularly green sukuk and sustainability-linked Islamic finance instruments, can be supported through tax incentives or credit guarantees (Liu & Lai, 2021; Securities Commission Malaysia, 2019). This aligns with Euromoney (2021), who highlighted the role of regulatory support in scaling Shariah-compliant ESG instruments. Furthermore, the study underscores the importance of integrating green procurement practices and renewable energy adoption in bank operations, which remains underdeveloped among the sampled institutions. As noted, the transition to low-carbon operations is essential not only for reducing operational emissions but also for signalling long-term institutional commitment to sustainability (Stern & Valero, 2021). Participation in collaborative platforms such as the Joint Committee on Climate Change (JC3) could further support knowledge-sharing and benchmark setting across the industry.

Beyond its practical implications, this study also makes several theoretical contributions. First, it offers a theoretical extension of legitimacy theory into the domain of Islamic banking sustainability, demonstrating how disclosure practices can be interpreted through the lens of symbolic versus substantive legitimacy. Second, by developing and applying the Green Banking and Sustainability Index (GBSI), the study provides a replicable framework for operationalizing sustainability maturity in Islamic finance, thereby bridging theory with measurable practice. Third, the findings highlight a moderate level of theoretical novelty, as the study extends an established theory into a new institutional and cultural setting rather than proposing a new theory. Finally, the type of theoretical interestingness is noteworthy: the results reveal that Islamic banks, despite their ethical and Shariah-based foundations, exhibit disclosure patterns similar to conventional banks, underscoring the universality of legitimacy-seeking behaviour. These contributions strengthen the explanatory power of legitimacy theory and enrich sustainability scholarship by integrating global frameworks (e.g., TCFD, CCPT, SDGs) with Shariah principles.

Looking ahead, this study recommends several future research directions. Comparative studies involving conventional banks and Islamic banks in other jurisdictions such as Indonesia or the Gulf Cooperation Council (GCC) countries could offer global benchmarking and identify contextual best practices. Additionally, future research should explore quantitative assessments of green financing outcomes, such as emission reductions, credit risk mitigation, and financial returns, to empirically evaluate the impact of sustainability initiatives (Berg et al., 2022). Another underexplored area is the consumer perspective on Islamic green financial products. Understanding customer awareness, preferences, and willingness to adopt green financing solutions will be essential for product design and market scaling (Mir et al., 2025). Moreover, integrating Maqasid al-Shariah into ESG evaluation frameworks could enhance the ethical orientation of Islamic green finance and distinguish it further from conventional sustainability models (Mohd Zain et al., 2024). Finally, longitudinal studies tracking the evolution of sustainability disclosures among Islamic banks over time could offer valuable insights into institutional learning, regulatory influence, and shifts in sustainability priorities.

References

Accenture. (2022). Banking for Net Zero.

Agrobank. (2023). Annual Integrated Report 2023.

Alam, N., Duygun, M., & Ariss, R. T. (2016). Green Sukuk: An Innovation in Islamic Capital Markets. In Energy and Finance (pp. 167–185). Springer International Publishing. https://doi.org/10.1007/978-3-319-32268-1_10

Andatu, M., & Hilabi, A. (2023). The Implementation of Sustainable Financial Regulation in Islamic and Conventional Banks in Indonesia. Al Irsyad: Jurnal Studi Islam, 2(1), 23–34. https://doi.org/10.54150/alirsyad.v2i1.116

Anggraini, S., & Muhammad Iqbal, F. (2022). Analisis Pengaruh Green Banking Terhadap Profitabilitas Bank Umum Syariah Indonesia. Journal of Business Management and Islamic Banking, 1(1), 73–88. https://doi.org/10.14421/jbmib.2022.011-05

Araminta, D. V., Qudziyah, Q., & Timur, Y. P. (2022). The Role of Green Sukuk in Realizing the Sustainable Development Goals 2030 Agenda. Jurnal Ekonomi Dan Bisnis Islam (Journal of Islamic Economics and Business), 8(2), 251–266. https://doi.org/10.20473/jebis.v8i2.37531

Bank Islam. (2024). Integrated Annual Report 2024.

Bank Muamalat. (2023). Annual Report 2023.

Bank Negara Malaysia. (2021). Climate Change and Principle-based Taxonomy.

Bank Negara Malaysia. (2023). The Malaysian Islamic Financial Market Report.

Bank Rakyat. (2023). Bank Rakyat’s Sustainability Report.

Berg, F., Kölbel, J. F., & Rigobon, R. (2022). Aggregate Confusion: The Divergence of ESG Ratings. Review of Finance, 26(6), 1315–1344. https://doi.org/10.1093/rof/rfac033

Bowen, G. A. (2009). Document Analysis as a Qualitative Research Method. Qualitative Research Journal, 9(2), 27–40. https://doi.org/10.3316/QRJ0902027

Braun, V., & Clarke, V. (2006). Using thematic analysis in psychology. Qualitative Research in Psychology, 3(2), 77–101. https://doi.org/10.1191/1478088706qp063oa

BSN. (2023). BSN Sustainability Report 2023.

Bukhari, S. A. A., Hashim, F., & Amran, A. (2020). The Journey of Pakistan’s Banking Industry Towards Green Banking Adoption. South Asian Journal of Business and Management Cases, 9(2), 208–218. https://doi.org/10.1177/2277977920905306

Bukhari, S. A. A., Hashim, F., Amran, A. Bin, & Hyder, K. (2019). Green Banking and Islam: two sides of the same coin. Journal of Islamic Marketing, 11(4), 977–1000. https://doi.org/10.1108/JIMA-09-2018-0154

Cho, C. H., Laine, M., Roberts, R. W., & Rodrigue, M. (2015). Organized hypocrisy, organizational façades, and sustainability reporting. Accounting, Organizations and Society, 40, 78–94. https://doi.org/10.1016/J.AOS.2014.12.003

Creswell, J. W., & Creswell, D. J. (2022). Research Design: Qualitative, Quantitative, and Mixed Methods Approaches. SAGE Publications.

d’Aspremont, C. (2023). Navigating Sustainable Finance: Challenges and Opportunities for Banks on Their Path to Net Zero Goals. Greenomy. https://www.greenomy.io/blog/sustainable-finance-banks-challenges-opportunities#:~:text=Overall%2C%20with%20the%20right%20approach,financial%20data%20from%20their%20clients.

Deegan, C. (2002). Introduction the legitimising effect of social and environmental disclosures – a theoretical foundation. Accounting, Auditing & Accountability Journal, 15(3), 282–311. https://doi.org/10.1108/09513570210435852

Donner, E. K., Meißner, A., & Bort, S. (2025). Moving from voluntary to mandatory sustainability reporting—Transparency in sustainable development goals (SDG) reporting: An analysis of Germany’s largest MNCs. Business Ethics, the Environment & Responsibility, 34(3), 900–911. https://doi.org/10.1111/beer.12687

Euromoney. (2021). Malaysia brings Islamic finance and ESG together. Euromoney. https://www.euromoney.com/article/297ljl7o060lbd1wh23nk/sustainability/malaysia-brings-islamic-finance-and-esg-together/

Fajriah, S. D., Riani, R., & Surur, M. (2023). Does the Implementation of Green Banking Affect the Profitability of Islamic Banks in Indonesia? Proceedings of Femfest International Conference on Economics, Management, and Business.

Fereday, J., & Muir-Cochrane, E. (2006). Demonstrating Rigor Using Thematic Analysis: A Hybrid Approach of Inductive and Deductive Coding and Theme Development. International Journal of Qualitative Methods , 5(1), 80–92. https://doi.org/10.1177/160940690600500107

Financial Stability Board. (2015). Task Force on Climate-related Financial Disclosures (TCFD).

Firmansyah, A., & Kartiko, N. D. (2024). Exploring the association of green banking disclosure and corporate sustainable growth: The moderating role of firm size and firm age. Cogent Business and Management, 11(1). https://doi.org/10.1080/23311975.2024.2312967;WGROUP:STRING:PUBLICATION

Hahn, R., & Kühnen, M. (2013). Determinants of sustainability reporting: a review of results, trends, theory, and opportunities in an expanding field of research. Journal of Cleaner Production, 59, 5–21. https://doi.org/10.1016/j.jclepro.2013.07.005

Hamidi, M. L., & Worthington, A. C. (2021). Islamic banking sustainability: Theory and evidence using a novel quadruple bottom line framework. International Journal of Bank Marketing, 39(5), 751–767. https://doi.org/10.1108/IJBM-06-2020-0345

Hermala, I., Sunitiyoso, Y., & Sudrajad, O. Y. (2024). Green Financing Using Islamic Finance Instruments in Indonesia: A Bibliometrics and Literature Review. International Journal of Energy Economics and Policy, 15(1), 239–248. https://doi.org/10.32479/ijeep.17208

Hollebeek, L. D., Kumar, V., Srivastava, R. K., Lim, W. M., & Urbonavicius, S. (2025). Guidelines for Theory Selection: The IMPACT Framework. Psychology and Marketing, 42(11), 2789–2806. https://doi.org/10.1002/mar.70009

Institute for Capital Market Research Malaysia. (2023). Environmental, Social and Governance (ESG) Integration in Malaysia: Navigating Challenges and Embracing Opportunities for a Sustainable Future.

Islam, M. T., & Kokubu, K. (2018). Corporate social reporting and legitimacy in banking: a longitudinal study in the developing country. Social Responsibility Journal, 14(1), 159–179. https://doi.org/10.1108/SRJ-11-2016-0202

Khan, M., Serafeim, G., & Yoon, A. (2015). Corporate Sustainability: First Evidence on Materiality. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.2575912

Khattak, M. A., Ali, M., & Burki, A. K. (2020). Sustainability-Disclosures and Financial Performance: Shariah Compliant vs Non-Shariah-Compliant Indonesian Firms. Journal of Islamic Monetary Economics and Finance, 6(4), 789–810. https://doi.org/10.21098/jimf.v6i4.1087

Krippendorff, K. (2019). Content Analysis: An Introduction to Its Methodology. SAGE Publications, Inc. https://doi.org/10.4135/9781071878781

Kurniawati, A. D. (2025). Revealing Sustainability Performance: A Content Analysis of Sustainability Reporting from Big Four Indonesian Banking Institutions. Proceedings of the 12th Gadjah Mada International Conference on Economics and Business, 46–60. https://doi.org/10.2991/978-94-6463-692-5_4

Kyngäs, H. (2020). Inductive Content Analysis. In The Application of Content Analysis in Nursing Science Research (pp. 13–21). Springer, Cham. https://doi.org/10.1007/978-3-030-30199-6_2

Liu, F. H., & Lai, K. P. (2021). Ecologies of green finance: Green sukuk and development of green Islamic finance in Malaysia. Environment and Planning A: Economy and Space, 53(8), 1896–1914. https://doi.org/10.1177/0308518X211038349

Martini, M., & Creed, A. (2025). The Transition to Net Zero: Banks Can Do Better.

MBSB. (2024). MBSB’s Sustainability Report 2024.

Michelon, G., Pilonato, S., & Ricceri, F. (2015). CSR reporting practices and the quality of disclosure: An empirical analysis. Critical Perspectives on Accounting, 33, 59–78. https://doi.org/10.1016/J.CPA.2014.10.003

Mir, A. A., Bhat, A. A., Al-Adwan, A. S., Farooq, S., Jamali, D., & Malik, I. A. (2025). Green banking practices and customer satisfaction-way to green sustainability. Innovation and Green Development, 4(2), 100221. https://doi.org/10.1016/j.igd.2025.100221

Mohd Zain, F. A., Muhamad, S. F., Abdullah, H., Sheikh Ahmad Tajuddin, S. A. F., & Wan Abdullah, W. A. (2024). Integrating environmental, social and governance (ESG) principles with Maqasid al-Shariah: a blueprint for sustainable takaful operations. International Journal of Islamic and Middle Eastern Finance and Management, 17(3), 461–484. https://doi.org/10.1108/IMEFM-11-2023-0422

Muchiri, M. K., Erdei-Gally, S. K., & Fekete-Farkas, M. (2025). Green Banking Practices, Opportunities, and Challenges for Banks: A Systematic Review. Climate, 13(5), 102. https://doi.org/10.3390/cli13050102

Pipere, A., Reunamo, J., & Jones, M. (2010). Perceptions of Research in Education for Sustainable Development: An International Perspective. Discourse and Communication for Sustainable Education, 1(2), 5–24. https://doi.org/10.2478/dcse-2013-0011

Qoyum, A., Sakti, M. R. P., Thaker, H. M. T., & AlHashfi, R. U. (2022). Does the Islamic label indicate good environmental, social, and governance (ESG) performance? Evidence from sharia-compliant firms in Indonesia and Malaysia. Borsa Istanbul Review, 22(2), 306–320. https://doi.org/10.1016/j.bir.2021.06.001

Rahman, S., Moral, I. H., Hassan, M., Hossain, G. S., & Perveen, R. (2022). A systematic review of green finance in the banking industry: Perspectives from a developing country. Green Finance, 4(3), 347–363. https://doi.org/10.3934/GF.2022017

Salsabila, A., Fasa, M. I., Suharto, S., & Fachri, A. (2022). Trends in Green Banking as Productive Financing in Realizing Sustainable Development. Az-Zarqa’: Jurnal Hukum Bisnis Islam, 14(2), 151–174. https://doi.org/10.14421/azzarqa.v14i2.2562

Sebastião, A. M., Tavares, M. C., & Azevedo, G. (2024). Evolution and Challenges of Sustainability Reporting in the Banking Sector: A Systematic Literature Review. Administrative Sciences, 14(12), 333. https://doi.org/10.3390/admsci14120333

Securities Commission Malaysia. (2019). Sustainable and Responsible Investment Sukuk Framework An Overview.

Spetic, W., Marquez, P., & Kozak, R. (2012). Critical Areas and Entry Points for Sustainability‐Related Strategies in the Sugarcane‐Based Ethanol Industry of Brazil. Business Strategy and the Environment, 21(6), 370–386. https://doi.org/10.1002/bse.1727

Stern, N., & Valero, A. (2021). Innovation, growth and the transition to net-zero emissions. Research Policy, 50(9), 104293. https://doi.org/10.1016/j.respol.2021.104293

Suchman, M. C. (1995). Managing Legitimacy: Strategic and Institutional Approaches. The Academy of Management Review, 20(3), 571. https://doi.org/10.2307/258788

UNEP Finance Initiative. (2025). Guidance for Climate Target Setting for Banks.

Vőneki, Z. T., & Lamanda, G. (2020). Content analysis of bank disclosures related to ESG risks. Economy & Finance, 7(4), 412–424. https://doi.org/10.33908/eF.2020.4.3

Weber, O. (2017). Corporate sustainability and financial performance of Chinese banks. Sustainability Accounting, Management and Policy Journal, 8(3), 358–385. https://doi.org/10.1108/SAMPJ-09-2016-0066

Zhixia, C., Hossen, Md. M., Muzafary, S. S., & Begum, M. (2018). Green Banking for Environmental Sustainability-Present Status and Future Agenda: Experience from Bangladesh. Asian Economic and Financial Review, 8(5), 571–585. https://doi.org/10.18488/journal.aefr.2018.85.571.585